When you hear the term 'full coverage,' it's easy to picture an impenetrable shield for your car, a single policy that handles everything. But in the world of auto insurance, it’s not quite that simple.

So, from our perspective as Atlanta personal injury attorneys, what does full coverage mean in auto insurance? It’s not an official product you can buy off a shelf. Instead, it’s a common phrase for a bundle of different coverages that provides broad protection far beyond Georgia’s legal minimums. Think of it as a financial safety net designed to protect you, not just other drivers.

Decoding the Myth of Full Coverage

Let's clear the air right away: "full coverage" is a common phrase, not a formal insurance policy. Both agents and drivers use it to describe a package of coverages that protects your finances after a crash.

Think of it less like one giant umbrella and more like a well-stocked toolkit. Each tool—or coverage—is designed for a specific job.

When someone says they have full coverage, their policy almost always includes three core components:

- Liability Coverage: This is the non-negotiable foundation required by Georgia law. It pays for injuries and property damage you cause to other people in an at-fault accident. It does nothing for you or your car.

- Collision Coverage: This is the part that pays to repair or replace your own vehicle after a collision with another car or an object (like a pole or a wall), regardless of who was at fault.

- Comprehensive Coverage: This handles damage to your car from just about everything else—events that aren't a collision. Common examples include theft, vandalism, fire, storm damage, or hitting a deer.

The main reason to bundle these coverages is to protect your financial stake in your own vehicle, something basic liability insurance simply won't do. If you have a car loan or lease, your lender will almost certainly require you to carry both collision and comprehensive coverage to protect their investment.

Insurance terms can be confusing. Our legal dictionary can help clarify some of the jargon you'll run into.

Full Coverage vs Minimum Liability at a Glance

To see the difference in practical terms, here’s a quick comparison of what you get with a typical full coverage package versus the bare-bones minimum required in Georgia.

| Coverage Aspect | Minimum Liability | Typical Full Coverage |

|---|---|---|

| Your Vehicle's Repairs | Not covered. You pay out-of-pocket for all damages. | Covered. Collision coverage pays for repairs after a crash. |

| Theft or Vandalism | Not covered. You bear the full cost of a stolen or damaged car. | Covered. Comprehensive coverage handles these non-collision events. |

| Other Driver's Injuries | Covered (up to your policy limits). | Covered (usually with much higher limits for better protection). |

| Your Own Injuries | Not covered. | Covered (if you add MedPay or have Uninsured Motorist coverage). |

| Storm Damage (Hail, Floods) | Not covered. | Covered under your comprehensive policy. |

As you can see, the gap in protection is massive. Minimum liability protects others from your actions, while full coverage is designed to protect you and your assets.

The Real-World Picture

Most drivers understand that minimum liability leaves them financially exposed. According to the Insurance Information Institute, about 80% of insured drivers nationally carry comprehensive coverage, and 77% have collision.

That extra protection comes at a cost. A full coverage policy can average over $1,900 more per year than a state minimum plan. But that higher premium is what pays to get your car back on the road after an accident or replace it after a theft. Getting a true understanding of what does full coverage mean in auto insurance is the first step toward ensuring you have the protection you actually need before a crash happens.

The Building Blocks of a Full Coverage Policy

When people talk about auto insurance, "full coverage" is a term that gets thrown around a lot. But it's not actually a specific type of policy you can buy off the shelf. Instead, think of it as a package of different coverages bundled together to give you the most complete protection.

Your state-mandated liability insurance is the bare minimum—it’s the foundation. But that only protects other people when you cause an accident. To protect your own car and your own financial well-being, you need to add more layers. So, what does full coverage mean in auto insurance? It's the combination of liability with other important protections that shield you.

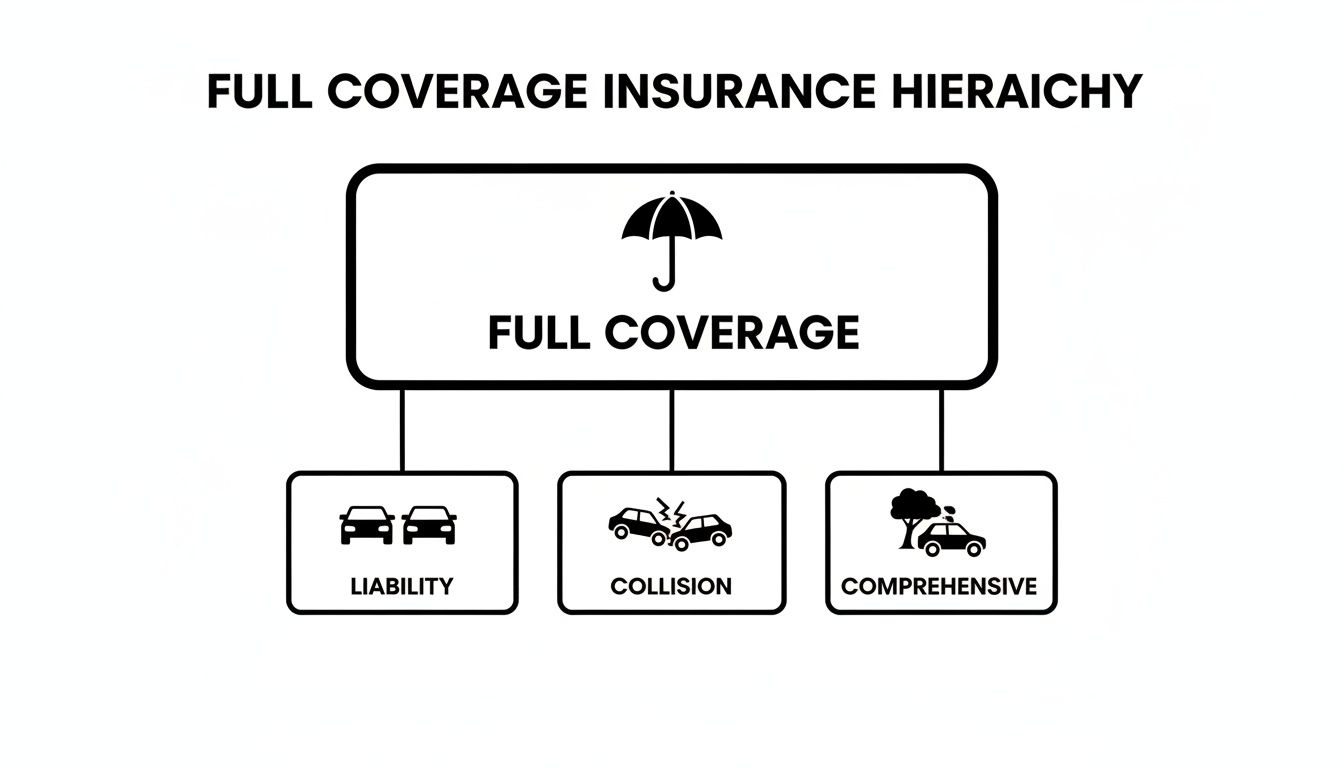

This diagram shows how the core components come together under the "full coverage" umbrella.

Let's break down exactly what goes into a solid full coverage policy.

The Three Core Components

A genuine full coverage package is built on three pillars. Each one is designed to handle a different kind of risk you face on the road.

- Liability Coverage: This is the non-negotiable part required by the Georgia Department of Revenue. It pays for the injuries and property damage you cause to others in a crash. Importantly, it does not pay for your car or your medical bills.

- Collision Coverage: This is what pays to fix or replace your car after it's damaged in a collision with another vehicle or an object—think hitting a guardrail on I-285 or backing into a pole. It kicks in no matter who was at fault for the accident.

- Comprehensive Coverage: You can think of this as "non-crash" damage protection. It covers you for things like theft, vandalism, fire, hail, flooding, or hitting a deer. If your car gets stolen from a Braves game parking lot, comprehensive coverage is what helps you recover.

Together, these three create a powerful financial shield. Liability protects your assets from a lawsuit, while collision and comprehensive protect the actual value of your vehicle.

Essential Add-Ons We Always Recommend

Beyond the big three, there are a few other coverages that we, as attorneys who deal with the aftermath of serious crashes every day, consider absolutely essential. Without them, you're leaving yourself dangerously exposed.

The single most important protection you can buy is Uninsured/Underinsured Motorist (UM/UIM) coverage. This is what pays for your injuries, lost wages, and other damages when the driver who hit you has no insurance or not enough to cover the harm they caused.

It’s a sad fact that many drivers in Georgia are uninsured or carry only the bare minimum limits. This coverage is your personal safety net. Here are the other key additions:

- Uninsured/Underinsured Motorist (UM/UIM) Coverage: This is your primary defense against irresponsible drivers. It covers your medical bills, pain and suffering, and property damage when you're hit by someone who can't pay. Georgia law requires insurers to offer it, and you should always take it.

- Medical Payments (MedPay): This coverage helps pay medical expenses for you and your passengers right away, regardless of who was at fault. It's great for covering immediate costs like ambulance rides, emergency room visits, and health insurance deductibles without having to wait for a settlement.

When you combine these building blocks, you get what is commonly known as "full coverage" insurance—a package truly designed to provide peace of mind and real financial security when you need it most.

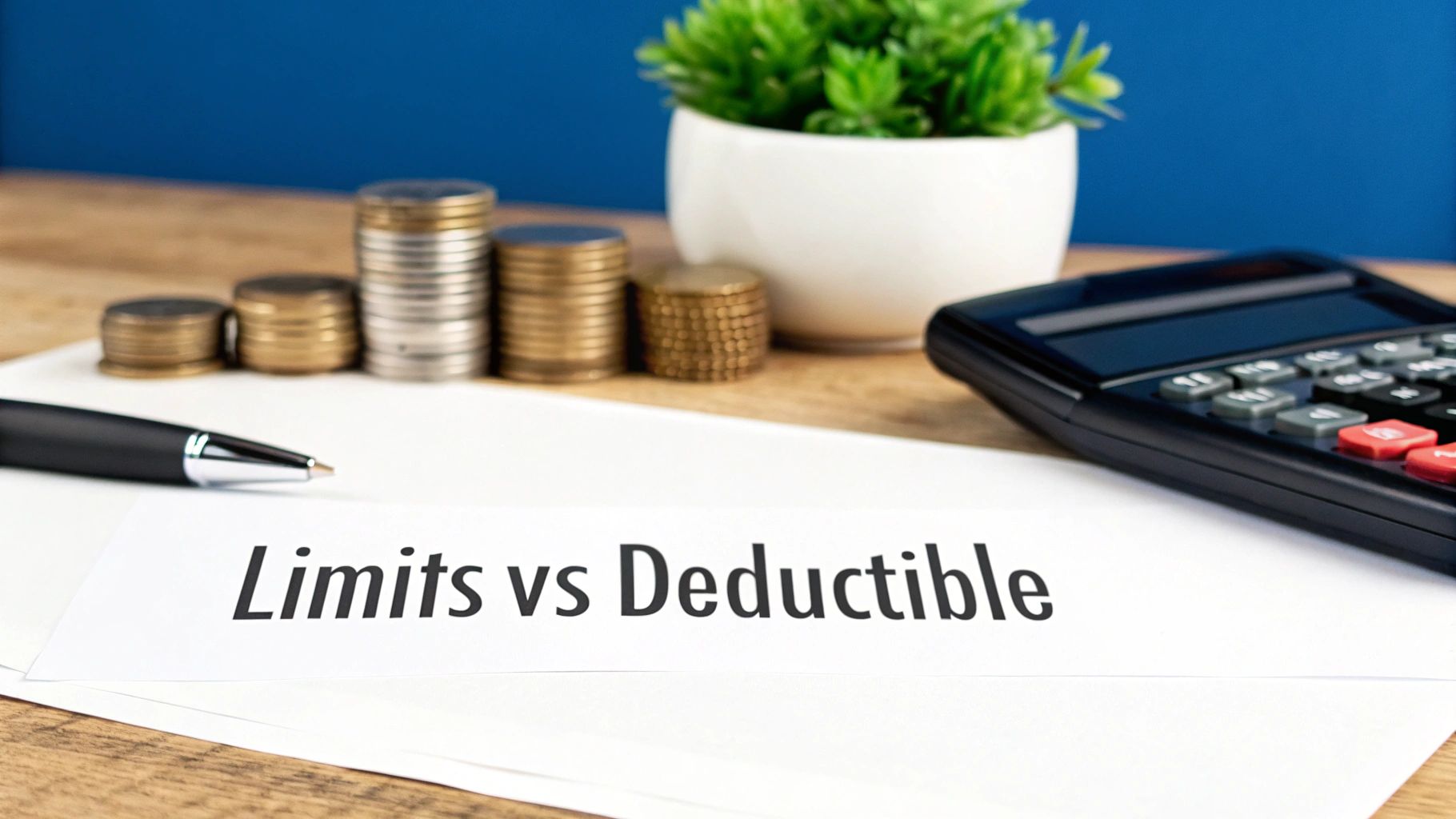

How Policy Limits and Deductibles Work

Simply having the right types of coverage is only half the battle. If you really want to understand what does full coverage mean in auto insurance, you have to look at the numbers: your policy limits and deductibles.

These two figures truly define how much financial protection you have after a crash. They work hand-in-hand, so let's break them down.

Think of your policy limit as the absolute maximum your insurance company will pay out for a covered claim. It's the ceiling. Your deductible, on the other hand, is the amount you have to pay out-of-pocket before your insurer steps in to pay the rest.

Let's say you have a $1,000 collision deductible, and a fender-bender leaves you with a $5,000 repair bill. You'll pay the first $1,000, and your insurance company will cover the remaining $4,000. It's that simple. These two numbers also directly impact what you pay each month for your premium.

Your Policy Limits: The Maximum Payout

Policy limits are absolutely vital for your liability and Uninsured/Underinsured Motorist (UM/UIM) coverages. Georgia's minimum liability limit for property damage is a shockingly low $25,000.

Imagine causing a multi-car pileup on I-75 and totaling a brand-new pickup truck worth $60,000. Your insurance would pay its limit of $25,000. The truck's owner could then sue you personally for the remaining $35,000. That's a financially devastating scenario.

This is exactly why choosing higher limits is one of the smartest things any driver can do. We strongly recommend carrying at least:

- $100,000 in bodily injury liability per person

- $300,000 in bodily injury liability per accident

- $100,000 in property damage liability

These higher limits create a much stronger financial shield around you and your assets. While it focuses on a different area, the state provides some helpful resources for understanding insurance requirements, like those from the State Board of Workers' Compensation.

It's just as important that your UM/UIM limits match your liability limits. This ensures you and your family are protected to the same extent that you protect others if you're hit by someone with little or no insurance.

Your Deductible: The Upfront Cost

Deductibles only come into play for your own vehicle's repairs through collision and comprehensive coverage. They directly influence two key things: your monthly premium and how much cash you'll get for a claim. Common deductible amounts are $500, $1,000, or even $2,500.

Here’s the trade-off:

- A lower deductible (like $500) means you pay less out of your own pocket after a crash, but your monthly premium will be higher.

- A higher deductible (like $1,000) means you pay more upfront for repairs, but you'll enjoy a lower monthly premium.

Choosing the right deductible comes down to balancing your monthly budget with what you could realistically afford to pay on short notice after an accident. Getting a firm grip on how limits and deductibles work is the key to truly knowing what full coverage means for your specific situation.

Understanding the Real-World Cost

One of the biggest questions people have is a simple one: how much more does full coverage actually cost?

It’s true you’ll pay more for a full coverage policy compared to a bare-bones liability plan. But it helps to see that extra cost as an investment in your own financial safety. The higher premium buys you tangible protection for your vehicle and your savings.

Saving a few bucks each month with a minimum policy feels good, until it doesn't. A single at-fault wreck could leave you with thousands in repair bills that a full coverage plan would have handled. That’s the fundamental trade-off.

Breaking Down the Premium Difference

The price gap between liability-only and full coverage is significant, and for good reason—you're paying to protect your own car from damage or total loss.

Recent data shows that full coverage averaged $2,638 per year nationally, which is more than three times the $736 average for a liability-only policy. The difference is what pays to repair or replace your vehicle after a wreck. You can see a more detailed breakdown of these costs on Stanton Insurance's website and learn how a small monthly increase prevents a massive out-of-pocket expense.

To illustrate how these costs can vary, here's a quick comparison of average annual premiums.

Average Annual Premium Comparison

| Coverage Type | National Average Cost | Example State Cost (NC) |

|---|---|---|

| Minimum Liability | $736 | $510 |

| Full Coverage | $2,638 | $1,621 |

This data highlights how much more protection you get with full coverage, reflected in the premium.

That gap is especially important today. After recent supply chain shortages, the price of car parts jumped by 20-30%, making collision repair claims much more expensive. For anyone with a financed vehicle—which includes a huge number of drivers—lenders will require this protection anyway.

Key Factors Influencing Your Premium

Your auto insurance premium isn't a one-size-fits-all number. Insurers in a busy metro area like Atlanta look at a variety of factors to determine your specific rate.

Here are some of the most common elements that will raise or lower your costs:

- Your Driving Record: A clean record with no accidents or tickets will always result in lower premiums. Simple as that.

- The Car You Drive: The make, model, age, and safety features of your vehicle play a big role. A new, expensive car costs more to insure than an older, modest one.

- Your Location: Where you live and park your car matters. Zip codes in Atlanta with higher rates of theft or accidents will often have higher premiums.

- Your Chosen Deductible: As we discussed, opting for a higher deductible (like $1,000 instead of $500) will lower your monthly payment.

Ultimately, the goal is to balance the monthly cost against the potential financial disaster of being underinsured. Seeing the true value in this protection helps you make a smarter choice long before you ever need to file a claim.

You can also find more general information and tools by checking out our other available resources. Understanding what full coverage means in auto insurance is about weighing this cost against the very real risk of a major financial hit.

Common Misconceptions About Full Coverage

Because "full coverage" isn't a real insurance product you can buy off a shelf, it's surrounded by myths that cause major headaches after an accident. To really get a handle on what does full coverage mean in auto insurance, we first have to bust some of the most common misunderstandings we see from clients every single day.

A lot of drivers assume that if their car is in the shop after a wreck, their "full coverage" policy will automatically pay for a rental car. That's almost never the case. That specific protection, called rental reimbursement, is an optional add-on that you have to ask for and pay extra for. Without it, you’re left finding your own transportation while your car is being fixed.

Another big point of confusion is personal property. If someone smashes your window and steals your laptop, your auto insurance won't cover the stolen items. Your comprehensive coverage will pay to fix the broken window, but your laptop or gym bag falls under your homeowners or renters insurance policy.

What Is Not Covered By a Standard Full Coverage Policy

Knowing what your policy doesn't cover is just as important as knowing what it does. A standard "full coverage" policy will almost never pay for these things:

- Mechanical Breakdowns: If your engine seizes up or your transmission fails from normal wear and tear, your auto insurance won't help. Those are maintenance issues, not accident-related damage.

- Routine Maintenance: Things like oil changes, new tires, or replacing brake pads are all part of owning a car and are your financial responsibility.

- Custom Parts and Equipment: That expensive sound system or those custom rims you installed probably aren't fully covered unless you bought a special add-on, often called an "endorsement," to protect them.

- Intentional Damage: It should go without saying, but no insurance policy will cover you for intentionally damaging your own vehicle.

Even with a robust policy, you have to be aware of the details. For example, specialized protections like car key replacement insurance are almost always a separate add-on, not a standard part of a comprehensive plan.

The single biggest myth is that “full coverage” means unlimited coverage. Every single policy has a maximum payout, known as a policy limit. If the damages from a crash go over your limits, you could be on the hook personally for the rest.

Busting these myths gives you a realistic view of your insurance. Understanding the real story of what does full coverage mean in auto insurance is the best way to prevent a nasty surprise right when you need your policy the most.

What to Do After a Wreck with Full Coverage

Having a solid insurance policy is a great start, but knowing how to use it after a collision is a different ballgame. The hours and days after a car accident are chaotic and stressful. A clear plan of action is your best tool for protecting your rights and ensuring the claims process moves forward correctly.

Your first job is to ensure everyone's safety. If you can, move your car out of the flow of traffic. Call 911 immediately to report the crash and get paramedics on the way for anyone who is hurt. It’s important that you never admit fault at the scene—just provide the basic facts when you talk to the police and the other driver.

Starting Your Insurance Claim

Once you're in a safe spot, your next call is to your insurance company. Most carriers have 24/7 claims hotlines or mobile apps designed to get the process started quickly.

You’ll need a few key pieces of information to open the claim:

- Your policy number

- The date, time, and location of the crash

- A brief, factual account of what occurred

- Contact and insurance details for the other driver(s)

- The police report number, if you have it

After you report the wreck, an insurance adjuster will be assigned to your case. Their role is to investigate the accident, determine who was at fault, and evaluate the damage to your vehicle and any injuries you sustained. To get a better handle on what to expect, it's a good idea to review a guide on how to file an auto insurance claim.

Even with "full coverage," getting a fair settlement for your injuries, lost income, and vehicle damage can feel like an uphill battle. The insurance company's primary goal is to minimize its payout, which often isn't enough to make you whole again.

When to Consider Speaking with an Attorney

This is where the process often gets difficult. If your injuries are significant, if the other driver's insurer is fighting you on who was at fault, or if their settlement offer is insultingly low, it’s time to call a personal injury attorney. We can help you manage the tricky landscape of personal injury claims, take over all communications with the insurance company, and fight to protect your rights.

Understanding what does full coverage mean in auto insurance is the first step, but having a skilled advocate in your corner is the only way to secure the full compensation you deserve.

Frequently Asked Questions About Full Coverage

As Atlanta personal injury attorneys, we get a lot of questions about auto insurance. Here are some quick, straightforward answers to the most common ones we hear about "full coverage."

Do I Need Full Coverage if My Car Is Paid Off?

Legally speaking, no. Once you own your car free and clear, Georgia law only requires you to carry liability insurance. But from a financial standpoint, keeping full coverage is often the smartest move.

Think about it this way: if your car is still worth a decent amount, could you afford to pay for thousands of dollars in repairs—or replace it entirely—after a wreck? Full coverage is your financial safety net. A good rule of thumb is to consider dropping collision and comprehensive only if the annual premium costs more than 10% of your car's current market value.

Does Full Coverage Pay for Everything?

Absolutely not, and this is one of the most dangerous myths out there. "Full coverage" is just a nickname; it's not a blank check. Every single part of your policy has a limit, which is the maximum amount the insurance company will pay for a claim.

For example, let's say your policy has a $50,000 property damage limit. If you cause a crash that totals a brand-new $70,000 truck, you could be personally sued for the $20,000 difference. It also won't cover things like intentional damage or using your car for business unless you have a specific add-on.

A question we hear all the time is whether Uninsured/Underinsured Motorist (UM/UIM) coverage is automatic. While it's an important part of a solid policy, it isn't. Georgia insurers are required to offer it, but you have the right to reject it in writing. Given how many drivers are uninsured or underinsured, we strongly recommend you never reject this coverage.

Knowing what to do when you actually need to use your insurance is key. For a step-by-step guide, check out our article on how to file a car accident claim in Atlanta. This resource helps clarify what does full coverage mean in auto insurance when you're in the middle of a claim.