Georgia auto insurance requirements are essential for every driver in Atlanta and across the state. As an Atlanta personal injury attorney, I see the life-altering impact of car accidents every day. Understanding these requirements isn't just about following the law—it's about building a financial shield for yourself and your family.

Your Guide to Driving Legally and Safely in Georgia

Here in Georgia, the law operates on a "fault" system. That means if you cause a car accident, you and your insurance company are financially on the hook for the injuries and property damage that result. Proper insurance coverage is often the one thing that stands between a family and serious financial hardship after a collision.

Most drivers know the state sets minimum insurance limits, but few realize how quickly those minimums can evaporate in a real-world accident. Simply meeting the legal baseline might not be enough to protect your personal assets if a serious crash occurs.

Before we dive into the details, you might find the Wikipedia entry on car insurance helpful for general background.

What Is Mandatory Liability Coverage?

The foundation of Georgia's insurance law is liability coverage. Think of this as protection for other people when you are at fault. It is designed to pay for their medical bills and repair costs, not your own. The state mandates that every registered vehicle must carry at least the minimum amount of this coverage.

Georgia Minimum Liability Insurance at a Glance

This table shows the mandatory minimum liability coverage every Georgia driver must have, known as the "25/50/25" rule.

| Coverage Type | Minimum Per Person | Minimum Per Accident |

|---|---|---|

| Bodily Injury Liability | $25,000 | $50,000 |

| Property Damage Liability | N/A | $25,000 |

These numbers represent the bare minimum required to legally operate a vehicle. We will explain what they actually mean in an accident and explore why exceeding them is a wise decision.

Beyond the Minimums

Insurance isn't just a legal checkbox. It's a tool that protects you, your family, and your financial future from the unexpected chaos an accident can cause. For a broader overview of general driving laws and requirements in Georgia, this resource is quite helpful.

Breaking Down Georgia's 25/50/25 Liability Rule

At the heart of Georgia’s insurance law is a mandatory liability coverage rule known as "25/50/25." These numbers might just look like jargon, but they are the key to understanding your financial protection if you cause an accident. Let’s pull back the curtain on what each number really means.

Think of these as three separate pots of money your insurance company sets aside to pay for damages you cause to other people. This is the bare minimum you need to legally drive in Georgia.

The First 25: Bodily Injury Liability Per Person

The first number is $25,000. This is the maximum amount your insurer will pay for a single person's medical bills if you injure them in a crash you caused. This coverage helps pay for things like an ambulance ride, hospital treatment, and follow-up care for one individual.

So, if you’re at fault and the other driver's medical expenses hit $35,000, your policy pays up to its $25,000 limit. You are then on the hook for the remaining $10,000 out of your own pocket.

The 50: Bodily Injury Liability Per Accident

The second number, $50,000, represents the total payout for injuries if you hurt more than one person in a single accident. It's the absolute ceiling for all combined medical claims, no matter how many people need care.

Imagine you cause a collision that injures three people, each with $20,000 in medical bills. The total cost is $60,000, but your insurance will only pay its maximum of $50,000. That leaves you personally responsible for the $10,000 difference.

It's easy to see how quickly these minimums can be exhausted. One serious injury or a multi-vehicle pileup can lead to costs that blow past the state-required limits, putting your personal assets—like your home or savings—at risk.

The Second 25: Property Damage Liability

The final $25,000 is for property damage. It’s the maximum your policy will pay to repair or replace someone else's property you damage, which is almost always their vehicle. But it could also cover a smashed fence, a mailbox, or even the side of a building.

With the soaring prices of modern vehicles packed with expensive sensors and tech, $25,000 often isn't enough to cover a total loss. If you total someone's brand-new SUV, you could easily owe thousands more than your insurance will pay.

Georgia law requires every driver to carry this liability insurance. And the financial stakes are getting higher. The average cost for full coverage in Georgia jumped from $1,617 in 2022 to $1,973 in 2023—a 22% increase in one year. This spike is driven by more frequent accidents and bigger claim payouts.

It’s helpful to understand how Georgia’s minimums compare to federal rules, like the higher FMCSA insurance requirements for commercial trucks. For personal drivers, these minimums are just the starting point, not the finish line, for solid financial protection.

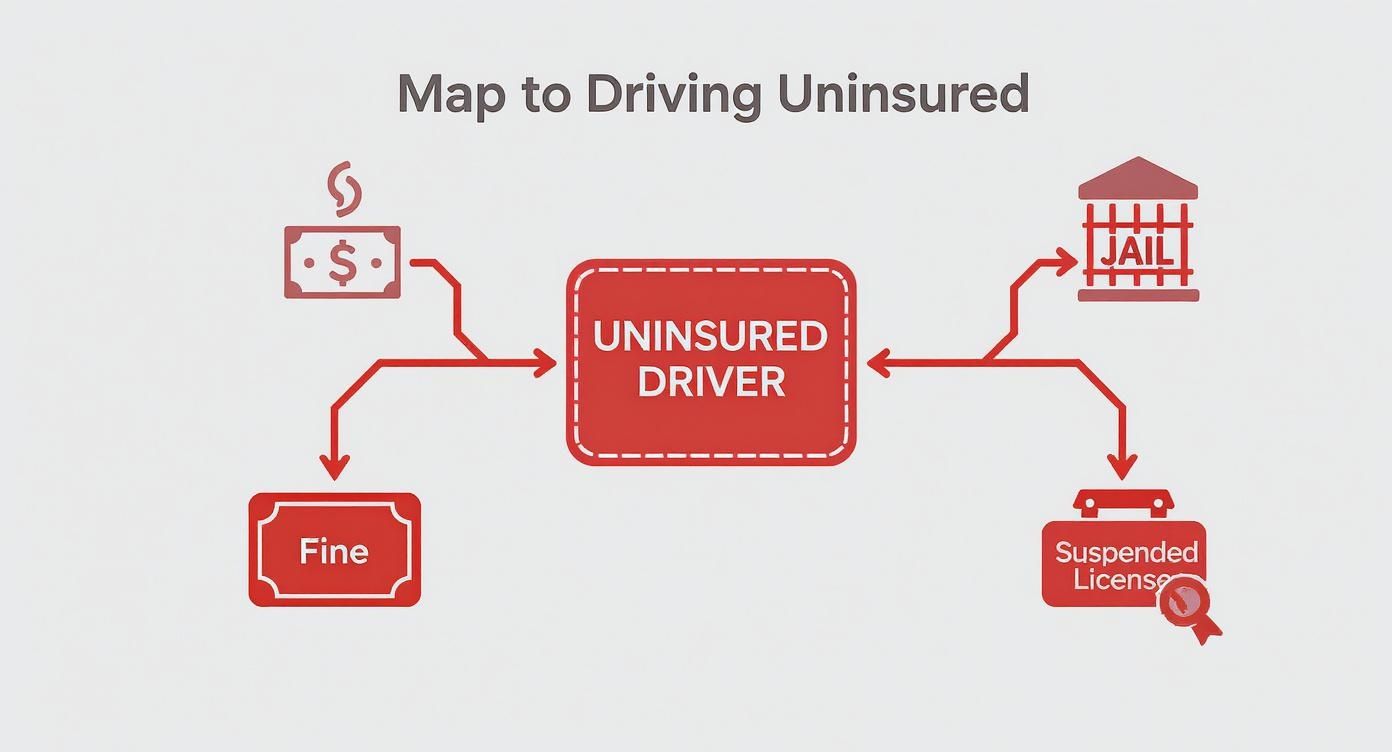

The Steep Price of Driving Uninsured in Georgia

Getting behind the wheel in Georgia without the state-mandated auto insurance isn't just a minor mistake—it’s a serious gamble with steep consequences. The state has put firm penalties in place, not just to issue a ticket, but to strongly discourage anyone from driving unprotected.

If you're caught driving without insurance, you are committing a misdemeanor. The penalties can disrupt your finances, your freedom, and your ability to drive legally.

Immediate Legal Consequences

- Substantial Fines: Between $200 and $1,000.

- Potential Jail Time: Up to 12 months.

- Suspension of License & Registration: 60 to 90 days.

After the suspension, you’ll pay additional lapse and reinstatement fees, and your insurer will need to file an SR-22A certificate with the state—a probationary watchlist that lasts about three years.

The Overwhelming Financial Risk of an Accident

Forget the legal penalties for a moment. The real financial danger comes if you cause an accident while uninsured. Georgia is a fault state, meaning you are personally responsible for every dollar of damage.

Think about causing a pile-up on I-285. The costs for vehicle repairs, ambulance rides, hospital stays, and lost wages can skyrocket into the tens or even hundreds of thousands of dollars. Without an insurance company to pay those bills, that entire financial weight lands squarely on you.

Handling that mess alone can be overwhelming. Knowing how to file a car accident claim in Atlanta is key for anyone in a collision, but for an uninsured driver, the process is loaded with personal liability. For official penalty details, visit the Georgia Department of Driver Services.

The state’s message is clear: driving without insurance is a high-stakes bet where you risk your money, your freedom, and your financial future. It’s simply not worth it.

Why State Minimum Coverage Is Often Not Enough

Meeting the state's Georgia auto insurance requirements is just the first step. Think of the 25/50/25 rule as the absolute floor for legal driving, not the ceiling for your financial protection. While it keeps you compliant with the law, state minimum coverage can leave you dangerously exposed in a serious accident.

Imagine you cause a collision that totals a new SUV worth $40,000. The other driver racks up $60,000 in medical bills. Your minimum policy covers just $25,000 for the vehicle and $25,000 for injuries, leaving you on the hook for $50,000. That debt can put your home, savings, and future income in jeopardy.

Building Your Financial Shield with Optional Coverages

If your basic liability insurance is the foundation, these add-ons are the walls and roof that actually shield you from a financial storm:

- Uninsured/Underinsured Motorist (UM/UIM) Coverage: This add-on is arguably the most important protection in Georgia. It covers you if the at-fault driver lacks sufficient insurance.

- Medical Payments (MedPay) Coverage: Pays medical expenses for you and your passengers, regardless of fault. Great for deductibles, co-pays, and ambulance rides.

- Collision Coverage: Fixes or replaces your car after an accident you cause.

- Comprehensive Coverage: Covers non-collision damage like theft, vandalism, fire, or falling tree limbs.

Failing to carry even the minimum insurance leads to severe penalties, and that’s before the financial ruin of causing an accident.

The Real Cost of Protection

Yes, opting for better coverage increases your premium, but that cost is tiny compared to what you could owe after a serious accident. In Georgia, liability-only coverage runs around $77 per month, while comprehensive options average $135.

Your credit score also plays a role: drivers with poor credit might pay $262 for full coverage, versus $133 for those with good credit. With Georgia ranking 10th for the highest premiums—an average of $2,688 annually—making informed coverage choices matters.

Your auto insurance policy isn't just another monthly bill; it's a key investment in your financial security.

If you ever need to understand your legal options after a collision, learn more about how personal injury claims work.

Key Factors That Affect Your Insurance Premiums

Ever wondered how insurers calculate your premium? It’s a personalized assessment of risk based on factors like:

Your Driving Record and Experience

- Clean Record: No accidents or violations signals low risk.

- Age & Experience: Younger, less-experienced drivers face higher rates.

Where You Live and Park Your Car

- Urban vs. Rural: Cities like Atlanta often have higher rates than smaller towns.

- Parking Location: A secure garage can lower comprehensive rates compared to street parking.

The Vehicle You Drive

- Make & Model: Sports cars and luxury vehicles cost more to insure.

- Safety Ratings: Discount opportunities for top-rated vehicles from Insurance Institute for Highway Safety (IIHS).

- Theft Rates: Popular target models can drive premiums up.

Personal Factors and Coverage Choices

- Credit-Based Insurance Score: A significant rating factor in Georgia.

- Coverage Limits & Deductibles: Higher limits and lower deductibles raise premiums but boost protection.

The average annual auto insurance premium in Atlanta is $3,112, compared to $2,360 in Augusta and $2,515 in Columbus. See how how these insurance costs vary across Georgia.

Understanding what drives your premium helps you find discounts and balance cost with protection.

Common Questions About Georgia Auto Insurance

How Do I Prove I Have Insurance in Georgia?

Show a physical insurance card or a digital copy on your phone. Georgia’s Electronic Insurance Verification System (GEICS) also lets officers confirm your status in real time.

Does a Car Need Insurance If It Is Not Driven Often?

Yes. Any vehicle with active Georgia registration must have continuous insurance. To drop coverage, you must first cancel the registration.

What Is an SR-22A Certificate?

An SR-22A is a certificate your insurer files with the state to prove you’re carrying required liability coverage. It’s typically required after serious offenses like a DUI or driving uninsured.

Will My Rates Increase After a Not-at-Fault Accident?

Rates should not go up if you’re clearly not at fault, such as being rear-ended. However, confirm with your insurer, since policies vary. Also, know the statute of limitations for personal injury in GA to protect your right to seek compensation.

Make sure you stay informed about and meet all your Georgia auto insurance requirements.