After an accident, your top priority is getting your medical bills paid. Often, your own insurance company steps up to cover those initial costs. Around this time, you'll probably hear a new term: subrogation. So, what is a subrogation claim?

Simply put, it’s the legal right your insurer uses to get back the money it paid for your care from the at-fault party’s insurance company.

Your Simple Guide to Understanding Subrogation

Think of it this way: you and a friend go out for lunch, but the person who was supposed to pay forgot their wallet. Your friend covers your bill. Later, your friend gets that money back directly from the person who was originally responsible. That’s subrogation in a nutshell.

This might seem like a behind-the-scenes issue between insurance companies, but it directly impacts the final settlement you receive. That's why having a solid grasp of how it works is so important for anyone with a personal injury case.

The entire process is designed to hold the responsible party financially accountable. At its core, subrogation allows an insurer to "step into your shoes" after it has paid your bills to pursue the party that actually caused the harm.

The key players in this process are fairly straightforward. Let's break down who does what.

Key Players in a Subrogation Claim

This table outlines the main parties involved and clarifies their specific roles.

| Party | Role in the Subrogation Process |

|---|---|

| The Insured (You) | The person who was injured and received initial payment from their own insurer for medical bills or property damage. |

| Your Insurer | The company that paid your initial claim and now seeks reimbursement from the at-fault party's insurer. |

| The At-Fault Party | The individual or entity legally responsible for causing the accident and your injuries. |

| At-Fault Party's Insurer | The company that provides liability coverage for the at-fault party and is ultimately responsible for paying the subrogation claim. |

Understanding these roles helps you see where you fit in and why your insurer is now dealing with the other driver's company.

Interestingly, insurance companies don't always follow through with this process. Subrogation is a financial recovery tool, but studies show that a surprising 91% of insurers pursue less than 30% of their potential subrogation cases. You can read more about these subrogation study findings and see why so much money is left on the table.

This fact is important for you. It shows that even large insurance companies don’t always succeed in recovering every dollar. Knowing the basics of what a subrogation claim is and how it functions is the first step toward protecting your settlement and making sure you aren't left shortchanged.

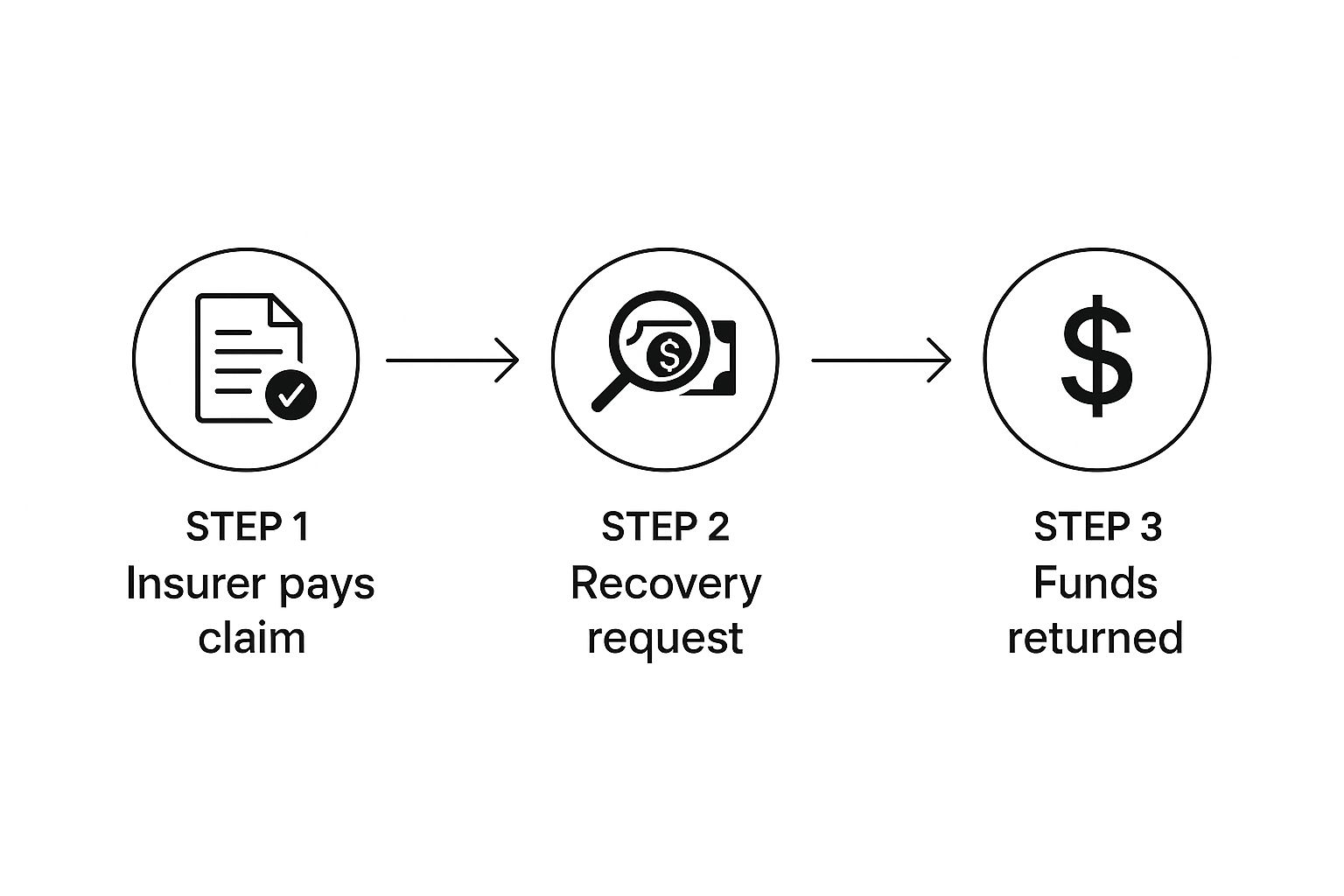

How Subrogation Works Step by Step

Let's walk through what the subrogation process actually looks like from your perspective after an injury in Atlanta. When you know what’s happening, the process feels much more manageable. While every case has its own unique details, most follow a predictable path.

Here’s how it usually unfolds:

-

Your Insurer Pays First: After an accident, your only job is to get the medical care you need. To prevent delays in treatment, your own health insurance or your car insurance’s Medical Payments (MedPay) coverage will step in to pay your initial hospital and doctor bills. This gets you immediate help without waiting for the at-fault party to pay.

-

You File Your Personal Injury Claim: Next, your attorney will file a personal injury claim against the person or company responsible for your injuries. This is the formal legal action where we seek full compensation for all your damages—including medical expenses, lost wages, and pain and suffering.

-

The Insurer States Its Claim: As soon as your insurance company finds out you’ve filed a claim, it will send a formal “notice of subrogation” or a “lien” to the at-fault party’s insurer. This is simply a legal notice informing them that your insurer has a right to be repaid from any settlement or verdict you receive. This is standard procedure and not a cause for alarm.

-

The Settlement Payout: Finally, once your case settles or you win at trial, your insurer's subrogation claim gets paid directly out of those funds. This happens before you receive the final balance. A key part of our job is to manage this step carefully, ensuring every dollar is handled according to Georgia law and negotiating that lien down whenever possible.

This visual shows the basic flow from the insurer's initial payment to the final recovery of funds.

As the infographic shows, subrogation is essentially a repayment cycle. Its purpose is to put the financial responsibility back where it belongs: on the at-fault party's insurer. Remember, this entire procedure is a normal part of any personal injury claim. Our goal is to make it as transparent as possible for you so you can focus on your recovery.

Common Types of Subrogation You May Encounter

The idea of subrogation isn't just a legal footnote; it shows up across several types of insurance, especially after an accident. When one insurance company pays out for damages that someone else was responsible for, they will want to get that money back. That's the core of subrogation.

It's a standard part of the insurance world, but it doesn't always happen. Insurers are surprisingly busy, and it's estimated that around 15% of all insurance claims are closed without anyone spotting a valid subrogation opportunity. You can learn more about how these missed subrogation numbers impact the industry. This detail alone shows why it’s so important to understand how the process works from your end.

Health and Auto Insurance Subrogation

For most personal injury clients, this is where subrogation becomes real. It's the most frequent type you'll run into.

-

Health Insurance Subrogation: If you're hurt in a car wreck or a slip-and-fall, you'll naturally use your health insurance to cover the immediate medical bills. Let’s say your health plan pays $25,000 for your surgery and hospital stay. Your health insurer then has a legal right to get that $25,000 back from the at-fault party's insurance. They do this by filing a subrogation claim.

-

Auto Insurance Subrogation: This one often involves your own auto policy. For instance, if your insurer pays your medical bills through a MedPay provision or covers your car repairs because the other driver was uninsured (Uninsured/Underinsured Motorist coverage), it will turn around and pursue the person who caused the accident to recover what it paid.

Workers’ Compensation Subrogation

This type of subrogation is a bit different. It applies only to injuries that happen on the job but were caused by a third party—meaning, not your employer or a coworker.

For example, imagine you're a delivery driver and a distracted driver runs a red light, hitting your truck. Your employer's workers' compensation insurance will immediately cover your medical treatment and lost wages. But because a separate, negligent driver caused your injuries, the workers' comp insurer can then file a subrogation claim against that driver's auto insurance to get back every dollar it paid out for your care.

How a Subrogation Claim Affects Your Final Settlement

This is one of the most common questions we get from clients: “If subrogation is just between the insurance companies, how does it end up costing me money?” The answer is unfortunately quite direct. A subrogation claim is paid straight from your total settlement award.

It's not a separate bill the at-fault party's insurer pays on the side. Think of it as a lien that gets first priority when your settlement check comes in.

Let’s use a quick example. Imagine your case settles for $100,000. If your health insurer paid $30,000 for your medical care, they now have a valid subrogation lien for that amount. That $30,000 must be repaid directly out of your $100,000 settlement, which significantly reduces the final amount you take home.

How We Protect Your Bottom Line

This is exactly where having an experienced Atlanta personal injury attorney makes a huge difference. A key part of our job is to challenge and actively negotiate these subrogation liens. Insurers almost always send an initial demand for the full amount they paid out, but that number is rarely set in stone.

The initial subrogation demand is just a starting point for negotiations. Our goal is to drive that number down as low as possible, because every single dollar we save you on the lien is another dollar that goes directly into your pocket.

We have several strategies for getting that lien reduced. We can point out weaknesses in the other side’s case, account for attorney’s fees and litigation costs, or make a strong argument for fairness based on the limits of your total recovery. This process turns what looks like a fixed debt into a real opportunity to boost your net settlement.

The first step is always a thorough review of your insurance policy's specific language. You can often find these details on your provider’s website or in consumer guides from state resources like the Georgia Office of Insurance. Understanding these terms is foundational. Successfully negotiating a subrogation claim is a key service that directly and powerfully impacts your final take-home recovery.

Understanding a Waiver of Subrogation

In some contracts, you might see a clause called a waiver of subrogation. It sounds like dense legal language, but the concept is actually pretty straightforward. It's a contractual promise where one party agrees to give up their insurance company's right to sue another party for a loss they caused. You can learn more about the legal principle from non-biased sources like Wikipedia.

You'll see these waivers all the time in commercial leases and construction contracts, though they can pop up elsewhere. When you sign one, you’re telling your insurer that if the other party is responsible for damages, your insurance company can't go after them to get its money back.

Think of it this way: a landlord often requires a tenant to sign a waiver of subrogation. If that tenant's employee then starts a fire that damages the building, the waiver stops the landlord's property insurance company from suing the tenant to recover the money it paid out for repairs.

A waiver of subrogation is designed to stop the repayment cycle before it even starts. It’s a pre-emptive block on what would otherwise be a standard what is a subrogation claim.

Insurers globally are paying very close attention to subrogation's financial impact. The subrogation market was valued at USD 523.1 million in 2023 and is projected to grow. Still, billions in potential recoveries are missed every year. You can learn more about insurance claims market trends to see just how much is at stake for these companies.

Because signing a waiver permanently changes your rights—and your insurer's—it's always a good move to have an attorney look over any document with this clause before you put your name on it.

Frequently Asked Questions About Subrogation

As Atlanta personal injury attorneys, we field a lot of questions about how insurance policies and settlements really work. To provide some clarity, here are straightforward answers to the most common questions our clients ask us. Understanding if you can simply say "no" is just as important as knowing what is a subrogation claim in the first place.

Can I Tell My Insurance Company Not to Pursue Subrogation?

Generally, no. Your insurance policy is a legally binding contract. That contract almost certainly includes a subrogation clause giving your insurer the right to recover money it pays out on your behalf.

Trying to block your insurer from exercising this right would likely be considered a breach of your contract. A much better approach is to have your attorney work directly with the insurer to ensure the process is handled fairly and that your financial interests are protected.

Do I Have to Pay the Lien if My Settlement Is Not Enough?

This is a key issue where specific state laws, especially Georgia’s, become very important. In our state, a legal principle known as the “made whole doctrine” is a powerful tool for injured victims. You can find more information on consumer rights in guides from the Georgia Office of Insurance and Safety Fire Commissioner.

The made whole doctrine establishes that your insurance company cannot collect its subrogation lien until you have been fully compensated for all your losses. This includes not just medical bills and lost wages, but also your pain and suffering.

An attorney's job is to build a strong argument showing that the settlement is not enough to make you whole. This can legally shield your recovery from being reduced by the insurer's lien.

Can My Lawyer Get the Subrogation Amount Reduced?

Yes, absolutely. Negotiating to reduce subrogation liens is a fundamental and high-value service a good personal injury lawyer provides. We don't just accept the initial demand letter the insurance company sends over.

We can successfully argue for a reduction based on several factors, including:

- Your percentage of fault (if any)

- Weaknesses in the at-fault party's case

- Simple appeals to fairness and equity

Every single dollar we get an insurer to knock off their lien is another dollar that goes directly into your pocket.

What Happens if I Ignore the Subrogation Notice?

Ignoring a subrogation notice is never a good idea. The insurance company holds a clear legal right to be repaid and can take direct legal action against you or the at-fault driver’s insurer to get its money.

This will only delay your settlement and can create serious legal headaches for you down the line. The best path forward is always to let your attorney manage all communications about what is a subrogation claim and its related liens to ensure everything is resolved correctly and in your favor.

If you've been injured and are now facing demands from insurance companies, you don't have to face it alone. The team at Jamie Ballard Law is here to protect your rights and fight to maximize your recovery. For a free, no-obligation case evaluation, contact us today at https://jamieballardlaw.com.