As an Atlanta Personal Injury attorney, I've handled far too many cases where a car accident with an uninsured driver becomes a financial nightmare. This is exactly why your own insurance policy’s protections are so important. A key decision you'll face is choosing between stacked vs unstacked uninsured motorist coverage.

So, what's the difference? In simple terms, unstacked coverage gives you a fixed protection limit tied only to the vehicle involved in the crash. Stacked coverage, however, lets you combine the uninsured motorist (UM) limits from multiple vehicles on your policy. This creates a much larger financial safety net when you need it most.

Understanding Your Core Coverage Options

When you buy auto insurance, you're building a financial shield. A vital piece of that shield is your Uninsured/Underinsured Motorist (UM/UIM) coverage, which steps in when the at-fault driver has no insurance—or not nearly enough to cover your damages. The distinction is important, as an alarming number of drivers on the road simply can't pay for the accidents they cause.

The insurance jargon can be a headache, but getting a handle on it is the first step toward making a smart choice. If you ever get stuck on a term, our firm's legal dictionary offers clear, straightforward definitions.

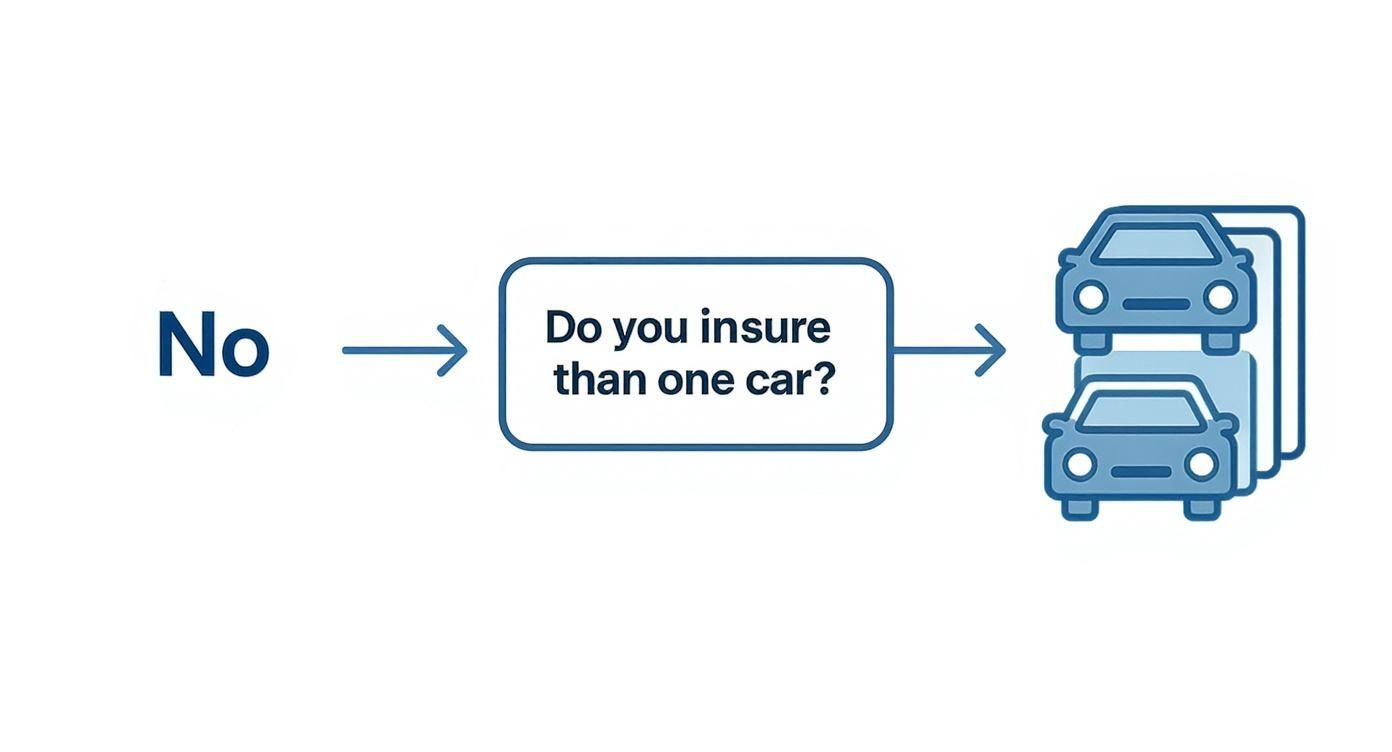

This simple decision tree breaks down the main factor that determines if stacking is even an option for you.

As the visual shows, the moment you insure more than one car, you unlock the powerful option to stack your coverage.

Comparing Stacked and Unstacked UM Policies

Putting these two options side-by-side really clarifies the differences. Each offers a distinct level of protection at a different price point.

To make things even clearer, here’s a quick breakdown of how these two policy types stack up.

Stacked vs Unstacked UM Coverage at a Glance

| Feature | Unstacked UM Coverage | Stacked UM Coverage |

|---|---|---|

| Coverage Limit | Capped at the limit for the single vehicle in the accident. | Combines the limits from all vehicles on your policy for a higher total. |

| Ideal For | Households with only one insured vehicle. | Households insuring two or more vehicles seeking maximum protection. |

| Premium Cost | Generally lower, making it a more budget-friendly choice. | Typically higher, but often a modest increase for a large boost in coverage. |

| Protection Level | Provides a fixed, basic layer of financial protection. | Offers a significantly larger financial safety net for serious accidents. |

This isn't just a theoretical exercise. The reality is that many drivers could be a major financial risk if they hit you. For example, statistics from the Insurance Information Institute show that about 1 in 8 drivers on the road are completely uninsured.

Ultimately, picking the right coverage is about balancing cost with your need for real security. Carefully evaluating the stacked vs unstacked uninsured motorist options is an important step in making sure you and your family are properly protected on the road.

How Stacked Uninsured Motorist Coverage Works

Before you can decide between stacked vs unstacked uninsured motorist coverage, it's helpful to understand how stacking actually functions on a practical level. Think of it as pooling your own insurance resources to create a much stronger financial safety net. This option is available exclusively to people who insure more than one vehicle on the same policy.

Stacking lets you combine the uninsured motorist (UM) coverage limits from each vehicle you insure. This creates a single, larger fund that you can draw from if you are injured by a driver who has no insurance or flees the scene after a hit-and-run.

A Practical Example of Stacking

Let’s break this down with a real-world scenario. Imagine you live in Atlanta and have two cars insured on a single policy.

- Car A: Has $50,000 in Uninsured Motorist Bodily Injury (UMBI) coverage.

- Car B: Also has $50,000 in UMBI coverage.

With a stacked policy, you don't just have $50,000 available. Instead, you add the limits together. This gives you a total of $100,000 in UMBI coverage that you can access, no matter which car you were driving during the accident.

The real power of stacking is its flexibility. This combined coverage protects you not only when you're driving one of your insured cars but also if you're a passenger in someone else's vehicle or even if you are hit as a pedestrian.

Where Does Stacked Coverage Apply?

One of the most common questions I hear is when this pooled coverage can actually be used. The protection follows the people insured on the policy, not just the vehicles. This means you are generally covered in various situations, including:

- Driving any of the vehicles listed on your policy.

- Riding as a passenger in a friend or family member's car.

- While walking or cycling, if you are struck by an uninsured driver.

This broad protection is a key reason why many families with multiple vehicles opt for stacking. It addresses the reality that an accident can happen anytime, anywhere. After a serious collision, medical bills and lost wages escalate quickly, so having a larger pool of funds can make a significant difference. If you're exploring your options after an accident, understanding the full scope of different personal injury claims can provide valuable context.

Ultimately, choosing a stacked policy is a strategic move to maximize the value of the premiums you're already paying for multiple vehicles. It’s an effective way to leverage your full insurance policy for the worst-case scenario, which is a key part of the stacked vs unstacked uninsured motorist decision.

How Unstacked Uninsured Motorist Coverage Works

When you're weighing stacked vs unstacked uninsured motorist coverage, the unstacked option is the simpler of the two. Think of it as a distinct layer of protection assigned to each specific vehicle you insure. What you see on the declarations page for one car is exactly what you get for that one car—period.

With an unstacked policy, your coverage is capped at the amount listed for the particular vehicle involved in the crash. It makes no difference if you insure two, three, or even more cars on that same policy; you simply cannot combine or "borrow" the coverage from the other vehicles.

Understanding the Coverage Limits

The foundational principle of unstacked insurance is that each vehicle’s coverage stands entirely on its own. This strict separation is the key takeaway when you're reviewing your policy documents.

Let’s walk through a quick, practical example:

- You own three vehicles, all insured under a single household policy.

- Each vehicle carries a $50,000 unstacked uninsured motorist (UM) limit.

- While driving one of these cars, you are hit and injured by a driver with no insurance.

In this scenario, the absolute maximum you can recover from your own insurer is $50,000—the limit tied to the specific car you were in. The UM coverage on your other two vehicles is completely off-limits, leaving you with a firm ceiling on your potential recovery.

With unstacked coverage, what you see is what you get. The policy limit for the vehicle involved in the accident is the absolute maximum you can recover under your UM coverage, regardless of how many other vehicles you insure.

Why Choose an Unstacked Policy

The main draw for an unstacked policy is almost always the price. Since the insurance company’s maximum exposure is confined to one vehicle's limit per incident, the premiums are usually lower than they are for stacked coverage. This can make it a sensible choice for drivers on a tight budget or for households that only have one car to insure.

But that lower premium comes with a significant trade-off. It buys you a fixed amount of financial protection that won't grow as you add more vehicles to your policy. Understanding this limitation is non-negotiable when you’re making the final call on stacked vs unstacked uninsured motorist coverage.

Real-World Scenarios: Stacked vs. Unstacked Policies in Action

Policy language can feel abstract until you see how it works in a real crash. The difference between stacked vs. unstacked uninsured motorist coverage isn't just jargon—it has a direct impact on your financial recovery after an accident. Let’s break it down with a clear, practical example.

When an accident happens, your first priorities are safety and evidence. Knowing the steps to take immediately after an accident is important, as the documentation you gather at the scene can become vital for your UM claim.

An Atlanta Hit-and-Run Example

Picture this: an Atlanta family has two cars insured on the same policy, and they carry $100,000 in uninsured motorist bodily injury (UMBI) coverage on each vehicle. One night, a hit-and-run driver causes a severe collision, leaving the policyholder with $150,000 in medical expenses and lost wages.

How does their insurance respond? It all depends on whether their policy is stacked or unstacked.

- With an Unstacked Policy: The insurance company will only pay up to the $100,000 limit for the specific car involved in the crash. This leaves the family with a staggering $50,000 in bills they have to cover out of pocket.

- With a Stacked Policy: The family can combine, or "stack," the UMBI limits from both of their cars. Their $100,000 limit becomes a $200,000 total pool of coverage. This is more than enough to cover the full $150,000 in damages, leaving them with no medical debt from the incident.

This scenario makes it obvious how stacking transforms a standard multi-car policy into a powerful financial safety net, particularly when injuries are serious.

The Growing Risk of Uninsured Drivers

This isn't just a theoretical problem. The danger posed by uninsured drivers is real and something to be aware of. The rate of uninsured motorists can fluctuate, meaning the odds of being hit by someone without proper insurance are always a concern for responsible drivers.

In a serious accident, the difference between having your damages fully covered and facing tens of thousands of dollars in debt often comes down to the simple choice you made between a stacked and unstacked policy.

At the end of the day, you're looking at a classic trade-off. An unstacked policy might shave a few dollars off your premium, but a stacked policy provides a level of financial security that can be priceless. When you view the stacked vs. unstacked uninsured motorist decision through the lens of a real-world crash, the right choice for your family becomes much clearer.

Making the Best Choice for Your Georgia Policy

Ultimately, deciding between stacked vs unstacked uninsured motorist coverage boils down to your personal circumstances, your budget, and the level of financial risk you're willing to accept. Every family's needs are different, so a perfect fit for one household may not work for another.

The good news is that Georgia law puts the power in your hands. Insurers are required to offer you Uninsured/Underinsured Motorist (UM/UIM) coverage when you purchase a policy. If you insure more than one vehicle, you have the right to choose stacking, giving you direct control over your financial protection.

Key Factors to Consider

Before you decide, take a hard look at your own situation. A few key areas will tell you how much coverage you might realistically need after a serious collision.

- Number of Vehicles: This is the most direct factor. If you only own a single car, stacking isn't an option. But if you have multiple vehicles, stacking becomes a powerful way to multiply your available coverage.

- Health Insurance Coverage: What do your health plan's deductibles, copays, and out-of-pocket maximums look like? A high-deductible plan could leave you facing overwhelming medical bills, making the higher UM limits from a stacked policy incredibly valuable.

- Your Budget: Yes, stacked coverage costs more. But the premium increase is often surprisingly small for the massive jump in protection it offers. Always ask your agent for a direct quote comparing both options side-by-side.

For most Atlanta households with two or more cars, stacking provides a much larger safety net for a relatively modest increase in cost. It’s an investment in your financial security on the road.

Situational Recommendations

Your choice should align with your real-world risks. For families with multiple cars—especially those with young drivers on the policy—stacking provides an essential layer of security. The more family members you have on the road, the higher your collective risk of an accident with an uninsured driver becomes.

If you own a single vehicle, your focus shifts. Instead of choosing between stacking options, your goal is to select an unstacked UM limit that's high enough to cover potential medical bills and lost wages. Make sure your limits are adequate to protect your assets. An accident happens in an instant, but the consequences, including legal deadlines for taking action, can last for years. Understanding the Georgia statute of limitations for personal injury is a vital part of protecting your rights.

I always recommend having a frank conversation with your insurance agent. Ask them to show you the exact price difference and coverage amounts for a stacked vs unstacked uninsured motorist policy. Seeing the numbers clearly will give you the information you need to make the best choice for you and your family.

Frequently Asked Questions About UM Coverage

As Atlanta personal injury attorneys, we've heard just about every question there is when it comes to insurance. The discussion around stacked vs unstacked uninsured motorist coverage, in particular, always brings up some important, real-world concerns. Here are the most common questions clients ask and the direct answers you need to know.

Is Stacked Coverage Much More Expensive?

While a stacked policy does come with a higher premium, the increase is often far more reasonable than most people assume. When you weigh the small cost against the massive jump in financial protection it provides, many Georgia drivers decide the peace of mind is easily worth it.

The only way to know for certain is to ask your insurance provider for a direct quote. Have them show you the exact price difference between a stacked and an unstacked policy for your specific vehicles. That simple comparison often makes the value crystal clear.

Can I Stack Coverage From Different Insurance Policies?

No, and this is a major point of confusion for many drivers. Stacking is designed exclusively to combine the Uninsured Motorist (UM) coverage from multiple vehicles insured under a single auto insurance policy.

You cannot take the UM coverage from your policy with one company and combine it with a separate policy from another. This is one of the main reasons it's a smart move to keep all your family's vehicles insured with the same carrier—it simplifies everything and actually enables you to stack your protection.

Remember, stacking combines limits within one policy. It does not permit you to pool coverage from entirely separate insurance contracts or companies.

What Are My Options If I Only Own One Car?

If you insure just one vehicle, stacking isn't an option. There are simply no other UM limits on the policy to combine with your own, so your policy is considered unstacked by default.

For single-car owners, the goal is to choose a UM coverage limit high enough to shield you from catastrophic medical bills and lost wages. A solid rule of thumb is to select a UM limit that is at least equal to your own bodily injury liability limits. This ensures you’re giving yourself the same level of protection you’re required to provide for others. You can find more state-specific guidance at the Georgia Office of Insurance and Safety Fire Commissioner's website.

Does Georgia Law Require Uninsured Motorist Coverage?

This is a very important question. Under Georgia law (O.C.G.A. § 33-7-11), insurance companies must offer you UM coverage. However, accepting or rejecting it is ultimately your choice—you have the right to decline this coverage in writing.

Frankly, with so many uninsured drivers on our roads, I strongly advise every client against rejecting this protection. Your UM coverage is one of the most valuable parts of your auto policy, serving as your primary financial backstop against someone else's irresponsibility. Making the right choice on stacked vs unstacked uninsured motorist coverage is one of the most important financial decisions you can make for your family's safety.

If you've been hurt in an accident and are fighting to make sense of your insurance options, you don't have to go through it alone. We offer free, no-obligation case evaluations to help you understand your rights and the coverage you are entitled to. Contact us 24/7 to get the clear answers you deserve.