When you're sorting out your car insurance, the choice between stacked vs unstacked car insurance boils down to a single, important difference. Stacked insurance lets you combine the Uninsured/Underinsured Motorist (UM/UIM) coverage from all your vehicles, creating a much larger financial safety net. Unstacked insurance, on the other hand, limits you to the coverage on the one vehicle involved in the crash. Understanding this distinction is a key part of making an informed decision about your auto policy.

While stacked policies usually cost more, they offer significantly greater protection if you’re ever hit by a driver who has little or no insurance.

Understanding the Basics of Insurance Stacking

At its heart, "stacking" car insurance is your ability to combine—or "stack"—the uninsured (UM) and underinsured (UIM) bodily injury coverage limits from multiple vehicles you insure. The result is a much higher total amount of protection available to you after an accident with an at-fault driver who can't cover your bills.

Think of it as building a bigger financial cushion for you and your family. If you insure three cars, stacking allows you to add their individual UM/UIM coverage amounts together. This is a powerful tool for shielding yourself from the financial fallout of a serious collision, especially when medical bills and lost wages start piling up.

Many insurance terms can be confusing, but our legal dictionary can help clear things up for you.

Quick Overview Stacked vs Unstacked Insurance

This table offers a straightforward, side-by-side look at the fundamental differences between stacked and unstacked UM/UIM coverage.

| Feature | Stacked Insurance | Unstacked Insurance |

|---|---|---|

| Coverage Limits | Combines UM/UIM limits from multiple vehicles or policies. | Limits are restricted to the single vehicle in the accident. |

| Financial Protection | Offers a much higher total amount of available coverage. | Provides a lower, fixed amount of coverage. |

| Typical Premium Cost | Generally higher due to the increased coverage potential. | More affordable due to the limited coverage. |

| Best For | Households with multiple insured vehicles seeking maximum protection. | Single-vehicle owners or those prioritizing lower monthly costs. |

Ultimately, choosing between stacked vs unstacked car insurance is about balancing your monthly budget against your need for robust protection if the worst happens.

How Stacked Insurance Works in the Real World

Let's move past the definitions and see how this coverage actually performs when you need it most. Imagine you're a responsible driver in Atlanta with two family cars insured on one policy. Each car carries $50,000 in Uninsured/Underinsured Motorist (UM/UIM) bodily injury coverage.

One afternoon, you're rear-ended by a driver who has no insurance at all. The collision leaves you with serious injuries, and your medical bills quickly climb past $80,000. This is where stacking becomes an essential financial tool.

Because you opted for stacked coverage, you can combine the UM limits from both of your insured vehicles. Instead of being stuck with the $50,000 limit of the car you were driving, you now have access to a total of $100,000 ($50,000 + $50,000) to cover your medical bills, lost income, and other damages.

The Two Ways You Can Stack Coverage

Insurance stacking generally comes in two forms, and knowing the difference helps clarify how your policy can protect you. The specific options available will depend on your state's laws and your insurance carrier.

- Stacking Within a Single Policy: This is the most common approach. If you have multiple cars listed on the same auto insurance policy, you can combine the UM/UIM coverage for each one. Our earlier example—turning two $50,000 limits into a $100,000 pool—is a perfect illustration of this method.

- Stacking Across Multiple Policies: This method is used when a household has more than one auto insurance policy. For example, if you and your spouse maintain separate policies but live together, some states permit you to combine the UM/UIM limits from both policies if one of you is injured by an uninsured driver.

A key takeaway is that stacking transforms multiple smaller coverage amounts into a single, much larger safety net. It’s a way of ensuring the premiums you pay for all your vehicles work together to protect you in a serious accident.

Accessing these funds involves a specific claims process. You can learn more about what to expect by reviewing our guide on how to file a car accident claim in Atlanta, which outlines the necessary steps.

Seeing these scenarios makes it clear that stacking is more than just an abstract policy term. It's a tangible financial tool that can dramatically impact your ability to recover after a crash without facing overwhelming debt. The choice between stacked vs. unstacked coverage could mean the difference between a full recovery and a devastating financial setback.

The Big Catch with Unstacked Coverage

That lower monthly premium for unstacked coverage looks good on paper, but it’s important to understand what you’re giving up. When you choose unstacked insurance, you’re accepting a hard limit on what you can recover financially, a decision that could leave you seriously exposed after a major accident. It directly impacts your ability to pay for hefty medical bills and cover lost income when the at-fault driver has no insurance.

The limitation is pretty simple: your Uninsured/Underinsured Motorist (UM/UIM) coverage is capped at the limit for the one vehicle involved in the crash. It doesn’t matter if you pay premiums for three other cars on the same policy—their coverage is completely off-limits. This is the core difference you need to grasp when weighing stacked vs unstacked car insurance.

How the Single-Limit Cap Plays Out

Let’s go back to our earlier example. You have two cars, and each one is insured with a $50,000 UM/UIM policy. But this time, you opted for unstacked coverage to keep your premiums down.

An uninsured driver hits you, and your medical bills climb to $80,000. Your unstacked policy will only pay out the $50,000 limit of the car you were driving. That leaves you personally on the hook for the remaining $30,000. You’d have to find a way to cover that massive shortfall yourself, even though you’ve been dutifully insuring a second vehicle.

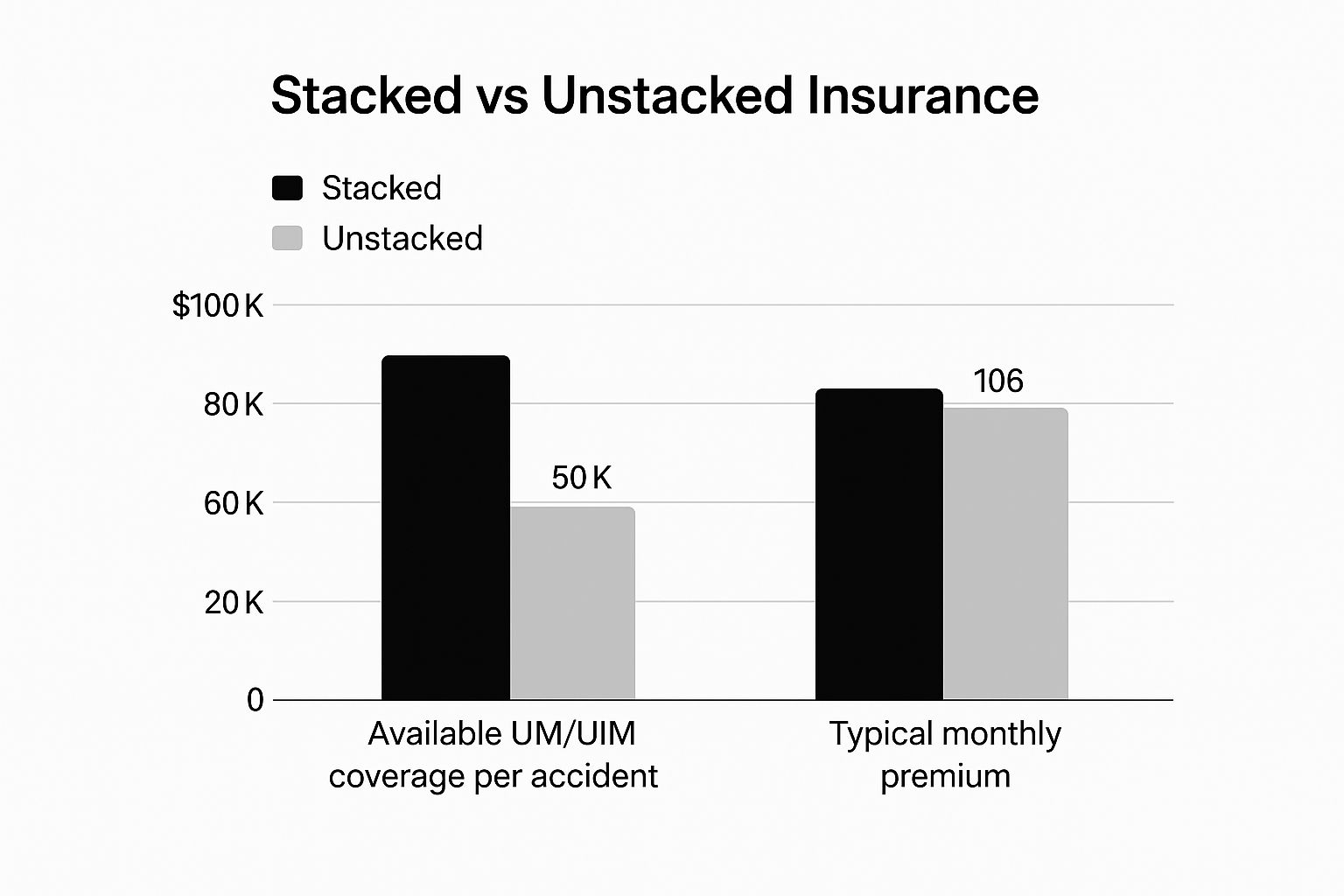

This infographic breaks down the potential coverage and typical costs between the two options.

As you can see, while unstacked insurance might save you a little bit on the premium, it slashes the available accident coverage in half in this scenario.

The Financial Gamble of Unstacked Policies

Unstacked car insurance is the default option in many states. It provides only the stated UM/UIM bodily injury coverage for that specific vehicle, no matter how many other cars are on your policy. If you have two cars, each with $50,000 in unstacked UM coverage, your maximum recovery after being hit by an uninsured driver is just $50,000. That's it—even though you pay premiums for both. You can always discover more insights about UM/UIM coverage formats on reputable insurance information sites to get a better handle on the details.

Choosing unstacked coverage is a bet. You’re betting that your damages from an accident with an uninsured driver will never go above the policy limit of a single vehicle.

That's a huge gamble, especially since severe injuries can easily send medical expenses far beyond standard policy limits. The upfront savings on your premium might feel good now, but they could look tiny compared to the financial ruin you might face after a collision. Ultimately, the debate over stacked vs unstacked car insurance boils down to this trade-off between short-term savings and long-term financial safety.

Comparing Coverage Potential And Costs

When you’re weighing stacked vs unstacked car insurance, you’re really choosing between a lower monthly premium and a larger safety net after an accident.

This isn’t simply about trimming your bill; it’s about how much protection you want when the unexpected happens.

Detailed Feature Comparison Stacked Vs Unstacked

Below is an in-depth look at how stacked and unstacked insurance differ across key aspects like cost, coverage limits, and risk.

| Comparison Point | Stacked UM/UIM Coverage | Unstacked UM/UIM Coverage |

|---|---|---|

| Total Available Coverage | High. Limits from all vehicles on your policy combine into one pool. | Low. Capped at the single vehicle’s policy limit. |

| Typical Premium Costs | Higher. You pay more to access a larger financial safety net. | Lower. Premium stays down because payout is limited. |

| Financial Risk Exposure | Lower. Extra protection guards against catastrophic medical bills or lost wages. | Higher. You face bigger out-of-pocket costs if bills exceed the limit. |

| State Law Availability | Varies. Allowed in states like Georgia and Florida; banned in others. | Universal. Default option in most states. |

With this side-by-side view, it’s easier to pinpoint where your dollars go and how much coverage truly matters.

Making An Informed Financial Decision

Ultimately, your premium mirrors the risk the insurer takes on. Stacking drives up rates because it exposes the company to a much larger potential payout.

For families with multiple cars, that extra premium often pays for peace of mind. You’ll rest easier knowing your policy can handle medical costs well beyond $50,000 or even $100,000.

Before you decide, run through this quick checklist:

- Number of vehicles on your policy and their individual limits

- Typical annual mileage and accident likelihood

- Premium difference between stacked and unstacked coverage

- Your state’s regulations on stacking UM/UIM limits

Think of it this way: Choosing stacked coverage is like buying extra financial armor. You hope you never need it, but if you do, it can be the one thing that prevents a devastating financial blow to your family.

Every household’s budget and risk tolerance are unique. If a single accident could drain your savings, the higher cost of stacked coverage could be a wise defensive move. These situations often lie at the heart of difficult personal injury claims where adequate protection is vital.

It’s also smart to explore understanding specific coverages like car key replacement insurance so you won’t face surprises after signing on the dotted line.

How To Choose The Right Option For Your Needs

Deciding between stacked and unstacked car insurance isn’t a plug-and-play decision. It’s about your household, your wallet, and how much risk you’re willing to shoulder. By running through a few targeted questions, you’ll move past theory and land on an option that actually eases your mind.

Assessing Your Household And Vehicle Situation

Begin with a simple inventory of your cars and drivers. The more vehicles—and the more people behind the wheel—the greater your exposure to an uninsured or underinsured motorist.

- How Many Vehicles Do You Insure? Stacked coverage only applies if you have two or more cars on one policy (or multiple policies under the same roof).

- Who’s Driving? Teens, spouses, roommates—each new driver nudges your accident probability higher.

- What Are Your Current UM/UIM Limits? If your limits fall short of covering a major injury claim, stacking could plug that gap.

If you check off several of these risk factors, stacked coverage starts to look like an important safety net rather than an extra cost.

Evaluating Your Financial Safety Net

Now, take a hard look at your finances. Remember: your auto policy’s UM/UIM coverage is meant to fill the holes that health insurance—and your savings—won’t cover.

“Health insurance might pay the hospital. But what about lost wages, rehab, or pain and suffering if you can’t work after a crash?”

Imagine a medical bill that overshoots an unstacked policy by $50,000. For many families, that gap could erase an emergency fund overnight. If your savings aren’t built to handle a six-figure surprise, paying a bit more each month for stacked coverage becomes a small, predictable expense in exchange for peace of mind.

State Laws That Affect Your Insurance Options

https://www.youtube.com/embed/xn7_wmTVpls

Your ability to choose between stacked and unstacked car insurance isn't a given; it's entirely dependent on where you live. State laws dictate whether you can stack your Uninsured/Underinsured Motorist (UM/UIM) coverage, creating a patchwork of rules across the country.

This geographic factor is the very first thing you need to check when considering your policy options. Some states, like Florida and Pennsylvania, permit stacking, giving drivers the option to create a much larger financial safety net. Others, however, have laws that completely prohibit it.

As an Atlanta-based firm, we know Georgia allows stacking, but this isn't universal. You can't assume what's true in one state holds for another.

Finding Your State's Insurance Regulations

Because these rules are so specific, the best approach is to go directly to the source. Official government websites are the only place to get completely accurate and up-to-date information for your location.

Start by locating your state's department of insurance. You can usually find it with a quick search, but the National Association of Insurance Commissioners (NAIC) also provides a helpful directory. Once you're on your state's official site, you'll find the detailed regulations on stacking UM/UIM coverage.

Understanding your state’s stance is the most important step in knowing your true coverage options. It determines whether the choice between stacked vs unstacked car insurance is even available to you.

It's also a smart move to be aware of other laws that influence your policy and potential claims. For example, knowing the details of Florida state driving laws can be just as important as your insurance choices.

Similarly, every state has a different time limit for taking legal action. Here in Georgia, understanding the statute of limitations for personal injury is another key piece of information that can make or break a case.

Common Questions We Hear About Insurance Stacking

As Atlanta personal injury attorneys, we spend a lot of time demystifying car insurance policies for our clients. The concept of stacked vs unstacked car insurance is a major source of confusion, but getting it right can dramatically impact your financial recovery after a crash.

Here are some of the questions we get asked most often.

Is Stacked Insurance More Expensive?

Yes, stacking your coverage will increase your premium. You are, after all, purchasing a much higher potential payout, which naturally increases the insurer's level of risk.

However, most drivers we talk to consider the slight cost increase a smart trade-off. It buys you significant peace of mind, knowing you have a much stronger financial safety net if you're ever hit by an uninsured or underinsured driver.

Can I Stack Insurance On Just One Car?

No, the principle of stacking only works when you insure two or more vehicles. The whole idea is to combine the coverage limits from multiple vehicles to create a larger pool of funds.

You can stack coverage "within" a single policy that covers multiple cars or "across" separate policies for vehicles in the same household, depending on your state's laws. If you only own one car, you can't stack—your best bet is to simply buy the highest Uninsured/Underinsured Motorist (UM/UIM) limit you can comfortably afford.

How Do I Know If I Have Stacked Coverage?

The fastest way to find out is to look at your policy's declaration page. This document should clearly state whether your UM/UIM coverage is "stacked" or "unstacked."

If the wording isn't clear, don't guess. A quick call to your insurance agent will get you a firm answer. For more official guidance, the Georgia Office of Insurance is an excellent resource for consumers.

Ultimately, choosing between stacked vs unstacked car insurance comes down to a simple calculation: balancing a small, certain cost today against the potential for much greater protection if the unexpected happens.

If you or someone you love was injured in an accident and you're now facing a difficult insurance claim, Jamie Ballard Law is ready to step in. Contact our office for a free, no-obligation case evaluation to get clear on your rights and your next steps. https://jamieballardlaw.com