When you’ve been hurt on someone else’s property, the first question on your mind is usually, "What is my case actually worth?" As an Atlanta personal injury attorney, I get this question a lot, and I believe in giving you a straight, honest answer. The reality is, there's no magic number or a single "average" for premises liability settlement amounts. I've handled cases that settled for a few thousand dollars for a minor sprain and others that exceeded a million dollars for life-altering injuries.

What Is a Typical Premises liability Settlement Amount?

The final value of your case hinges entirely on the unique facts of your situation. A settlement isn't a number pulled out of thin air; it's a carefully calculated amount meant to cover every single one of your losses, both financial and personal. Think of it as a way to rebuild what was taken from you because a property owner was negligent.

This includes every dollar you’ve spent on medical care, the paychecks you missed while you were out of work, and the very real, personal toll of your pain and suffering. To really grasp what a settlement represents, it helps to know the legal duty property owners have. Under the law, owners must keep their property in a reasonably safe condition for visitors. You can dig deeper into these legal duties through resources like the Legal Information Institute at Cornell Law School.

Breaking Down the Building Blocks of a Settlement

To see how a final settlement number comes together, you have to look at all the individual pieces that build it. In legal terms, these pieces are called "damages," which is just a formal word for the losses you've suffered. They generally fall into two main buckets: economic damages and non-economic damages.

- Economic Damages: These are the straightforward, calculable costs. They have a clear dollar amount attached and include things like hospital bills, surgery costs, physical therapy sessions, and any income you lost because you couldn't work.

- Non-Economic Damages: This category is much more personal and, frankly, harder to put a price tag on. It’s meant to compensate you for your physical pain, emotional trauma, and the overall negative impact the injury has had on your day-to-day life.

The table below breaks down these core components in a bit more detail.

Key Components of a Premises Liability Settlement

| Damage Type | Description & Examples |

|---|---|

| Medical Expenses | Covers all past and future medical care tied to your injury. This includes everything from the initial ER visit and doctor's appointments to prescription drugs, surgery, and physical rehabilitation. |

| Lost Wages | Reimburses you for the income you lost while you were unable to work. This can also cover the loss of future earning capacity if your injury causes a long-term or permanent disability. |

| Pain and Suffering | Accounts for the physical pain, discomfort, and emotional distress the injury caused. This is a non-economic damage that acknowledges the human cost of the accident. |

| Property Damage | If any of your personal belongings were damaged in the incident—think a broken phone, laptop, or glasses—the cost to repair or replace them can be included in your claim. |

Getting a handle on these components is the first and most important step in understanding what your unique case might truly be worth. Each of these elements is documented, calculated, and argued to build a complete and compelling picture of your losses, which is what ultimately determines the final premises liability settlement amounts.

The Most Important Factors That Shape Your Settlement

Figuring out a potential premises liability settlement amount isn’t a simple calculation. It’s more like building a case brick by brick, where every piece of evidence adds to its strength and value. No two injury claims are the same, so no two settlements will ever be identical.

Think of it this way: your case's value is a story told through evidence. Each factor we'll discuss is a chapter, and the strength of one chapter builds on the next. As an Atlanta personal injury attorney, I see every day how these specific elements directly impact the final negotiation.

To get a realistic idea of what your claim might be worth, you have to understand what insurance adjusters and juries look at when they put a number on a case.

The Severity and Nature of Your Injuries

This is the anchor of your entire claim. The foundation of any personal injury case is the harm you suffered. A sprained ankle that heals in six weeks is valued completely differently than a shattered hip that requires surgery and leaves you with a permanent limp.

The more serious the injury, the higher the settlement value. That's because severe injuries create a massive ripple effect across your life, leading to:

- Extensive Medical Treatment: This covers everything from the ambulance and emergency room visit to surgeries, physical therapy, pain management, and prescriptions.

- Future Medical Needs: A fair settlement must account for the care you'll need down the road. This could mean future operations, in-home nursing care, or specialized medical equipment.

- Permanent Impairment or Disfigurement: If an injury leaves you with a lasting disability, chronic pain, or significant scarring, the settlement must reflect that permanent loss of quality of life.

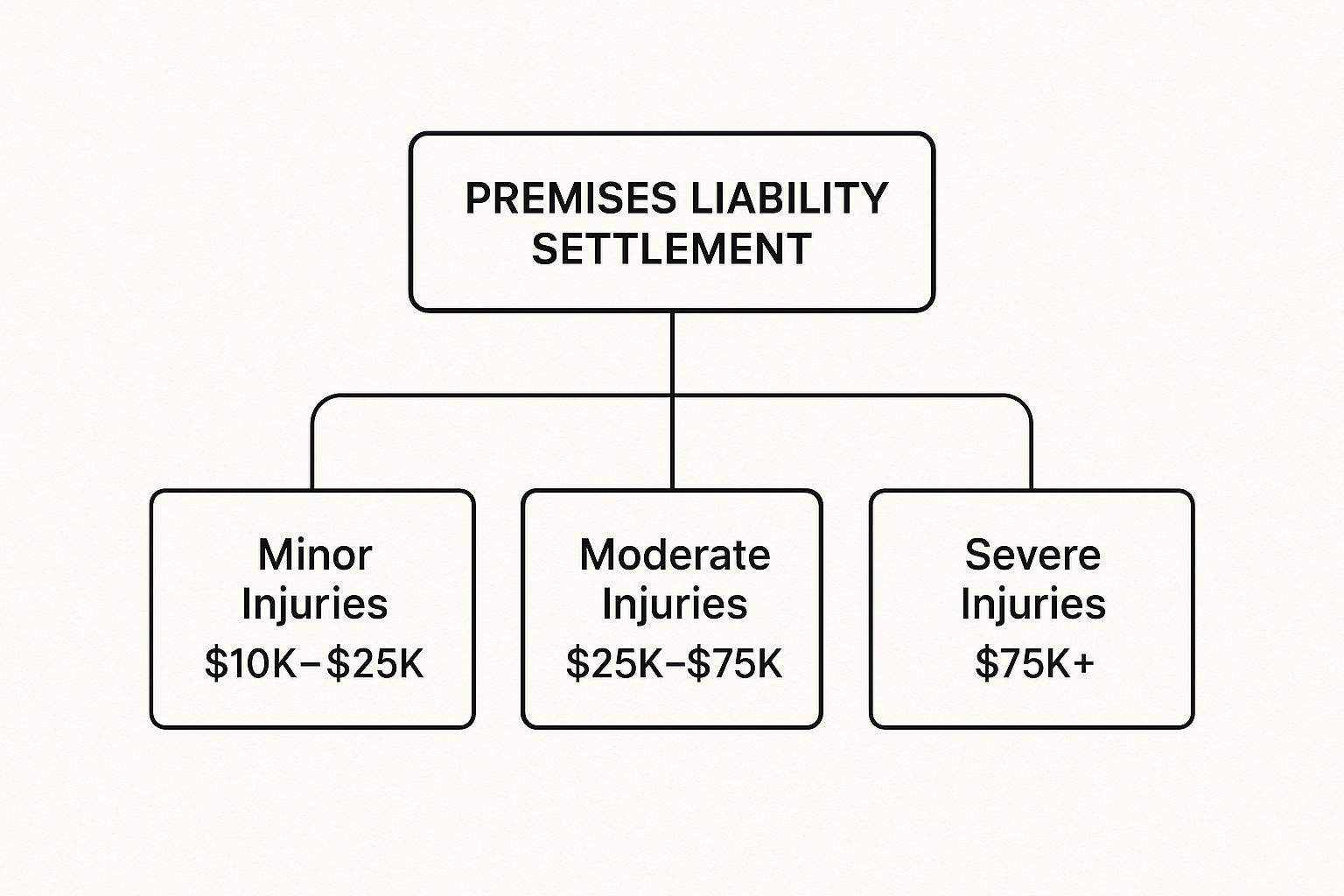

This infographic shows just how much settlement ranges can vary based on how badly you were hurt.

As you can see, a catastrophic injury claim can be worth many times more than a minor one. This factor is absolutely central to the final calculation.

Total Economic Damages Documented

After the injury itself, the next piece of the puzzle is your documented financial losses. These are the concrete, calculable costs that are tied directly to the accident. We refer to these as "economic damages."

A strong claim is built on a foundation of clear documentation. Every bill, receipt, and pay stub helps to tell the financial story of your injury and justify the compensation you are seeking.

The primary components of economic damages include:

- Medical Bills: This is the running total of every single cost related to your medical care. It includes not just big-ticket items like surgery but also ambulance fees, co-pays, diagnostic tests like MRIs, and prescriptions.

- Lost Income and Wages: This calculation covers the paychecks you missed while you were out of work recovering. If you had to burn through sick days or vacation time, that lost benefit is part of the claim, too.

- Loss of Earning Capacity: This is an important one. If your injury prevents you from returning to your old job or limits your ability to work in the future, your settlement must compensate you for that lost earning potential over your entire working life.

Strength of Evidence and Fault

Finally, the strength of your case is make-or-break. You have to prove the property owner was negligent and that their negligence was the direct cause of your injuries. Strong evidence makes a strong case. This includes things like photos of the hazard, surveillance video, witness testimony, and reports from safety experts.

Georgia’s laws on shared fault also play a massive role. Under our state's "modified comparative negligence" rule, you can still recover damages as long as you are found to be less than 50% at fault. However, your final award gets reduced by your percentage of fault. For example, if you were awarded $100,000 but a jury found you 10% responsible, you would receive $90,000.

You can read the official statute yourself at O.C.G.A. § 51-12-33. But the bottom line is key: if you are found 50% or more at fault, you get nothing. All these factors combine to paint the full picture and ultimately determine the final premises liability settlement amounts.

How Long Does a Premises Liability Case Take to Settle?

Here in Atlanta, one of the first questions I always get is, "How long is this all going to take?" It's a completely fair question. Your life has been turned upside down, and you need to know what to expect. The answer is tied directly to the very same factors that drive premises liability settlement amounts.

There's a clear relationship between the time it takes to resolve a case and what it’s ultimately worth. It might sound strange, but a longer timeline is often a good thing for your claim. This isn't about dragging things out for no reason; it's about being thorough.

Why Rushing Can Cost You

When medical bills are piling up and you're out of work, the temptation to grab the first offer an insurance company dangles in front of you is immense. I get it. But this is almost always a mistake. Quick settlements usually mean you're leaving a lot of money on the table.

A fast deal rarely captures the full, long-term picture of an injury. It takes time for you and your doctors to truly understand the extent of your medical needs. Will you need another surgery down the road? Could arthritis develop in that injured joint? Will you have to manage lifelong pain? Answering these questions is essential to securing a settlement that actually covers your losses.

Rushing to settle before you’ve reached what doctors call "Maximum Medical Improvement" (MMI) is like guessing what your future looks like. A proper settlement is built on facts, not guesswork.

MMI is the point where your condition has stabilized and a doctor can reasonably predict what future care, if any, you'll need. Getting to that point takes time, but it’s the only way to make sure your settlement accounts for all your future medical bills.

Timelines Based on Injury Severity

The single biggest factor dictating how long your case will take is how badly you were hurt. A claim for a minor injury might wrap up fairly quickly. A case involving a catastrophic injury will, without a doubt, take much longer.

This isn't an arbitrary delay. It’s a necessary part of the process to document every single loss you've suffered. The data shows this connection clearly. For instance, recent studies show a direct link between injury severity and the time needed to settle.

- Minor injuries like cuts or sprains may resolve in about 10 to 13.5 months.

- Moderate injuries, such as broken bones, often push the timeline to 12-16 months.

- Severe injuries—think spinal cord damage or traumatic brain injuries—can take from 33 to 48 months or even longer.

You can learn more about how timelines correlate with personal injury case values from recent studies on case duration.

This extended timeframe is important. It gives your legal team the time needed to conduct a deep investigation, gather all the evidence, and build the strongest possible case for liability against the property owner. It also allows for a precise calculation of all lost wages and, most importantly, any future loss of your ability to earn a living.

Ultimately, patience in a premises liability case isn't just a virtue—it's a strategy. A longer timeline usually means your legal team is meticulously building a case designed to secure the full and fair premises liability settlement amounts you deserve.

A Look at Real-World Settlement Ranges

While every injury claim has its own unique facts, looking at real-world examples can give you a better feel for potential premises liability settlement amounts. It's important to understand that these aren't guarantees; they are illustrations based on data and my experience as an Atlanta personal injury attorney. Think of them as a ballpark estimate—the final outcome always depends on the specific details of your case.

The value of a case is directly tied to the severity of the injury and its impact on a person's life. We can generally group these into three broad categories to see how settlement values shift.

Settlements for Minor Injuries

For injuries considered "minor," settlements typically fall on the lower end of the spectrum. These are injuries that, while painful and disruptive, usually heal completely within a few weeks or months without long-term consequences.

Examples of minor injuries include:

- Soft tissue sprains and strains, like a twisted ankle or a strained back.

- Minor cuts and bruises that require minimal medical attention.

- Injuries causing you to miss a short amount of work but not affecting your future earning capacity.

For these types of cases, settlements often land in the $10,000 to $50,000 range. This amount is calculated to cover initial medical bills, any lost wages, and compensation for the pain and inconvenience you experienced.

Payouts for Moderate Injuries

When an injury is more significant and has a greater impact on your life, the settlement value increases accordingly. "Moderate" injuries are those that often require more intensive medical treatment, like surgery, and might involve a longer, more difficult recovery.

These can include:

- A broken bone (fracture) that needs a surgical procedure to set correctly.

- A herniated disc in the back or neck causing ongoing pain.

- Second-degree burns requiring specialized care.

- Injuries resulting in some form of temporary or partial disability.

Settlements for moderate injuries can range from $75,000 to $500,000, and sometimes higher. This broader range reflects the wide variety of injuries in this category and the significant differences in medical costs and recovery times.

Compensation for Severe and Catastrophic Injuries

This category represents the most serious and life-altering injuries. When an accident results in permanent disability, disfigurement, or requires lifelong medical care, the settlement must reflect that immense loss.

These aren't just about covering bills; they are about providing financial security for a lifetime of challenges. A catastrophic injury changes everything, and the settlement's job is to acknowledge that reality.

Severe injuries can include traumatic brain injuries (TBIs), spinal cord damage leading to paralysis, amputations, or severe burns. In these situations, settlements can easily exceed $500,000 and often reach into the millions of dollars. The final amount is designed to cover not just past and future medical care, but also the costs of in-home assistance, home modifications, and the profound loss of quality of life.

Data from other large markets, like New York City, shows similar patterns. For example, in fiscal year 2023, the average personal injury payout was $134,656, with the most severe cases reaching over $2.3 million. You can find more details in the report from the NYC Comptroller's Office. While this isn't Atlanta, it helps show how dramatically premises liability settlement amounts scale with the severity of the harm done.

How Rising Jury Verdicts Can Affect Your Settlement

When you're hurt on someone else's property, your case doesn't exist in a vacuum. It's influenced by a much larger legal landscape, and one of the biggest trends right now is the rise of what legal insiders call "nuclear verdicts."

These are jury awards that are shockingly large—often running into the tens or even hundreds of millions of dollars. While they make headlines, their real impact isn't just in the courtroom. It sends a powerful ripple effect across the entire personal injury world, influencing how even smaller cases are negotiated and settled.

The Ripple Effect of High-Profile Verdicts

You might think a massive verdict in another state has nothing to do with your slip and fall claim. Think again. Insurance companies watch these outcomes very, very closely. Every huge verdict against a property owner is a stark reminder of the massive financial risk they face if they let a case go to trial.

This completely changes the dynamic during settlement negotiations. It’s no longer just about your specific injuries; it's about the insurer's potential exposure in front of a jury that could decide to make an example out of them.

The threat of a "nuclear verdict" changes the math for insurance companies. Suddenly, a reasonable settlement offer looks a lot more attractive when the alternative is a multi-million-dollar gamble at trial.

This trend is fueled by a shift in public sentiment. Juries are showing less and less patience for companies that appear to put profits before people's safety. This often leads them to award huge damages to punish the negligent party and send a clear message to other businesses.

How This Trend Strengthens Your Position

Knowing about this trend gives you and your attorney significant leverage. When we present a strong, well-documented claim to the insurance adjuster, they aren't just calculating your medical bills. They're also weighing the risk of what a jury might do if they refuse to be fair.

This isn't just a theory; it's happening right now. A recent premises liability case ended with a $43 million penalty against a pharmacy where a violent crime took place in its parking lot. Cases like this are part of a growing pattern of juror distrust toward large corporations. You can find more analysis on how these major verdicts are reshaping corporate liability on Facilities Dive.

Of course, this doesn't guarantee a lottery-sized settlement for every claim. What it does mean is that a strong, professionally prepared case carries more weight than ever before. The fear of a runaway jury is a powerful motivator for an insurer to stop lowballing and start negotiating in good faith. This shifting legal climate can be an important factor in the final premises liability settlement amounts we secure for our clients.

Practical Steps to Protect Your Claim's Value

After you’re hurt on someone else's property, the next few moments are exceptionally important. The steps you take—or fail to take—can directly influence the final premises liability settlement amounts you might recover. Securing fair compensation starts right there, at the scene of the accident.

Think of yourself as the lead investigator at a crime scene. Your job is to preserve the facts and lock down evidence before it vanishes. Following a clear checklist can build a powerful foundation for your claim and make a significant difference in your settlement.

Your Immediate Post-Accident Checklist

Taking a few deliberate actions right away will safeguard the value of your potential claim. Every step you take creates another piece of evidence that tells the true story of what happened.

- Seek Medical Attention Immediately: Your health is the absolute priority. See a doctor right away, even for what seems like a minor injury. This creates an official medical record, which is the single most important piece of evidence connecting your injuries to the incident.

- Report the Incident to the Property Owner: Find a manager, owner, or employee and tell them exactly what happened. You have a right to request a copy of the incident report they file. This officially documents that the event took place on their property.

- Document Everything on Your Phone: Use your phone to take photos and videos of the hazard that caused you to fall or get hurt. Get shots from multiple angles, showing any lack of warning signs. Also, take clear pictures of your visible injuries, like cuts or bruises.

- Get Witness Information: If anyone saw the accident, their testimony can be incredibly powerful. Politely ask for their name and phone number. An independent witness adds enormous credibility to your account of events.

- Preserve the Physical Evidence: The shoes and clothing you were wearing are now important evidence. Put them in a bag and store them somewhere safe. Don’t wash them—they might hold clues about the surface where you slipped.

An Important Piece of Advice

You will almost certainly be contacted by the property owner’s insurance company. They might sound friendly and concerned, but you need to remember their actual goal.

An insurance adjuster’s job is to protect their company's bottom line by paying out as little as possible. They are not on your side.

One of the most important things to remember is to never give a recorded statement to an insurance adjuster without speaking to an attorney first. Adjusters are skilled at asking questions designed to get you to downplay your injuries or accidentally admit partial fault. This can seriously damage your case. The Federal Trade Commission (FTC) also offers consumer guidance on handling personal injury claims, reinforcing the need for caution.

Protecting your rights by being careful with what you say is a key step toward securing fair premises liability settlement amounts.

Common Questions About Premises Liability Settlements

As an Atlanta personal injury attorney, I spend a lot of time answering questions about premises liability settlement amounts. The legal process can seem dense and confusing, so I want to tackle some of the most common concerns I hear from injured people and their families with clear, straightforward answers.

What Happens If I Was Partially at Fault for My Accident?

This is a fantastic question, and it gets to the heart of many injury cases in Georgia. Our state follows a legal rule known as “modified comparative negligence.” In plain English, this means you can still recover money for your injuries even if you were partly to blame, as long as a court finds you were less than 50% at fault.

Your final settlement, however, is reduced by your exact percentage of fault. For example, if your claim is valued at $100,000 but a jury decides you were 20% responsible for the accident, your award would be cut to $80,000. It’s an important distinction, because if you are found 50% or more at fault, you get nothing. You can see the specific language in the Official Code of Georgia Annotated, O.C.G.A. § 51-12-33.

Do I Have to Pay Taxes on My Settlement Money?

For the most part, no. The portion of your settlement that compensates you for physical injuries, physical sickness, and the medical bills that come with them is generally not considered taxable income by the IRS.

Think of it this way: the money is meant to make you whole again after an injury, not to act as income. Because of that, the IRS typically doesn't tax those funds.

There are a few exceptions. Any part of the settlement specifically designated for lost wages or punitive damages is usually taxable. Since every case has unique details, it's always a good idea to run the specifics by a tax professional. The IRS also offers helpful guidance in its Publication 4345, Settlements—Taxability.

Why Should I Not Accept the First Offer from the Insurance Company?

Insurance companies are businesses, and their number one goal is protecting their bottom line. That means paying out as little as they possibly can on claims. Their first settlement offer is almost always a lowball amount that completely fails to cover the full, true value of what you've lost.

This initial number rarely accounts for future medical treatments, long-term lost earning capacity, or the real toll of your pain and suffering. Once you accept an offer, the case is closed forever. You lose all rights to seek more money for that injury, even if your condition gets much worse down the road. That's why having an experienced attorney review any offer is non-negotiable—it’s the only way to know if the proposed premises liability settlement amounts are actually fair.