When you're driving in Atlanta, understanding what is uninsured motorist coverage is one of the smartest things you can do for your financial well-being. At its heart, this is a special part of your own car insurance that pays for your injuries and damages if the driver who hits you has no insurance, not enough insurance, or flees the scene in a hit-and-run.

It's a shield you put in place to protect yourself from another person's lack of responsibility.

Your Financial Shield After a Crash

A car wreck is upsetting enough. Discovering the other driver is uninsured can turn a stressful event into a financial disaster. Suddenly, you're looking at growing medical bills, lost time from work, and no obvious way to get those costs covered.

This is exactly why uninsured motorist (UM) coverage exists. You can think of it as a reserve fund you've set aside just for this type of situation. Instead of the headache of trying to sue a driver who likely has no money, you make a claim directly with your own insurance company. Your policy steps up to pay for the harm the at-fault driver should have covered.

What Does It Actually Cover?

UM coverage is built to handle the real costs of a serious accident. It's about much more than just fixing your car—it’s about taking care of you and your family.

Let’s quickly review what Uninsured Motorist (UM) and its partner, Underinsured Motorist (UIM), coverage typically handle.

UM Coverage at a Glance

| Coverage Type | What It Covers |

|---|---|

| Uninsured Motorist (UM) | Covers your costs when the at-fault driver has no liability insurance at all. This includes medical bills, lost income, and pain and suffering. |

| Underinsured Motorist (UIM) | Kicks in when the at-fault driver has insurance, but their policy limits are too low to cover the full extent of your damages. |

This table provides a quick look, but how it works in the real world is what truly matters.

Here’s a breakdown of what UM/UIM can pay for:

- Medical Bills: This covers everything from the ambulance ride and emergency room treatment to surgery, physical therapy, and any future medical care you might need.

- Lost Income: If your injuries keep you out of work, this coverage helps replace your lost paychecks, helping you focus on recovery without financial strain.

- Pain and Suffering: The physical pain and emotional toll from an accident are very real. UM coverage can provide payment for these non-economic damages.

The unfortunate truth is that a surprising number of drivers are on the road without proper insurance. The Insurance Information Institute tracks this data, and the percentage of uninsured drivers highlights a significant risk on our roads.

Uninsured motorist coverage essentially steps into the shoes of the at-fault driver. It ensures you have a source of financial recovery when the person who caused your injuries has none.

This coverage is your first line of defense, protecting your financial stability when you need it most. It ensures that another person's irresponsibility doesn’t derail your life. Understanding your rights is a key part of the process, and you can learn more about handling different types of personal injury claims on our website. Without this protection, you could be stuck paying for everything yourself.

Why This Coverage Is So Important in Georgia

https://www.youtube.com/embed/ROliJ27Br9A

While Georgia law doesn't make drivers carry uninsured motorist (UM) coverage, deciding to go without it is a big financial gamble. The reality is that many drivers on our roads have no insurance. If one of them causes a wreck, you could be left paying for every single expense.

Think about this situation: You're driving on I-285 during rush hour when a car swerves into your lane, causing a multi-car pile-up before speeding off. You're left with a damaged car and a serious back injury. In a hit-and-run, the at-fault driver is legally considered uninsured. Without UM coverage, you're on your own.

The Real Costs of a Wreck

The expenses after a crash can add up with shocking speed, especially here in Atlanta. We’re not just talking about a few thousand dollars for car repairs; the impact on people is often huge.

Here’s a look at what you could be facing:

- Emergency Room Visits: Even for what seems like a minor injury, a single trip to the ER can easily cost thousands.

- Ongoing Medical Care: Serious injuries often require follow-up care, like physical therapy, appointments with specialists, and sometimes, future surgeries.

- Lost Paychecks: If your injuries keep you out of work, your income stops. That puts immediate and immense strain on your ability to pay your mortgage, rent, and other bills.

This is exactly why knowing what uninsured motorist coverage is becomes so important. It serves as your personal financial safety net, stepping in to fill the huge gap left by an uninsured or hit-and-run driver. It's there to protect your health, your family, and your financial future.

The Georgia Office of Insurance and Safety Fire Commissioner offers resources for consumers, making it clear what types of auto coverage are available.

This official resource confirms that while only liability coverage is mandatory, protections like UM are offered for your benefit.

The main purpose of UM coverage is to ensure you aren't financially ruined by someone else's irresponsibility. It’s a shield for your savings and your future.

It's also important to act quickly after an accident. There are strict deadlines for taking legal action. You can learn more about the statute of limitations for personal injury in Georgia to ensure your rights are protected. In the end, having solid uninsured motorist coverage is one of the smartest decisions a Georgia driver can make.

Understanding Your Two Types of UM Protection

It’s a common misunderstanding among Georgia drivers that Uninsured Motorist (UM) coverage is just one thing. In truth, it’s divided into two different parts. Each one is designed to protect a different part of your life if you’re in an accident with a driver who has no insurance.

Understanding this difference is key to knowing exactly what your policy covers and where you might have gaps. These two parts work together to create a stronger financial barrier against both the personal and property costs that follow a wreck.

Uninsured Motorist Bodily Injury (UMBI)

The first part, Uninsured Motorist Bodily Injury (UMBI), is all about taking care of people. When an uninsured driver injures you or your passengers, this is the coverage that steps in to handle the growing medical expenses and related costs.

You can think of it as a vital line of defense for your physical and financial health. UMBI is meant to pay for the kinds of expenses that can quickly get out of hand, such as:

- Medical and Hospital Bills: This includes everything from the initial ambulance ride and emergency room visit to surgery and long-term physical therapy.

- Lost Wages: If your injuries leave you unable to work, UMBI helps replace that lost income so you can keep your finances stable.

- Pain and Suffering: This is payment for the physical pain and emotional distress that a serious crash causes.

This coverage lets you focus on what really matters—your recovery—without the constant stress of figuring out how to pay for everything. For clear definitions of other important legal terms, you can always reference our firm’s helpful legal dictionary.

Uninsured Motorist Property Damage (UMPD)

While UMBI covers injuries to people, Uninsured Motorist Property Damage (UMPD) protects your vehicle. If an uninsured driver damages or even totals your car, UMPD is there to cover the cost of repairs or help you get a replacement.

To put it simply: UMBI protects you and your passengers. UMPD protects your car. Having both gives you a much more complete layer of security.

The threat from uninsured drivers on the road is real. Statistics consistently show that a meaningful percentage of drivers—around one in seven or eight—operate their vehicles without insurance. This highlights just how important it is to have your own protective coverage in place.

With a clear understanding of both UMBI and UMPD, you can see the full picture of what this important coverage does to protect you, your family, and your property from the careless actions of others.

Stacked Versus Unstacked UM Policies Explained

When you’re looking into your auto insurance options, you’ll likely see the terms "stacked" and "unstacked" UM coverage. It might sound like insurance jargon, but the difference is straightforward—and it dramatically changes how much protection you actually have after a crash.

Making the right choice here is a big step toward building a real financial safety net.

In short, stacking lets you combine the uninsured motorist coverage limits from multiple vehicles on your policy. This creates a much larger pool of money you can access if a driver with no insurance leaves you with serious injuries.

A Real-World Example of Stacking

Let’s make this clear. Imagine your family owns two cars, and you’ve insured each one with a $50,000 Uninsured Motorist Bodily Injury (UMBI) limit.

- If you have a stacked policy, you can combine those limits. If you get into a serious wreck in either car, you now have access to a total of $100,000 ($50,000 + $50,000) to cover your medical bills, lost income, and other damages.

- With an unstacked policy, you're limited to the coverage on the single vehicle involved in the accident. In the same situation, you could only access $50,000, no matter how serious your injuries are.

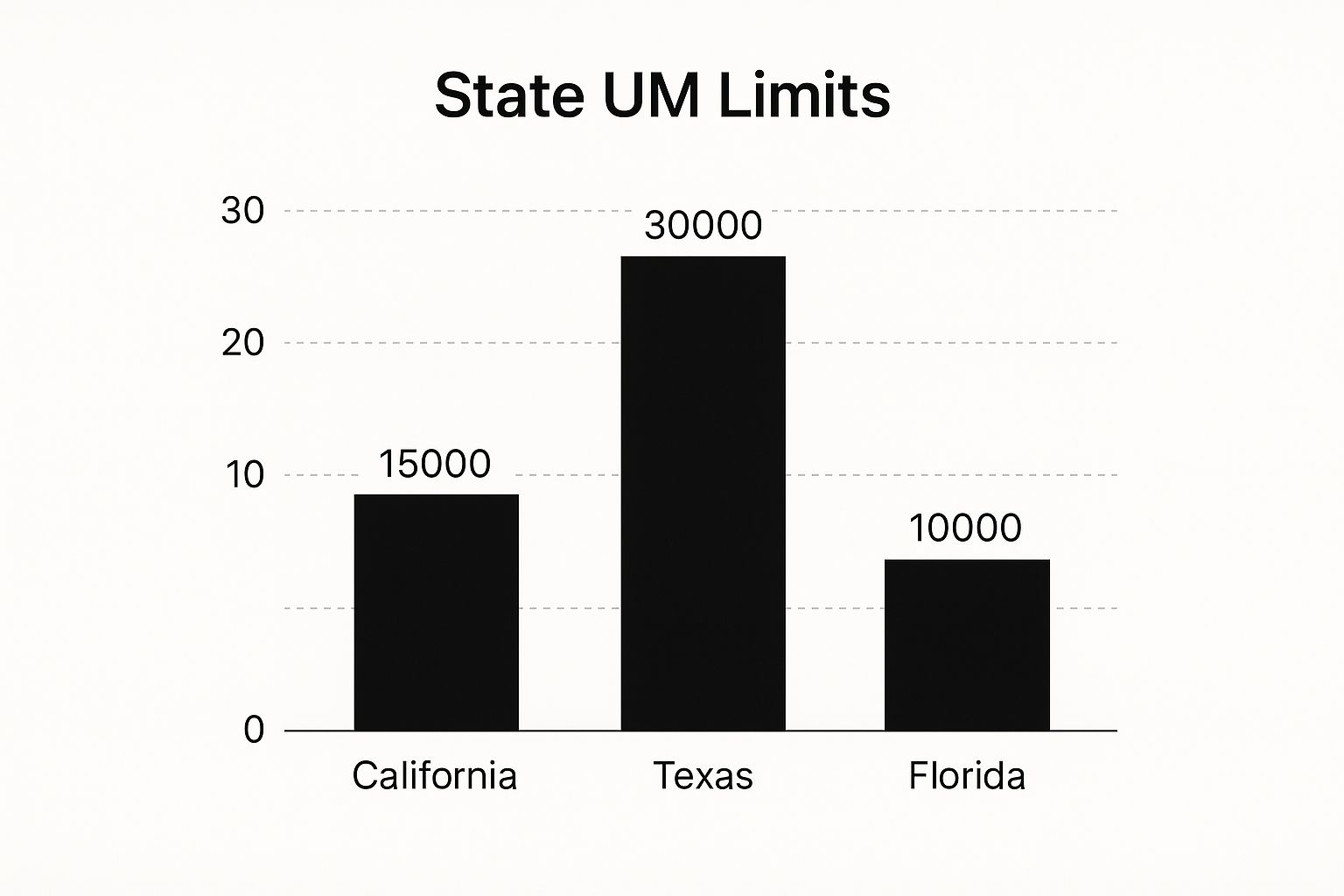

This infographic shows just how little coverage some states require drivers to carry.

As you can see, those state minimums are often very low. It’s a clear reminder of why you can't depend on the other driver to be properly insured.

To make the difference even clearer, here's a direct comparison using our two-car family example.

Stacked vs. Unstacked UM Coverage Example

| Policy Type | Coverage Limit Per Car | Total Available Coverage After an Accident |

|---|---|---|

| Stacked | $50,000 | $100,000 (Both cars' limits combined) |

| Unstacked | $50,000 | $50,000 (Limited to the single car involved) |

The math is simple, and the benefit is powerful. Stacking doubles your protection.

Why Does This Choice Matter?

A single serious accident can easily create medical costs well over $100,000. Stacking your UM coverage gives you a much higher limit, usually for a very small increase in your premium. It's one of the most effective ways to give your family a meaningful layer of financial protection.

Unstacked UM coverage caps your recovery at one car's limit. Stacked UM coverage multiplies your protection by the number of cars on your policy, offering a much stronger defense against major financial loss.

Not every state allows stacking, but fortunately, Georgia does. You can find more details on how different states handle auto insurance from trusted sources like the Insurance Information Institute.

When you're talking with your insurance agent about what is uninsured motorist coverage, be sure to ask specifically about your options for stacking. It’s a conversation that could be worth hundreds of thousands of dollars one day.

How to File an Uninsured Motorist Claim

Knowing you have uninsured motorist coverage is one thing; using it after a wreck is another matter. The time after an accident is often chaotic, but the path to filing a UM claim can be broken down into a clear, step-by-step process. Following these steps from the start protects your right to payment.

Remember, you are now filing a claim with your own insurance company. While they are your insurer, their goal is still to limit what they pay out. This makes clear records and quick communication your most powerful tools.

Immediate Steps to Take After the Accident

What you do in the first few hours after a collision sets the stage for your entire claim. Your first priority is always safety, but gathering key information is a very close second.

Here’s a simple checklist of what to do right at the scene:

- Call 911 Immediately: Even if the crash seems minor, a police report is very important evidence. It creates an official record of the accident, identifies everyone involved, and often includes the officer’s initial thoughts on who was at fault.

- Seek Medical Attention: Get a medical evaluation as soon as you can, even if you feel fine. Adrenaline can easily hide serious injuries, and a medical record from the day of the crash directly links your injuries to the collision.

- Gather Evidence Safely: If it’s safe to move around, use your phone to take pictures and videos of everything. Document the damage to all cars, skid marks on the road, the weather conditions, and any visible injuries.

- Notify Your Insurer: Report the accident to your own insurance company right away. Tell them you were hit by an uninsured driver or that the other driver fled the scene. This is the first step that officially opens your claim.

Building Your Claim with Documentation

After you open a claim, your insurance company will assign an adjuster to your case. It’s now your job to give them all the evidence they need to approve your claim and cover your damages. This means keeping detailed records.

Keep every bill, receipt, and doctor’s note organized in one place. The more detailed your documentation is, the stronger your position will be when it comes time to work out a fair settlement.

As you move forward, it's also smart to understand common issues. You can learn more about why an insurance company might refuse to pay a claim from various online guides. For a complete breakdown of the claims process, see our article on how to file a car accident claim in Atlanta. This is how you take the idea of uninsured motorist coverage and put it to work for you.

Frequently Asked Questions About Uninsured Motorist Coverage

Even after you learn the basics, it's normal to have more questions about uninsured motorist coverage. We hear them all the time from our clients here in Atlanta. Let's walk through a few of the most common ones to give you some clarity.

Getting these details right isn't just about insurance—it's about making sure you’re ready to protect your family's financial security if something unexpected happens.

Does Uninsured Motorist Coverage Apply to Hit and Run Accidents?

Yes, it absolutely does. In Georgia, a hit-and-run accident is a primary example of when UM coverage is designed to step in and protect you. Since the at-fault driver fled and can't be identified, the law treats them as an uninsured driver.

This is a key reason why filing a police report is so important after any crash, especially a hit-and-run. Insurance companies will almost always require an official report to process a UM claim in these situations. It serves as strong evidence and confirms your account of what happened.

Is UM Coverage Required in Georgia?

No, Georgia law doesn't make drivers carry Uninsured/Underinsured Motorist (UM/UIM) coverage. However, insurers are legally required to offer it to you in writing whenever you buy a standard liability policy.

If you decide against it, you must formally reject the coverage in writing. While it’s optional, we see it as necessary protection for every Georgia driver. You can find more details on state insurance rules on official resources like the Georgia state website.

Will My Insurance Rates Go Up if I File a UM Claim?

Filing a UM claim should not cause your insurance rates to increase. Georgia law generally prohibits insurers from penalizing you for using your own coverage for an accident that wasn't your fault. You are simply using a benefit you've already paid for through your premiums.

Think of it this way: You're using your coverage as a shield against someone else's mistake. You shouldn't be penalized for protecting yourself when another driver was negligent.

What Is the Difference Between Uninsured and Underinsured Coverage?

The difference is simple and depends entirely on the at-fault driver’s insurance situation.

- Uninsured Motorist (UM) Coverage: This kicks in when the at-fault driver has no liability insurance at all.

- Underinsured Motorist (UIM) Coverage: This applies when the at-fault driver does have insurance, but their policy limits are too low to cover the full extent of your damages.

Here in Georgia, these two protections are typically sold together in a single UM/UIM policy. This creates a safety net for both situations, ensuring you have a clear path to recovery and fully answering the question of what is uninsured motorist coverage and how it works for you on the road.

If you've been injured in an accident with an uninsured driver, the path forward can seem uncertain. At Jamie Ballard Law, we are here to provide the clarity and support you need. Contact us today for a free, no-obligation case evaluation to understand your rights and options. Let us help you get the compensation you deserve. Visit us at https://jamieballardlaw.com.