When you're in a car wreck in Atlanta, the worst-case scenario is discovering the at-fault driver has no insurance—or not enough to cover your injuries. In that moment, a choice you made on your own policy suddenly becomes the most important factor in your financial recovery: uninsured motorist stacked vs unstacked coverage.

In simple terms, stacked coverage lets you combine the insurance limits from multiple vehicles on your policy, creating a much larger safety net. Unstacked coverage, on the other hand, restricts you to the coverage limit of only the single vehicle involved in the crash. Understanding the difference between uninsured motorist stacked vs unstacked is a key step in protecting your family.

What Georgia Drivers Must Know About Stacked vs Unstacked UM

When an uninsured or underinsured driver hits you, your own insurance policy is supposed to step in and cover your losses. The decision to stack or not stack this coverage directly dictates how much financial help you can actually access from your own insurer.

Understanding this distinction is the first step toward making sure your family has the protection it truly needs. It's not a minor detail—the Insurance Research Council reports that about 1 in 8 drivers on the road is uninsured, making this a very real risk every time you drive.

Key Differences at a Glance

Let's quickly compare the core features of each option. This table provides a side-by-side look at how stacked and unstacked uninsured motorist (UM) coverage work in Georgia.

| Feature | Stacked UM Coverage | Unstacked UM Coverage |

|---|---|---|

| Coverage Limits | Combines the UM limits of all vehicles on your policy. | Limited to the UM coverage of the single vehicle in the crash. |

| Protection Level | Significantly higher. Creates a larger pool of funds for recovery. | Lower. Capped at the individual vehicle's policy limit. |

| Premium Cost | Slightly higher monthly premium. | More affordable, lower monthly premium. |

| Best For | Households with multiple vehicles seeking maximum financial security. | Budget-conscious drivers with a single vehicle or lower risk tolerance. |

The fundamental difference is multiplication versus limitation. Stacking multiplies your available coverage by the number of vehicles you insure, while unstacking limits it to a single policy amount, regardless of how many cars you own.

This choice has tangible, real-world consequences. For any household with more than one vehicle, stacking can be the difference between having your medical bills fully paid and facing substantial out-of-pocket costs after a serious accident.

If you need more information on insurance laws and your rights, you can find helpful legal guides in our online resources. Ultimately, a clear grasp of uninsured motorist stacked vs unstacked coverage helps you make a far more informed decision for your family's safety.

Understanding Uninsured and Underinsured Motorist Coverage

Before we can even talk about the pros and cons of uninsured motorist stacked vs unstacked policies, we have to get clear on what this coverage actually does. Think of Uninsured/Underinsured Motorist (UM/UIM) coverage as your personal financial backstop—an important part of your auto policy that protects you when the driver who hit you has little or no insurance.

This coverage is specifically designed to cover your damages when the at-fault driver simply can’t. Without it, you could be facing a mountain of medical bills and lost wages, all because of an accident you didn't cause.

The Two Pillars of UM/UIM Protection

This essential protection is broken down into two distinct parts, each designed to handle a different, but equally serious, situation you might encounter on Georgia roads.

Uninsured Motorist Bodily Injury (UMBI): This is your primary shield if you're hit by a driver with no insurance at all—a scenario that’s far too common. UMBI covers your medical bills, lost income from being unable to work, and compensation for your pain and suffering.

Underinsured Motorist (UIM): This kicks in when the at-fault driver has insurance, but their policy limits are too low to cover the full cost of your injuries. For instance, if your medical bills hit $75,000 but the other driver only has the state minimum of $25,000, your UIM coverage can bridge that $50,000 gap.

In essence, UM/UIM coverage becomes a substitute for the insurance the at-fault driver should have had. It ensures your ability to recover isn’t dictated by someone else's irresponsibility.

Why This Coverage Is So Important in Georgia

Georgia law, as outlined in O.C.G.A. § 33-7-11, only requires drivers to carry a minimum of $25,000 in bodily injury liability coverage per person. A serious car crash can easily generate medical expenses far beyond that amount, making UIM coverage especially valuable. You can explore our guide to get more insights into the full scope of personal injury claims and the types of damages you can recover.

This foundation explains why your choice between stacked and unstacked is so significant. It's not just a minor policy detail; it directly impacts the financial security of you and your family after a collision. That's why carefully weighing the benefits of uninsured motorist stacked vs unstacked options is one of the most important insurance decisions a driver can make.

A Detailed Analysis of Stacked and Unstacked Policies

To really understand the difference between uninsured motorist stacked vs unstacked coverage, you have to look past the definitions on the policy page and see how they actually function after a crash. The core distinction is simple: one multiplies your protection, while the other puts a hard limit on it.

This isn't just some minor detail in your insurance contract. It's a choice that can fundamentally change your financial stability after a serious accident. Let's break down the mechanics of each option with real-world numbers so you can see exactly what your premium is buying.

The Math Behind Unstacked Coverage

With an unstacked policy, sometimes called non-stacked, your uninsured motorist (UM) coverage is fixed. It applies only to the vehicle you were in during the accident, regardless of how many other cars you insure.

Think of it as having separate, isolated safety nets for each vehicle you own.

- Scenario: You insure three cars in your Atlanta household.

- Policy: Each car has $50,000 in unstacked UM coverage.

- The Accident: While driving Car A, you're hit by a driver with no insurance. Your medical bills climb to $90,000.

- The Result: Your insurance company will pay up to the $50,000 limit for Car A. The coverage on your other two cars is irrelevant, leaving you with a $40,000 hole to fill for your medical care.

This structure keeps your premiums lower, but it also creates a firm ceiling on what you can recover.

The Power of Stacking Your Coverage

Stacked coverage operates completely differently. It lets you combine—or "stack"—the UM coverage from every vehicle on your policy into one large pool of funds available after a collision.

It takes those separate safety nets and weaves them into one much larger, more robust one.

- Scenario: You own the same three cars.

- Policy: Each car has $50,000 in stacked UM coverage.

- The Accident: The same wreck occurs, resulting in $90,000 in medical bills.

- The Result: You can now combine the limits from all three cars (3 x $50,000) for a total coverage pool of $150,000. This amount is more than enough to handle your $90,000 in bills.

This multiplication effect is the key advantage of stacking. It provides a significantly higher level of financial security, which is important in cases involving severe injuries.

Comparing Payout Potential: A Side-by-Side Look

To make the financial difference crystal clear, let’s put the two approaches next to each other in a common scenario. This comparison shows the real-dollar impact of your choice.

| Coverage Element | Unstacked UM Policy Example | Stacked UM Policy Example |

|---|---|---|

| Vehicles Insured | 2 Cars | 2 Cars |

| UM Limit Per Vehicle | $100,000 | $100,000 |

| Total Medical Bills | $160,000 | $160,000 |

| Maximum Available Coverage | $100,000 | $200,000 (2 x $100,000) |

| Your Out-of-Pocket Cost | $60,000 | $0 |

As the table demonstrates, the stacked policy covers the extensive medical costs entirely. The unstacked policy leaves the injured person holding a bill for a substantial amount of debt.

It's important to remember a key detail in Georgia: stacking typically applies to bodily injury claims, not property damage. This means it's designed to cover your medical bills, lost wages, and pain and suffering—not the repairs to your vehicle.

This is a nationwide issue, not just a local one. In some states, a rising number of uninsured drivers has made stacked coverage an even more important choice. For example, if a family insures three vehicles with $25,000 of UM protection on each, stacking gives them access to a $75,000 safety net if a family member is hurt by an uninsured driver. The combined coverage far surpasses what an unstacked policy could provide. You can find more information on state-by-state rules in this detailed breakdown of UM coverage.

By analyzing the practical math, it becomes obvious that the choice between uninsured motorist stacked vs unstacked is a big financial decision for any household with more than one car.

How Stacking Works: Vertical vs. Horizontal Methods

The concept of "stacking" your insurance might seem tricky, but it's really just a method for combining Uninsured Motorist (UM) coverage to give yourself a bigger financial cushion. It’s a key detail in the uninsured motorist stacked vs unstacked conversation.

In Georgia, there are two ways this works: vertical and horizontal stacking. Knowing which one applies to your policy is valuable, as it directly dictates how much your coverage limits can be multiplied after a crash.

Vertical Stacking: The Georgia Standard

Vertical stacking is, by far, the most common approach you’ll see in Georgia. This method lets you combine the UM coverage limits for multiple vehicles insured under a single policy.

Think of a family with two cars insured together on one policy. If you chose stacked UM coverage when you bought that policy, vertical stacking is how it activates.

- Policy Structure: One insurance policy covering two or more vehicles.

- Coverage Limit: Let’s say you have $25,000 in UM coverage for each car.

- How It Stacks: After an accident with an uninsured driver, you can combine those limits. Your total available UM coverage is now $50,000 ($25,000 from Car 1 + $25,000 from Car 2).

This is a powerful tool for any household insuring multiple cars together. Each vehicle on your policy essentially adds another layer of financial protection for you and your family.

The core principle of vertical stacking is straightforward: more vehicles on a single policy equal a higher potential UM payout. It’s a direct multiplication of your coverage based on the number of vehicles you insure together.

Horizontal Stacking: A Far Less Common Method

The second approach is horizontal stacking. This involves combining UM coverage limits from separate insurance policies within the same household. This scenario is much less common because its availability depends entirely on state law and the exact language in your insurance contracts.

For example, a husband and wife might each have their own separate auto policies.

- Policy Structure: You have a policy for your car, and your spouse has a completely separate one for theirs.

- Coverage Limit: Both policies carry $50,000 in UM coverage.

- How It Stacks: In the few states where horizontal stacking is allowed, an injured person covered by both policies could potentially access a combined limit of $100,000.

However, this is not standard practice in Georgia. Most insurance policies are specifically written to prohibit this kind of stacking across different policies. You should always assume vertical stacking is the default method unless your agent and policy documents explicitly say otherwise.

Comparing the Two Methods

The distinction between these methods is important. Stacked UM coverage works through two very different mechanisms—vertical and horizontal. To learn more about how stacking functions in different scenarios, this guide on stacked car insurance from Bankrate offers a helpful overview.

For Georgia drivers, here’s the bottom line:

| Stacking Method | How It Works | Commonality in Georgia |

|---|---|---|

| Vertical Stacking | Combines UM limits from multiple cars on a single policy. | Very Common. This is the standard method in Georgia. |

| Horizontal Stacking | Combines UM limits from separate policies in the same household. | Very Rare. Usually restricted or prohibited by policy language. |

Understanding these two approaches gives you a clearer picture of how a stacked policy multiplies your protection. This knowledge helps you ask the right questions when reviewing your policy, ensuring you have the coverage you think you do. The difference between uninsured motorist stacked vs unstacked ultimately comes down to maximizing the resources available to you and your family after a collision.

Real-World Scenarios Showing When Stacking Matters

Theory is one thing, but seeing how the choice between uninsured motorist stacked vs unstacked coverage plays out in real life is what truly matters. This one decision on your insurance policy has tangible, and often massive, financial consequences after a crash. Let’s walk through a few scenarios an Atlanta driver could easily face to see the powerful impact of stacking.

The Hit-and-Run on I-75

Picture a family of four driving home on I-75 after a Braves game. Out of nowhere, a speeding car swerves into their lane, causes a serious collision, and then races off. The hit-and-run driver is never found, which legally makes them an uninsured motorist. The mother, a passenger, suffers severe back injuries that will require surgery and months of physical therapy.

The family’s medical bills quickly climb to $140,000. They have two cars insured on their policy, each carrying $100,000 in Uninsured Motorist (UM) Bodily Injury coverage.

Scenario A: The Unstacked Policy: With an unstacked policy, their financial recovery is capped at the $100,000 limit for the single car they were in. This leaves them holding $40,000 in medical debt, forcing them to drain their retirement savings and set up a painful hospital payment plan.

Scenario B: The Stacked Policy: Because they chose to stack, they can combine the UM limits from both cars on their policy. Their total available coverage is now $200,000 ($100,000 x 2 cars). This is more than enough to cover the $140,000 in medical bills, plus lost wages and other related expenses. The family avoids financial disaster, all because of one small choice they made when buying their policy.

When Coverage Protects You Outside Your Car

Here’s an overlooked but valuable benefit: stacked UM coverage doesn’t just protect you behind the wheel. It often follows you and your resident family members even when you're pedestrians or cyclists.

Let's consider another situation. A college student is jogging near Piedmont Park when a distracted, uninsured driver blows a red light and hits her in the crosswalk. She sustains a broken leg and a concussion, leading to ER visits, specialist appointments, and weeks of missed work. Her total damages add up to $65,000.

Her parents have three vehicles on their auto policy, each with $25,000 in UM coverage.

With Unstacked Coverage: Since no specific car from the policy was involved, the insurer would likely cap the payout at the $25,000 limit associated with just one vehicle. This leaves her with $40,000 in uncovered medical bills and lost wages—a crushing financial burden for a young student.

With Stacked Coverage: Stacking lets her access the combined total from all three vehicles. She has a $75,000 pool of coverage ($25,000 x 3 cars) available for her injuries. This is enough to cover all her medical costs and lost income, allowing her to focus on healing instead of debt.

These scenarios highlight a fundamental truth: Your need for coverage doesn't disappear just because you aren't in your car. A serious injury can happen anywhere, and stacked UM coverage provides a much broader safety net for your entire household.

The Georgia Governor's Office of Highway Safety consistently reports thousands of pedestrian-involved crashes each year, underscoring that this risk is very real.

The Contrast in Financial Outcomes

The core difference in these examples isn't the accident—it's the financial aftermath. The family with unstacked coverage is pushed into a crisis, while the family with stacked coverage is made whole. Working through the claims process after an accident is already difficult; having enough coverage is the first step. For more on that process, you can find helpful information in our guide on how to file a car accident claim in Atlanta.

These stories show that the small extra premium for stacked insurance isn't just a cost; it's an investment in your family's financial security. When you’re facing catastrophic injuries caused by an irresponsible driver, the choice between uninsured motorist stacked vs unstacked can be the single most important factor in your ability to recover without going into debt.

How to Choose the Right Coverage for Your Family

Deciding between uninsured motorist stacked vs unstacked coverage is one of the most important insurance decisions you can make. It’s not just a box to check—it’s a choice that directly impacts your family's financial security after a serious accident.

There’s no one-size-fits-all answer here. The right move depends entirely on your household’s specific circumstances. It comes down to weighing the small increase in cost against the massive increase in protection. Your goal should be to secure genuine peace of mind without overextending your budget.

Key Factors to Consider

To get clear on the right path for you, start by asking a few practical questions. Your answers will point you toward the coverage that makes the most sense.

- How many vehicles are on your policy? If you insure two or more cars, stacking provides the most direct value. The financial benefit multiplies with each vehicle you add.

- What does your health insurance coverage look like? Think about your deductible and out-of-pocket maximums. A severe collision can easily generate medical bills far exceeding what your health plan will cover. Stacked UM coverage is designed to fill that important gap.

- What is your overall financial situation? Be honest about your savings and ability to absorb a catastrophic expense. Could your family handle $50,000 or more in unexpected medical debt? For most people, the answer is a hard no.

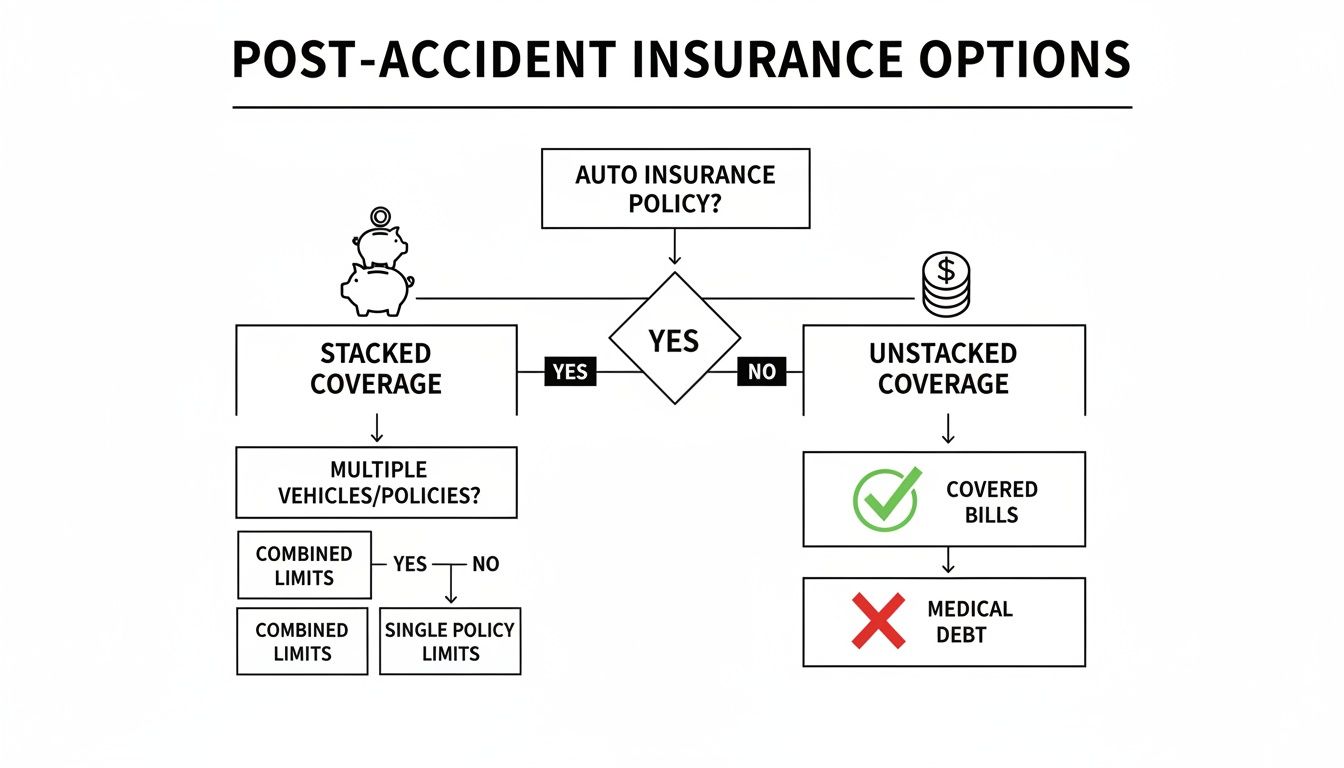

This decision tree shows the two very different outcomes you could face after an accident, depending entirely on which coverage you chose beforehand.

As the graphic illustrates, stacked coverage is the path to covered bills and financial stability. Unstacked coverage, on the other hand, can quickly lead to overwhelming medical debt.

For a small increase in your premium—often just a few dollars a month per vehicle—you can double, triple, or even quadruple your family's financial protection.

This isn't just about paying medical bills. It’s about safeguarding your savings, your home, and your family's future. The Georgia Office of Insurance and Safety Fire Commissioner offers helpful consumer resources to clarify your rights and policy options.

By taking a hard look at your personal situation, you can confidently decide if upgrading your uninsured motorist stacked vs unstacked coverage is the right move for you.

Frequently Asked Questions About Georgia UM Coverage

When it comes to uninsured motorist stacked vs unstacked coverage, I find the same questions come up again and again. Here are some straightforward answers to the questions we hear most often from our clients here in Atlanta.

Can I Stack My UM Coverage in Georgia?

Yes, absolutely. Georgia law permits you to stack your Uninsured/Underinsured Motorist coverage. If you insure multiple vehicles on a single policy, you can typically pay a slightly higher premium to combine—or "stack"—the coverage limits for each car into one larger pool of funds.

You must, however, actively choose this option. It's rarely the default setting on a policy. The only way to know for sure is to pull out your policy's declarations page or call your insurance agent directly to confirm you have this important protection.

Is Stacked Insurance Really Worth the Extra Cost?

For most Georgia families with more than one vehicle, the answer is an emphatic yes. The premium increase for stacking is usually quite small when you compare it to the massive leap in financial protection it provides for you and your family.

Think of it this way: a serious car wreck can easily run up medical bills over $100,000. If you have two cars on your policy, each with $50,000 in unstacked UM, your recovery is capped at $50,000. By simply stacking, you would have access to the full $100,000. That single decision can be the difference between financial security and devastating debt.

How Do I Know if My Coverage is Stacked or Unstacked?

Your auto insurance policy's declarations page is the most reliable source. This document summarizes all your coverages and their limits. Find the Uninsured/Underinsured Motorist (UM/UIM) section, and it should clearly state whether your coverage is 'Stacked' or 'Unstacked' (sometimes called 'Non-Stacked').

If you can't find it or the language is confusing, don't guess. Call your agent and ask them to provide written confirmation.

What Should I Do After an Accident with an Uninsured Driver?

First things first: ensure everyone is safe and call 911 to get an officer on the scene. An official police report is a non-negotiable document for any UM claim.

Next, notify your own insurance company as soon as you can—it's your policy that will have to protect you. I strongly advise speaking with an attorney before you give a recorded statement to any insurance adjuster. An experienced lawyer can also help you with all the strict deadlines that apply, which you can learn more about by reading our article on the statute of limitations for personal injury in GA.

Knowing the details of your uninsured motorist stacked vs unstacked coverage is fundamental to protecting your rights after a crash.