Getting a denial letter for your insurance claim feels like a punch in the gut. You’ve paid your premiums, you got hurt, and now the insurance company you trusted is telling you "no." It’s infuriating, but the absolute worst thing you can do right now is get emotional or give up. Figuring out what to do when your insurance claim is denied starts with a calm, strategic approach.

That denial letter isn't just a rejection; it's the key to your entire appeal.

Your First Steps After an Insurance Claim Denial

Insurance companies are legally required to give you a specific reason for denying your claim. You need to read that letter carefully—multiple times, if necessary—to understand exactly why they made their decision. Often, initial denials are based on simple mistakes, missing paperwork, or a misunderstanding that can be cleared up.

Your next move is to get organized. Start a file—a physical one and a digital one—for every single document related to your injury and claim. This includes the denial letter, your original insurance policy, every email and letter you've exchanged with the adjuster, photos, medical bills, and police reports. This file is now your arsenal.

Request Your Complete Claim File

Here’s a step most people miss: you have the right to see everything the insurance company has on your claim.

Send a formal, written request to the adjuster for a complete copy of your claim file. Don't just email them. Send it via certified mail with a return receipt so you have undeniable proof they got it.

This file is a treasure trove of information that can help you build your appeal. It will contain things like:

- The adjuster’s internal notes and communications about your case.

- Reports from any investigators or so-called "experts" they hired.

- The medical records or evaluations they reviewed to make their decision.

- A complete copy of the applicable insurance policy, not just the summary pages.

Getting their file allows you to see their playbook. You can find out what they focused on, where they made assumptions, and what evidence they might have ignored. For a more detailed breakdown of this process, check out this helpful comprehensive guide on what to do when your insurance claim is denied.

The table below breaks down some of the most common reasons for claim denials and what you should do immediately.

Common Denial Reasons and Your First Action

| Denial Reason | What It Means | Your Immediate First Step |

|---|---|---|

| Lapsed Policy | They claim your coverage wasn't active at the time of the incident. | Pull your payment records and proof of active coverage for the date of the incident. |

| Liability Dispute | They're arguing that their policyholder was not at fault for your injuries. | Gather the police report, witness statements, photos, and any other evidence proving fault. |

| Excluded Coverage | They say the specific circumstances of your injury aren't covered by the policy. | Request the full policy document and find the exact language they are citing. |

| Lack of Medical Evidence | They believe your injuries aren't as severe as you claim or aren't related to the incident. | Compile all your medical records, doctor's notes, and diagnostic test results. |

| Missed Deadline | They allege you failed to report the claim or submit paperwork on time. | Review the policy for the exact deadlines and find your records showing when you filed. |

Looking at their reasoning helps you focus your efforts where they'll have the most impact.

The single biggest mistake people make is giving up after the first denial. Insurance companies often count on you being too discouraged to fight back. Simply taking these initial organizational steps puts you in a much stronger position to challenge their decision.

This initial phase is all about gathering intelligence. Once you understand exactly why they said "no" and have a copy of their file, you’re equipped to build a powerful, evidence-based appeal. You can find more information on how we approach these situations on our page about Atlanta personal injury claims. Knowing what to do when your insurance claim is denied starts right here.

Decoding the Denial Letter and Building Your Case

So, you've gotten that dreaded denial letter. Before you do anything else, grab that letter and a highlighter. This document is your roadmap to fighting back.

Insurance companies are legally required to give you a reason for their decision, even if it's buried in dense jargon and policy codes. Your first mission is to translate their legalese into an action plan.

Look for specific phrases like "not a covered benefit," "liability dispute," or "lack of medical necessity." Those aren't just empty words; they're the exact arguments you now have to disprove. To do that, you need to know your policy inside and out. If you're dealing with a property claim, this complete guide to a homeowners insurance policy can give you a solid feel for how these documents are put together.

Understanding Insurance Jargon

The language in these letters is often technical on purpose. For instance, if the denial cites an "exclusion," it means the insurer believes a specific part of your policy rules out coverage for your situation. A denial for "lack of supporting documentation" is usually an easier fix—it just means you haven't sent them a key piece of evidence yet.

Don't guess what a term means. If you run into something you don't understand, look it up. Our Atlanta personal injury legal dictionary is a great place to start for plain-English explanations. Pinpointing their exact reason for the denial is the foundation for a strong rebuttal.

My experience has shown that many denials hinge on one or two key pieces of disputed information. The insurer is making a bet that you won't take the time to find and present the evidence that proves them wrong. Your job is to call that bet.

Building Your Evidence File

Once you know why they said no, it’s time to gather the proof that dismantles their argument. Think of yourself as a detective building an undeniable case file. Your goal is to overwhelm them with so much factual evidence that upholding the denial becomes impossible.

For an Atlanta-area accident claim, your evidence checklist needs to be airtight.

- The Official Police Report: Get the full, official report from the Atlanta Police Department or the relevant county's sheriff's office. This is often the most vital document in a liability dispute.

- Complete Medical Records: This means everything—doctor’s visits, specialist consults, physical therapy notes, prescriptions, and diagnostic tests like X-rays or MRIs. Your records must tell a clear, chronological story of your injuries from the moment of the crash.

- Visual Documentation: Gather every photo and video from the accident scene. We're talking property damage to all vehicles, visible injuries, and any relevant road conditions or hazards.

- All Communications: Keep a log of every single phone call with the adjuster, noting the date, time, and what was discussed. Save every email and letter you've exchanged.

- Proof of Financial Losses: Collect pay stubs to document lost wages. Add in receipts for every out-of-pocket expense, from prescriptions to the cost of getting to your doctor appointments.

Organize these documents in a binder or a dedicated digital folder. When you have everything at your fingertips, you turn their rejection into the first step of your comeback.

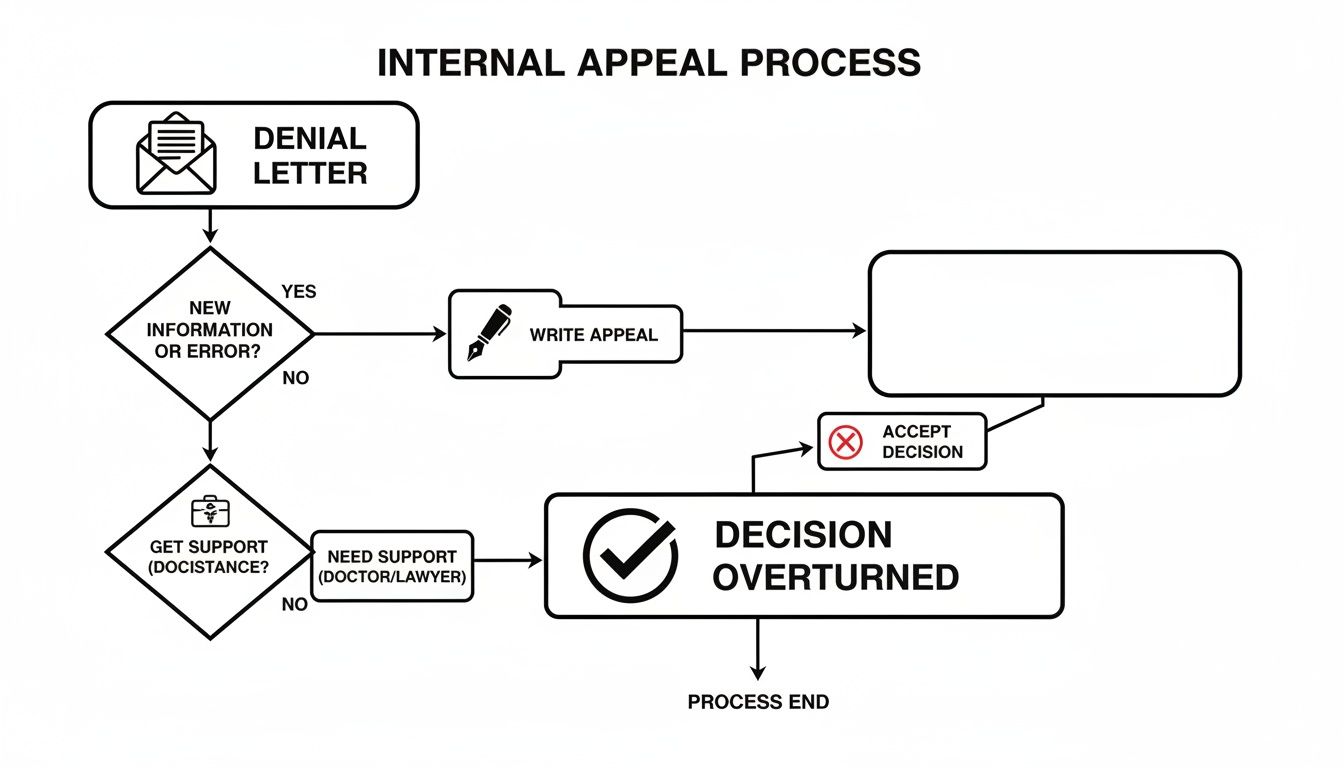

Mastering the Internal Appeal Process

When an insurance company denies your claim, your next move is to file an internal appeal. This is your first formal chance to make the insurer reconsider its decision, and it’s a step you absolutely cannot afford to skip. This isn't just about sending the same paperwork again and crossing your fingers. It’s about building a structured, persuasive case to systematically take apart their reasons for saying no.

A strong appeal is far more than just a letter—it's a professional, point-by-point rebuttal to their denial. You need to address every reason they gave, one by one, and counter it with the evidence you've gathered. Think of it as presenting your case to a fresh set of eyes within the company, someone who wasn't part of the initial denial and might see things differently.

Crafting Your Appeal Letter

Your appeal letter sets the entire tone for this stage. Keep it firm and factual, never emotional or angry.

Start by clearly stating that you are appealing the denial of your claim. Make sure to include your full name, policy number, and claim number right at the top for easy reference.

From there, structure your letter logically:

- State the Facts: Briefly recount the undisputed facts of the incident. For example, "On March 5, 2024, I was involved in a rear-end collision at the intersection of Peachtree Street and 10th Street NE."

- Address Their Denial Reason Directly: Quote the exact reason they gave you in their denial letter. For instance, "Your letter dated April 15, 2024, states the claim was denied due to a 'liability dispute.'"

- Present Your Counter-Evidence: This is where you make your case. Systematically explain why their reasoning is wrong and refer to the specific evidence you’ve included. For instance, "This position is contradicted by the enclosed police report (ATL-24-12345), which clearly assigns fault to your insured."

It's actually pretty encouraging to know that many denials get overturned right here. Industry data shows that a huge number of denials happen because of simple, fixable issues like missing information or basic coding errors. In fact, some analyses show that roughly 44% of internal appeals are ultimately successful. You can discover more about claim denial statistics and see for yourself how often a little persistence pays off.

The Power of a Doctor's Letter

If your claim was denied for a medical reason—maybe the insurer said a procedure wasn't "medically necessary"—a supporting letter from your doctor is one of the most powerful tools you have.

Don't just ask your doctor for a copy of your records. Ask them to write a specific letter of medical necessity. This letter needs to explain, in their professional opinion, why the treatment you received was essential for your recovery, directly connecting it to the injuries you sustained in the accident.

An insurance adjuster is a business professional, not a medical expert. A detailed letter from a physician laying out the clinical reasoning for your treatment is incredibly difficult for them to argue against. This one piece of evidence can completely change the dynamic of your appeal. By carefully building your case now, you give yourself the best possible shot at getting this resolved without having to escalate things any further.

Escalating Your Fight When an Appeal Fails

When your internal appeal gets rejected, it's easy to feel like you’ve hit a brick wall. This is a common tactic. The insurance company hopes you'll give up.

But this isn't the end of the road. It just means it's time to take your fight outside the insurance company's walls and use the systems in place to hold them accountable.

If an insurer refuses to police itself, there are official bodies that will. Here in Georgia, you have the right to file a formal complaint against the insurance company.

Filing a Complaint With the State of Georgia

The Georgia Office of Commissioner of Insurance and Safety Fire is the state agency that regulates insurance companies. Think of them as the official watchdog.

They investigate consumer complaints about issues like improper claim denials and unfair settlement practices. Filing a complaint gets your case in front of a neutral third party with the power to investigate the insurer's conduct.

The process is fairly straightforward and can be started online. You’ll need to provide all your documentation—the initial denial, your appeal letter, and any other correspondence you've had.

While the Commissioner’s office can't force the insurer to pay your specific claim, an official investigation often puts enough pressure on the company to make them reconsider their decision. Sometimes, just the threat of state oversight is enough to get them to the table.

Other Dispute Resolution Options

Beyond a state-level complaint, a couple of other avenues might fit your situation. These options are typically less formal and less costly than a full-blown lawsuit.

-

Mediation: This involves a neutral mediator who helps you and the insurer try to find common ground and reach a mutually agreeable settlement. It's a voluntary process, but it can be very effective at breaking a stalemate without going to court.

-

Appraisal: If your dispute is strictly about the amount of damages—for example, the adjuster says your car repairs are worth $3,000 but your body shop quotes $7,000—you might be able to invoke the appraisal clause in your policy. Each side hires an appraiser, and they work to agree on a fair value.

A denial from an insurance company doesn’t stop the clock on your legal deadlines. It is important to keep an eye on the calendar, because an insurer might drag out the appeals process intentionally. You can learn more about the statute of limitations for personal injury in GA on our site.

Ultimately, knowing what to do after a claim denial means understanding all the external tools at your disposal to continue the fight for fair treatment.

Knowing When to Hire an Atlanta Injury Attorney

While many parts of an insurance appeal can be handled on your own, some situations are a clear signal that it’s time to bring in professional legal help. Knowing what to do when your insurance claim is denied sometimes means recognizing the fight has moved beyond paperwork and phone calls. If you’re facing serious injuries, filing a lawsuit may be the only way to get the compensation you need for long-term recovery.

Hiring an attorney levels the playing field. Remember, the insurance company has a team of adjusters and lawyers whose job is to protect the company's bottom line. Having your own advocate ensures your rights are protected with the same degree of professional dedication.

Red Flags That Signal You Need an Attorney

You don't need a lawyer for every minor fender-bender, but certain actions from the insurance company are major red flags. If you experience any of the following, it's a good idea to seek a consultation right away.

- The Insurer Is Stalling or Unresponsive: Have weeks turned into months with no clear decision or communication? They may be delaying intentionally, hoping you’ll just give up.

- They Offer an Insultingly Low Settlement: A quick, lowball offer is a classic tactic. They're testing to see if you'll take a small amount of cash now instead of fighting for your claim's actual worth.

- They Blame You for the Accident: If they are unfairly shifting fault to you to avoid paying, you will need a strong legal argument—backed by solid evidence—to prove liability.

- Your Injuries are Severe or Permanent: Claims involving catastrophic injuries, long-term medical care, or permanent disability have very high stakes. Calculating future costs for this level of care is exactly what a personal injury attorney is trained to do.

When an insurance company denies a claim, it can create immediate financial pressure. A 2021 study by KFF found that 1 in 10 adults have medical debt, and surprise medical bills are a common source of that debt. This underscores the real-world financial consequences of a wrongful claim denial.

What an Injury Attorney Does for You

Once you hire an attorney, their team takes over the entire process. This immediately lifts a huge burden off your shoulders.

An experienced lawyer will manage all communications with the insurance company, so you no longer have to deal with adjusters. They will launch an independent investigation, gather important evidence, and may even hire accident reconstruction experts or medical specialists to build the strongest case possible.

Most importantly, they are not afraid to file a lawsuit if the insurer refuses to be fair. As an Atlanta personal injury attorney, I’ve seen firsthand how an insurer’s attitude can change the moment a formal lawsuit is filed. To get a better feel for this, you can learn more about Jamie Ballard's professional background and approach.

Most personal injury attorneys work on a contingent fee basis. This means you pay absolutely nothing unless they win your case. There are no upfront retainers or hourly bills. Their fee is simply a percentage of the final settlement or verdict, which directly aligns their interests with yours—getting you the maximum compensation possible. This is often the ultimate answer to what to do when an insurance claim is denied.

Common Questions About Denied Insurance Claims

After getting a denial notice from an insurance company, your head is probably swimming with questions. What now? It’s a confusing and frustrating spot to be in. Let's cut through the noise and get you direct answers to the questions we hear most often from people facing a denial right here in Atlanta.

How Long Do I Have to File an Appeal in Georgia?

This is the most time-sensitive question of all. The answer isn’t one-size-fits-all; it’s buried in your specific insurance policy documents. You absolutely must check your denial letter or the policy itself to find the exact deadline.

For many health insurance plans, federal law might give you up to 180 days for an internal appeal. But for your car or property insurance, the timeline is set by the contract you signed with them. Miss that deadline, and you could lose your right to challenge their decision for good. Time is not on your side.

How Does Georgia's At-Fault Law Affect My Claim?

Georgia is an "at-fault" state. In simple terms, this means the person who caused the accident is on the hook for the damages. You can see the official statute for yourself in the Official Code of Georgia Annotated (O.C.G.A.) § 51-1-6.

This law becomes the entire battleground when you're dealing with the other driver's insurance. One of the most common denial tactics is for the insurer to simply say, "our driver wasn't at fault." To win that fight, you need undeniable proof that says otherwise.

Your must-have evidence includes:

- The official police report, especially if it assigns fault.

- Clear photos and videos you took at the scene.

- Statements from any witnesses who saw what happened.

Without this, it’s just your word against their driver's, and the insurance company will almost always back their client.

Can an Insurer Deny My Claim Without a Reason?

No, they can't. Under Georgia law and their own policy contract, an insurance company is legally required to give you a specific, written reason for denying your claim. If they refuse to explain or give you a vague, nonsensical answer, that’s a massive red flag for "bad faith" insurance practices.

If an adjuster tells you your claim is denied over the phone and that's it, don't just accept it. Your next move should be to send a certified letter demanding a full, detailed explanation in writing. This creates a paper trail and signals that you're not backing down.

Documenting their lack of transparency is powerful evidence if you end up needing to file a complaint with the Georgia insurance commissioner or pursue legal action. Knowing your rights is the first step when you’re figuring out what to do after an insurance claim is denied.

If you're overwhelmed by the insurance company's games or have more questions about your denial, you don't have to fight this alone. The team at Jamie Ballard Law is here to offer a free, no-pressure case evaluation to help you figure out your next steps. Contact us 24/7 to get the help you need.