Being hit by an unlicensed driver in Georgia raises immediate questions about insurance coverage, liability, and who actually pays for your injuries. The answers depend on several factors — including who owned the vehicle, whether that owner had a valid insurance policy in effect, and what uninsured motorist coverage you carry on your own policy. Georgia law does not let unlicensed drivers off the hook for causing accidents, and it does not leave injured victims without meaningful options even when the at-fault driver appears to have nothing. What it requires is understanding how liability flows in these situations, because the path to compensation often runs through the vehicle owner, the owner’s insurer, and your own UM coverage — simultaneously — rather than following the straightforward path of a standard insured-driver collision. This guide explains your rights and every viable recovery option under Georgia law.

Does an Unlicensed Driver in Georgia Still Have Insurance Liability?

One of the most common misconceptions after being hit by an unlicensed driver is that their lack of a license means there is no insurance coverage available. That is usually wrong. In Georgia, insurance follows the vehicle — not the driver’s license status.

The Vehicle Owner’s Insurance Covers the Car, Not Just Licensed Drivers

If the unlicensed driver was operating a vehicle owned by someone else, the vehicle owner’s auto insurance policy is the first layer of coverage. Georgia’s auto insurance requirements attach to the vehicle registration. If the owner’s policy was active at the time of the collision, that policy covers damages caused by anyone they permitted to operate the vehicle — licensed or not. The driver’s lack of a license does not automatically void the owner’s coverage or eliminate your claim against that policy. Georgia’s financial responsibility laws are designed specifically to protect innocent third parties — not to shield insurers from paying covered claims.

The Owner May Face Independent Liability

Vehicle owners who knowingly permit an unlicensed driver to use their car face potential liability under Georgia’s negligent entrustment doctrine. If the owner knew — or should have known — that the person they gave the keys to was unlicensed, unqualified, or otherwise unfit to drive, they can be held personally liable for the resulting damages, separate from the driver’s own liability. This matters in cases where the driver has no assets and limited insurance, because the owner may be a deeper source of recovery.

Practical rule: In Georgia, the first question after a crash with an unlicensed driver is not “do they have insurance?” — it is “whose vehicle were they driving, and does that owner have coverage?” The vehicle owner’s policy is usually the primary source of recovery.

What Happens When the Unlicensed Driver Owns the Vehicle?

When the unlicensed driver owns the vehicle themselves, the coverage picture is more complicated — but not necessarily hopeless.

Can an Unlicensed Driver Get Car Insurance in Georgia?

Technically, some insurers will issue policies to unlicensed vehicle owners — particularly for vehicles that are garaged, loaned exclusively to licensed family members, or owned for purposes other than regular driving. However, most standard auto insurance policies require a licensed primary driver. If an unlicensed owner purchased a policy by misrepresenting their license status, the insurer may attempt to deny coverage on the grounds of material misrepresentation. Georgia law limits insurer rescission in some circumstances, particularly where innocent third-party claimants are involved — but this area of coverage litigation is complex and often requires legal challenge to resolve.

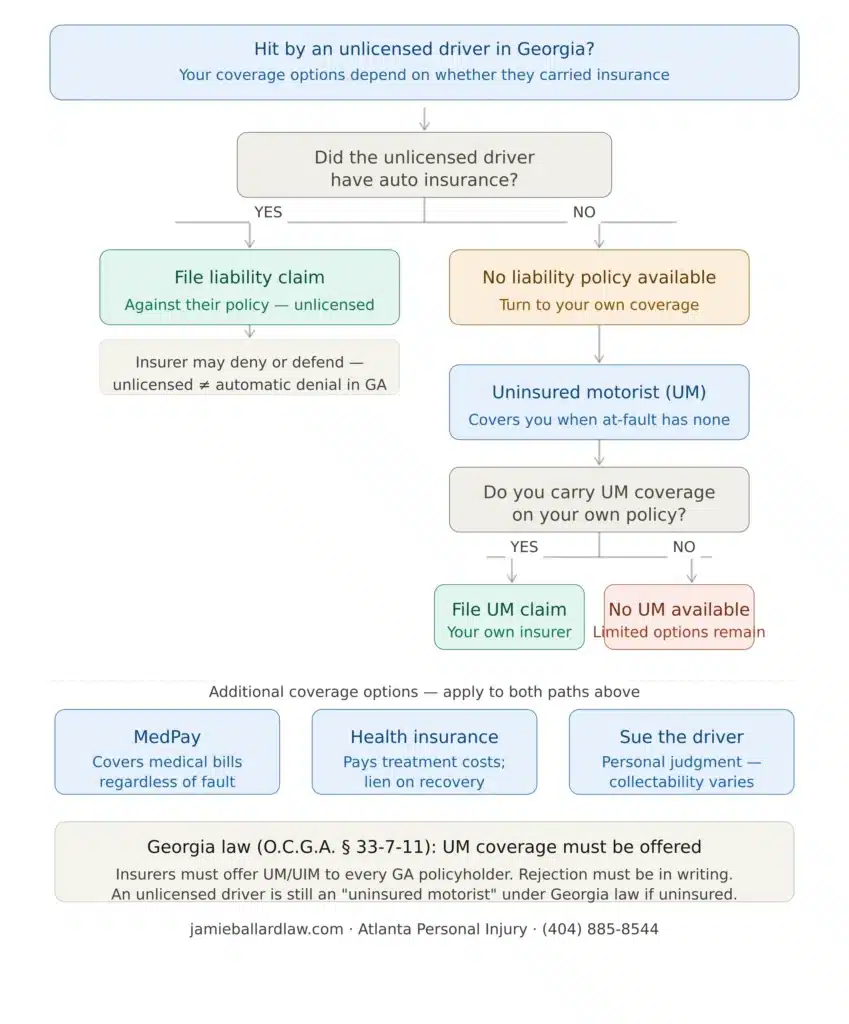

When No Insurance Exists at All

If the unlicensed driver owns the vehicle and carries no valid insurance — or if their insurer successfully denies coverage — your own uninsured motorist coverage becomes the primary recovery mechanism. Georgia car accident law requires insurers to offer uninsured motorist coverage to all policyholders. If you have it, it can compensate you for your injuries, medical bills, lost income, and pain and suffering as if the at-fault driver had carried liability coverage. The coverage limit equals your own UM policy limit — which is why carrying adequate UM coverage matters even if you are a careful driver.

Georgia’s Uninsured Motorist Statute

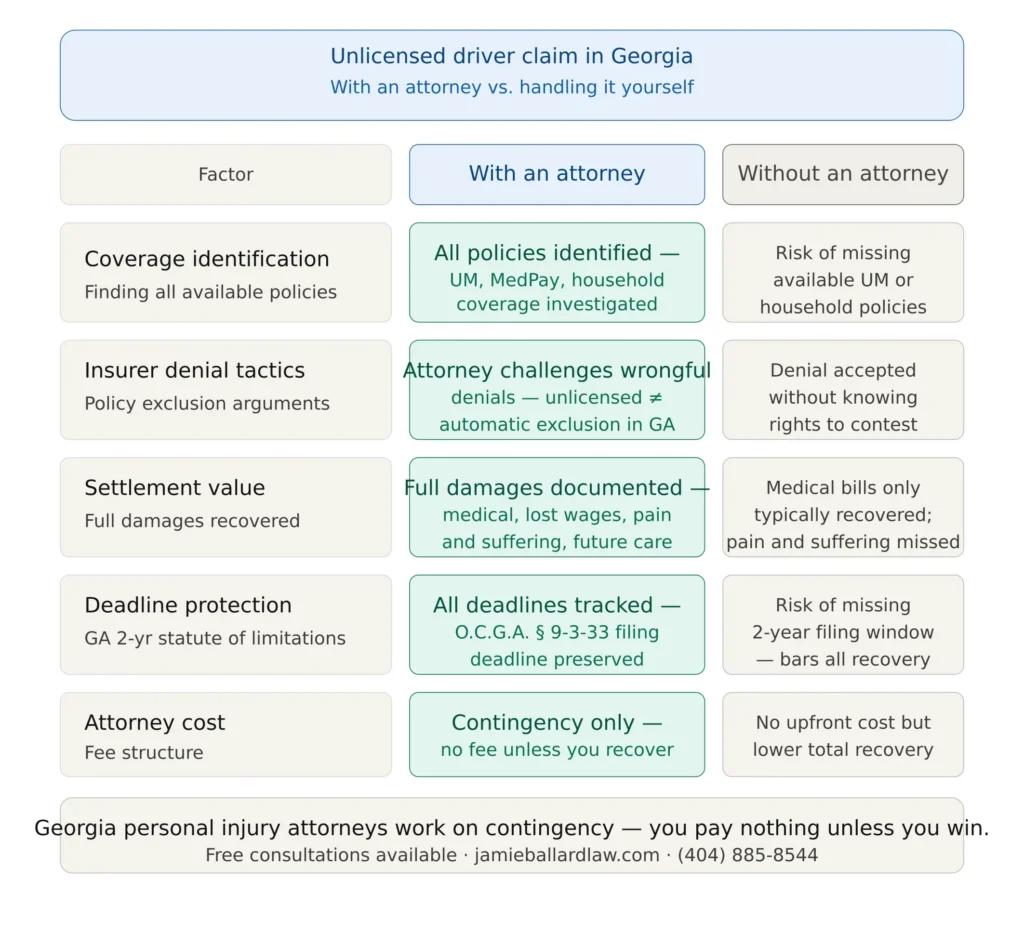

Under O.C.G.A. § 33-7-11, Georgia mandates that auto insurers offer uninsured motorist coverage to every policyholder at the time of policy issuance and renewal. You can reject it in writing — but if you did not affirmatively reject it on a signed form, you likely have it even if you do not realize the full scope of what it covers. Stacked UM coverage, available on policies covering multiple vehicles, allows you to add the UM limits from each vehicle together — potentially multiplying the total coverage available from a single insurer. An experienced Atlanta personal injury attorney reviews your complete policy declarations page alongside the at-fault driver’s coverage situation to map every available dollar of compensation from day one — including UM benefits you may not have known you carried.

Negligent Entrustment — Holding the Vehicle Owner Accountable

Georgia’s negligent entrustment doctrine is one of the most powerful tools in unlicensed driver accident cases. It allows injured victims to hold vehicle owners directly liable when they knowingly allowed an incompetent or unfit driver to use their vehicle.

What Negligent Entrustment Requires

To establish negligent entrustment under Georgia law, your attorney must show that the vehicle owner entrusted the vehicle to the unlicensed driver, that the owner knew or should have known the driver was unlicensed or otherwise incompetent, and that the driver’s operation of the vehicle caused your injuries. The knowledge element is critical. Prior incidents, conversations about the driver’s license status, family relationships where license status was common knowledge, or situations where a reasonable person would have checked — all of these can establish constructive knowledge sufficient to support a negligent entrustment claim under Georgia case law.

Why This Matters for Your Recovery

Negligent entrustment expands the defendant pool beyond the driver alone. Vehicle owners often have greater insurance coverage, more assets, and more exposure to liability than unlicensed drivers who may have little to none. When an owner’s liability insurer is facing a negligent entrustment claim in addition to standard vicarious liability, the settlement calculus changes significantly — producing higher offers and faster resolution than claims against the driver alone. The Georgia statutes and case law on Justia document how Georgia courts have applied negligent entrustment in vehicle accident contexts over decades of case history.

Practical rule: If the vehicle owner knew the driver had no license — or had any reasonable basis to check — negligent entrustment may give you a direct claim against the owner’s assets and insurance, independent of what coverage the driver carries.

What to Do Immediately After a Crash With an Unlicensed Driver in Georgia

The steps you take in the hours after the collision directly affect your ability to recover full compensation. These situations require more documentation, not less.

Get a Police Report That Documents the License Status

Call 911 and wait for law enforcement. When officers arrive, make sure the other driver’s lack of a valid license is documented in the report — do not assume the officer will check independently. Georgia law enforcement will note the driver’s license status and any citation issued for driving without a license during the accident investigation. This documentation becomes critical evidence for your car accident claim, for your negligent entrustment claim against the vehicle owner, and for your own UM carrier when processing your uninsured motorist claim. Never agree to handle a collision informally without a police report, especially when the other driver is unlicensed or uninsured — they have every incentive to avoid official documentation, and your legal position weakens significantly without it.

Identify the Vehicle Owner Separately From the Driver

Get the vehicle’s registration information from the officer’s report, not just from the driver. The registration shows the legal owner, which may be different from who was driving. Photograph the registration, the license plate, the VIN if visible, and any insurance documents the driver provides. If the driver claims to have insurance, get the policy number and insurer name and verify it independently — unlicensed drivers sometimes provide false or expired insurance information at accident scenes.

Seek Medical Care Immediately

Do not wait to see a doctor even if you feel relatively okay at the accident scene. Injuries from vehicle collisions frequently have delayed symptom onset — soft tissue damage, concussions, spinal injuries, and internal bleeding can worsen significantly in the 24 to 72 hours after impact, after adrenaline subsides and swelling sets in. Seeking immediate care creates a contemporaneous medical record that connects your specific injuries to the date and mechanism of the collision, which is essential documentation for every insurance coverage claim you will make — including your UM claim. A gap in treatment gives insurers grounds to argue your injuries were pre-existing or caused by something other than the accident. The CDC’s motor vehicle safety resources document the full range of injuries common in vehicle collisions and the critical importance of prompt medical evaluation even when initial symptoms appear minor.

Contact a Georgia Personal Injury Attorney Before Talking to Any Insurer

Unlicensed driver cases involve multiple potential insurers — the driver’s own coverage if any, the vehicle owner’s carrier, and your own UM carrier. Each of those insurers has adjusters whose job is to minimize what they pay. Before you give any recorded statement to any insurance company, speak with an attorney who can evaluate your coverage landscape, identify all available sources of compensation, and ensure you do not inadvertently say anything that limits your recovery. The Georgia Office of Commissioner of Insurance provides consumer resources on your rights when dealing with insurance carriers after an accident.

Practical rule: In unlicensed driver accidents, multiple insurers are potentially involved — and each one is looking for a reason to pay less. Get an attorney before you give any recorded statement to any of them.

Georgia Laws That Affect Unlicensed Driver Accident Claims

Several Georgia statutes directly shape how these cases develop and what remedies are available to injured victims.

Georgia’s Mandatory Liability Insurance Law

Under O.C.G.A. § 40-9-37, all motor vehicles operated on Georgia roads must be covered by minimum liability insurance — $25,000 per person and $50,000 per occurrence for bodily injury. The obligation attaches to the vehicle, not the driver’s license status. An unlicensed driver operating an insured vehicle does not void the vehicle owner’s coverage obligation to third parties under Georgia’s financial responsibility laws — though their insurer may dispute it and litigation may be required to enforce it.

Georgia’s Negligence Per Se Doctrine

Driving without a valid license in Georgia is a criminal offense under O.C.G.A. § 40-5-20. Under Georgia’s negligence per se doctrine, violating a criminal statute intended to protect public safety can establish negligence as a matter of law — meaning you do not have to separately prove the driver was acting carelessly. The unlicensed status itself, in the context of causing a collision, supports a finding of negligence without additional proof of careless driving behavior.

Georgia’s Two-Year Statute of Limitations

Personal injury claims in Georgia must be filed within two years of the accident date under O.C.G.A. § 9-3-33. This applies regardless of whether the at-fault driver was licensed. Do not let the complexity of the coverage situation delay your legal consultation — the clock starts on the day of the accident, and waiting too long risks losing your right to recovery entirely regardless of how strong your case is on the merits. Full text of this limitation is available at Justia’s Georgia statutes database.

How Georgia Courts Have Handled Unlicensed Driver Insurance Disputes

Litigation over coverage in unlicensed driver accidents follows a consistent pattern in Georgia courts. Understanding how these disputes typically unfold helps you and your attorney anticipate insurer arguments and build a response before they arise.

Insurer Exclusion Arguments and How They Fail

After an accident involving an unlicensed driver in Georgia, the vehicle owner’s insurer will sometimes attempt to invoke a policy exclusion — arguing that coverage does not apply because the driver lacked a valid license. Georgia courts have repeatedly scrutinized these exclusions when they are used to deny coverage to innocent third-party claimants. Under Georgia’s compulsory insurance framework, exclusions that effectively strip coverage from injured parties who had no knowledge of the driver’s license status face significant legal challenges. Courts distinguish between exclusions that limit coverage between the insurer and the named insured versus exclusions that attempt to bar injured third parties from recovery entirely.

Permissive Use and Implied Permission

Georgia applies a permissive use doctrine in vehicle insurance cases. If the unlicensed driver had the owner’s permission — express or implied — to use the vehicle, the owner’s liability coverage generally extends to the collision. Implied permission is established through patterns of conduct: the owner regularly let the person use the vehicle, the driver had unrestricted access to the keys, or family relationships existed that created a reasonable expectation of permission. Defense insurers frequently argue that permission was limited or that the driver exceeded the scope of any permission granted — and your attorney’s investigation of the relationship between driver and owner is essential to defeating those arguments.

When the Insurer Claims the Policy Is Void

In some cases, insurers argue the entire policy is void because the named insured misrepresented their license status when purchasing coverage. Georgia’s O.C.G.A. § 33-24-7 governs insurer rescission rights and requires that any misrepresentation be material and that the insurer act within applicable deadlines. More importantly, Georgia’s financial responsibility laws limit an insurer’s ability to avoid liability to innocent third-party accident victims even when rescission is otherwise permitted as between the insurer and the policyholder. Navigating these coverage disputes requires an attorney familiar with Georgia insurance law — not just personal injury practice.

Practical rule: When an insurer denies coverage after an unlicensed driver accident, that denial is the beginning of a legal dispute — not the end of your claim. Georgia law provides multiple avenues to challenge coverage denials that affect innocent third-party victims.

Using Georgia’s Bad Faith Statute Against Insurers

If your own UM carrier or the at-fault vehicle’s insurer refuses to settle a valid claim within a reasonable time, Georgia’s bad faith statute under O.C.G.A. § 33-4-6 may entitle you to penalty damages and attorney fees on top of your compensatory recovery. An attorney who makes a proper pre-suit demand and documents the insurer’s unreasonable delay or denial preserves your rights under this statute — adding meaningful financial pressure that often accelerates resolution of coverage disputes that would otherwise drag on for months. The Georgia Insurance Commissioner’s complaint portal also provides a regulatory mechanism to document insurer bad faith conduct in your claim file.

Frequently Asked Questions — Unlicensed Driver Georgia Insurance Liability

| Question | Answer |

|---|---|

| Does an unlicensed driver’s lack of license void their insurance? | Not automatically. In Georgia, insurance follows the vehicle. The vehicle owner’s policy typically covers damages regardless of the driver’s license status, though the insurer may dispute coverage and litigation may be required. |

| What if the unlicensed driver has no insurance at all? | Your own uninsured motorist coverage under O.C.G.A. § 33-7-11 becomes the primary recovery mechanism. UM coverage compensates you as if the at-fault driver had carried liability coverage up to your policy limit. |

| Can I sue the vehicle owner for letting an unlicensed driver use their car? | Yes, under Georgia’s negligent entrustment doctrine, if the owner knew or should have known the driver was unlicensed or incompetent, you can pursue a direct claim against the owner. |

| What is the minimum liability insurance in Georgia? | $25,000 per person / $50,000 per occurrence for bodily injury under O.C.G.A. § 40-9-37. In serious injury cases, these minimums are often insufficient — which is why your own UM coverage matters. |

| Does driving without a license make the driver automatically negligent in Georgia? | Under Georgia’s negligence per se doctrine, violating O.C.G.A. § 40-5-20 by driving unlicensed can establish negligence as a matter of law in the context of causing a collision. |

| How long do I have to file a claim in Georgia? | Two years from the accident date under O.C.G.A. § 9-3-33. Do not wait — the coverage investigation alone can take weeks, and building a negligent entrustment claim requires early evidence preservation. |

| Should I give a recorded statement to my own UM insurer? | Speak with an attorney first. Even your own UM carrier can use recorded statements to limit your payout. An attorney ensures your statement does not inadvertently harm your claim. |

| What if the unlicensed driver flees the scene? | A hit-and-run with an unidentified driver triggers your uninsured motorist coverage under Georgia law, provided you report the accident to law enforcement promptly. Physical contact with the vehicle is required under most Georgia UM policies. |

Practical rule: Every Georgia driver should carry uninsured motorist coverage at the highest limit they can reasonably afford. You cannot control whether the driver who hits you has a license or insurance — but you can control how protected you are when they do not.

Get the Full Compensation You Deserve After an Unlicensed Driver Accident in Georgia

Being hit by an unlicensed driver in Georgia does not mean your options are limited — it means the path to compensation requires a more thorough investigation of every available coverage layer. In many cases, injured victims recover full compensation through a combination of the vehicle owner’s liability policy, a negligent entrustment claim against the owner, and their own uninsured motorist coverage working together. Jamie Ballard Law handles unlicensed driver accident cases in Atlanta and throughout Georgia, identifying all sources of recovery — vehicle owner liability, negligent entrustment claims, and UM coverage — to maximize what you receive. Call (404) 885-8544 or visit the contact page to speak with a Georgia personal injury attorney at no cost — free consultations are always available.

About Jamie Ballard Law

Jamie Ballard Law is an Atlanta-based personal injury firm representing injured Georgians in car accident cases, including collisions caused by unlicensed, uninsured, and underinsured drivers throughout metro Atlanta and the state of Georgia. The firm handles every phase of the case — from initial insurance coverage investigation and evidence preservation through demand, mediation, and trial if necessary — providing direct attorney access, transparent communication, and results-driven representation at every stage. No fees are charged unless the firm recovers compensation for you.