If you've ever been in a car wreck in Atlanta, you know the immediate chaos is just the beginning. The real stress often starts when you discover the at-fault driver’s insurance policy won't come close to covering your medical bills, lost wages, and other mounting expenses.

This is a frustratingly common scenario. So, what does underinsured motorist cover? It's the extra layer of protection on your own auto policy that kicks in when the at-fault driver's liability insurance runs out. It is a vital tool for your financial protection.

Your Financial Safety Net After a Wreck

The best way to think about Underinsured Motorist (UIM) coverage is as a financial backstop you set up for yourself. It’s there specifically to protect you from other drivers who only carry the bare minimum insurance required by law—which is rarely enough to cover the costs of a serious accident.

Here’s how it works. When another driver causes a collision, their liability insurance is the first to pay for your damages. But what happens when your medical bills and lost income far exceed their policy limits? You could be left with a massive financial burden.

This is precisely the gap your UIM coverage is designed to fill. It pays the difference between your total damages and what the at-fault driver's insurance paid out, up to the limits of your own UIM policy.

In Georgia, the state-mandated minimum liability coverage is just $25,000 per person. A single trip to the emergency room, let alone ongoing treatment or surgery, can easily wipe that out. That’s why having adequate UIM coverage is one of the smartest decisions you can make to protect your family’s financial future.

Knowing how to properly file and manage these personal injury claims is key to getting the compensation you deserve. This guide will walk you through exactly what underinsured motorist coverage includes so you can move forward with confidence.

Uninsured vs. Underinsured Motorist Coverage Explained

It’s easy to get ‘uninsured’ and ‘underinsured’ motorist coverage mixed up, but they solve two very different problems you might face after a car wreck in Atlanta. Think of them as your personal safety net—they protect you, not the other driver. Understanding what each one does is the first step toward making sure you’re properly covered.

First, Uninsured Motorist (UM) coverage protects you when the at-fault driver has no insurance at all. This also comes into play in those frustrating hit-and-run scenarios where the driver flees the scene and can’t be found.

So, what does underinsured motorist cover? Underinsured Motorist (UIM) coverage applies when the at-fault driver does have insurance, but their policy limits are too low to cover all your damages. This is an incredibly common problem, since many drivers carry only the bare minimum required by the state.

A Clear Comparison

Let's put this into a real-world context. Georgia law only requires drivers to carry $25,000 in bodily injury liability coverage per person. If your medical bills and lost wages add up to $90,000, that minimum policy leaves a staggering $65,000 gap. This is precisely where your UIM coverage is designed to step in and make you whole.

You can learn more about Georgia's minimum requirements directly from the Georgia Department of Driver Services.

To make it even clearer, this table breaks down the key differences between these two coverages.

Uninsured (UM) vs. Underinsured (UIM) Coverage At a Glance

| Coverage Type | At-Fault Driver's Status | When It Applies | Example Scenario |

|---|---|---|---|

| Uninsured Motorist (UM) | Has no auto insurance policy or is an unknown hit-and-run driver. | You are hit by a driver who illegally let their insurance lapse or who flees the scene. | Your medical bills are $40,000. The at-fault driver has no insurance, so your UM coverage steps in to pay for your damages. |

| Underinsured Motorist (UIM) | Has an active insurance policy, but the liability limits are insufficient. | The at-fault driver’s insurance pays its full policy limit, but your damages exceed that amount. | Your medical bills are $90,000. The at-fault driver's policy pays its $25,000 limit. Your UIM coverage can then pay the remaining $65,000. |

While they sound similar, UM and UIM are triggered by entirely different circumstances. Both exist to ensure you aren't left paying out-of-pocket for someone else's mistake. Knowing exactly what underinsured motorist coverage means is essential for protecting your financial well-being after an accident.

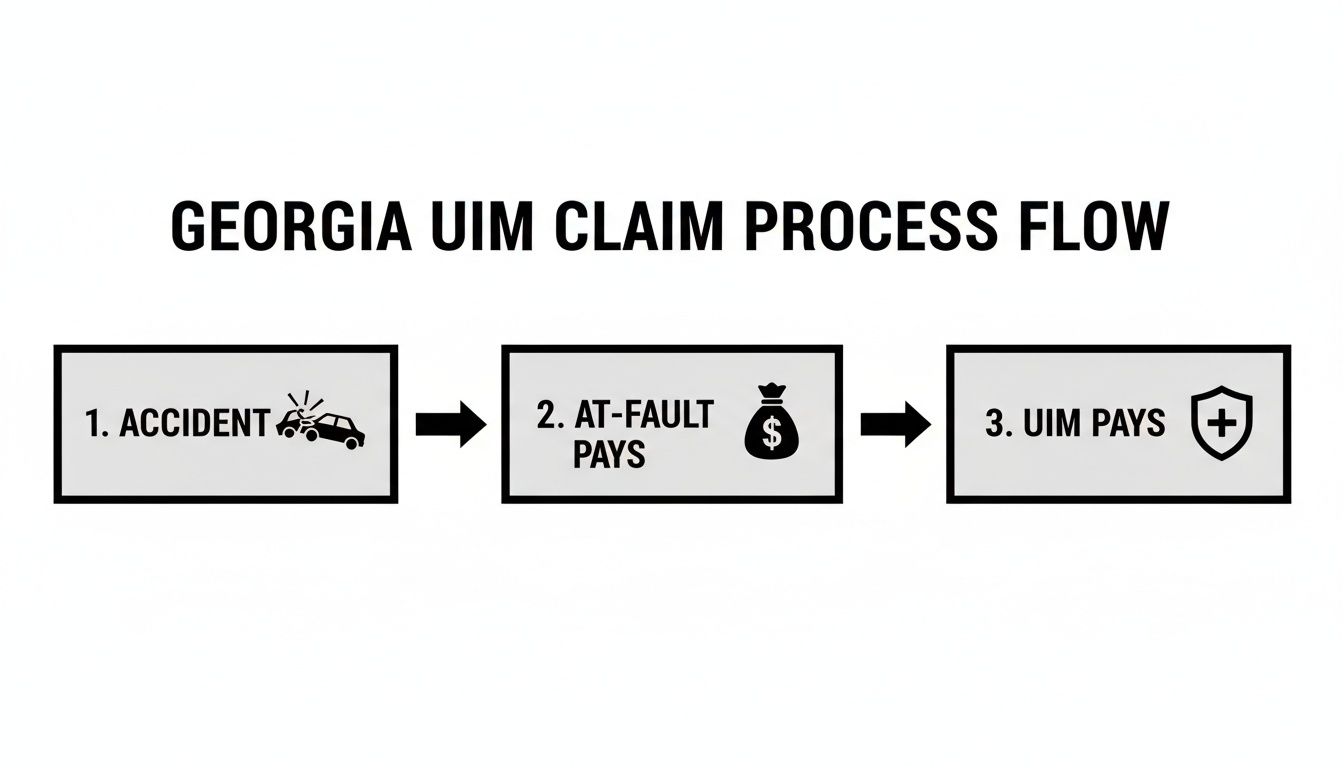

How UIM Coverage Works in Georgia Step by Step

Knowing what does underinsured motorist cover is the first step, but the real key is understanding how to actually get those benefits when you need them. The process in Georgia isn't automatic—it follows a specific sequence. You have to go after the at-fault driver's insurance first before your own policy can kick in.

It all starts with the driver who hit you. Before you can even think about your UIM coverage, you must file a claim against their insurance and push for the maximum possible payout from their bodily injury liability policy.

This means you need to fully resolve that initial claim. Typically, this ends with their insurance company "tendering," or offering, their full policy limit. Only after their insurer has paid its absolute maximum can you turn to your own insurance company to open an underinsured motorist claim.

The Georgia "Add-On" Rule

Here’s some good news for Georgia drivers: our state uses what’s called an “add-on” or “excess” UIM system. This is a huge advantage. It means your UIM coverage limit is added on top of whatever the at-fault driver’s insurance pays out.

Let’s walk through a quick example:

- Your total damages from the accident (medical bills, lost income, etc.) come to $125,000.

- The at-fault driver only has the state minimum liability coverage of $25,000.

- You, fortunately, have $100,000 in UIM coverage.

Under Georgia's add-on rule, you would first collect the $25,000 from the other driver's insurance. After that, you can file a claim with your own insurer for the remaining $100,000 in damages, tapping into your full UIM policy. The add-on system ensures you can access the full value of the coverage you paid for. The claim process itself has a lot of moving parts, and you can learn more about how to file a car accident claim in Atlanta in our detailed guide.

Understanding UIM Stacking in Georgia

"Stacking" is another powerful tool available under Georgia law. If your auto insurance policy covers multiple vehicles, you might be able to "stack" the UIM coverage from each vehicle to create a much larger pool of money to draw from.

Here’s how stacking works:

- Let's say you have three cars insured on your policy.

- Each car has $50,000 in UIM coverage.

- By stacking them, you could create a potential UIM limit of $150,000 ($50,000 x 3 cars).

This can be a complete game-changer in crashes involving serious injuries, where medical costs can skyrocket past a single policy's limit in no time. Whether you can stack your coverage depends entirely on the language in your specific insurance policy, so it's always smart to read it carefully.

Why This Coverage Is So Important

The hard truth is that a shocking number of drivers are on the road without enough insurance to cover the damage they might cause. The risk is very pronounced for those of us in Atlanta and throughout the state. According to a 2021 study by the Insurance Research Council, 12.4% of Georgia drivers are completely uninsured, ranking us 16th highest in the nation. Many more are underinsured.

This means there's a very real chance the person who hits you won't have anywhere near enough insurance to cover your losses. That’s precisely why your own UIM coverage is so essential.

Understanding what does underinsured motorist cover isn't just a technical exercise—it’s a key piece of financial protection for every driver in Georgia. Knowing the step-by-step process, from exhausting the other driver's policy to using the add-on rule and stacking, gives you the power to demand the full compensation you're entitled to. For more official information, you can check the consumer guides from the Georgia Office of Insurance and Safety Fire Commissioner.

What an Underinsured Motorist Policy Actually Pays For

When you have to file an underinsured motorist claim, it's easy to think it's just for covering the immediate hospital bills. But the real answer to what does underinsured motorist cover is much broader. This coverage is designed to pay for the full range of damages the at-fault driver's insurance should have paid for if their policy limits were high enough.

Your UIM policy is there to step into the other driver's shoes and make you whole again. It's not just about patching up your car; it's about addressing the complete physical, financial, and emotional fallout from the collision.

Breaking Down the Types of Compensation

So, what can you actually get paid for? UIM coverage is comprehensive and is meant to support every part of your recovery. The goal is to put you back in the financial position you were in right before the crash.

Here are the main categories of damages your UIM policy can cover:

- All Related Medical Expenses: This is the most obvious part. It covers every medical bill tied to the accident—the ambulance ride, ER treatment, hospital stays, and surgeries. It also pays for ongoing needs like physical therapy, chiropractic adjustments, prescriptions, and any future medical procedures your doctors expect you'll need.

- Lost Wages and Income: If your injuries keep you out of work, UIM can reimburse you for the paychecks you missed. This is based on what you would have earned during your recovery.

- Loss of Future Earning Capacity: Some injuries are permanent. They might prevent you from returning to your old job or earning the same income you did before the wreck. This part of your claim addresses that long-term financial devastation, which can be significant.

This flowchart shows the straightforward process of how a UIM claim works here in Georgia after an accident.

As you can see, your UIM coverage is that final, essential step in the process, filling the gap the at-fault driver’s cheap policy left behind.

Covering the Non-Economic Damages

Beyond the stack of bills and lost paychecks, a serious accident takes a massive human toll. Your UIM coverage is also there to compensate you for these less tangible, but equally real, losses. We call these "non-economic damages."

These damages are deeply personal and different for every single person, but they are a legitimate part of your claim.

A common myth is that UIM coverage is only for financial losses. In reality, it also provides compensation for the physical pain and emotional distress you've endured, which are often the hardest parts of recovering from a serious wreck. You can find general information about your rights as a consumer from sources like the Federal Trade Commission.

Here’s what these non-economic damages typically include:

- Pain and Suffering: This compensates you for the actual physical pain, discomfort, and chronic suffering caused by your injuries.

- Emotional Distress: A wreck can cause severe mental anguish, including anxiety, depression, a new fear of driving, and even post-traumatic stress disorder (PTSD).

- Loss of Enjoyment of Life: This is about how your injuries have robbed you of your ability to participate in hobbies, recreational activities, and daily routines that you once enjoyed.

By covering both the economic and non-economic harm you've suffered, your policy provides a more complete path to financial recovery. Knowing exactly what does underinsured motorist cover is the first and most important step toward making sure you demand—and receive—a fair settlement from your own insurance company after a crash.

Common Hurdles When Filing a UIM Claim

You’d think filing a claim with your own insurance company would be a straightforward, supportive process. After all, you’ve faithfully paid your premiums for this exact situation. But once you file a UIM claim, the dynamic can shift dramatically. Suddenly, your insurer might start acting more like an opponent than an ally, laser-focused on minimizing their payout.

Knowing what obstacles to expect can make a huge difference. Their goal is to protect their bottom line, which means they will scrutinize every single detail of your claim. Being prepared for their tactics is the best way to protect your right to a fair recovery.

Questioning Your Injuries and Treatment

One of the first and most common challenges is having the adjuster question the severity of your injuries. They might imply your medical treatments weren't truly necessary or even suggest you’re exaggerating your pain. It’s a classic tactic used to justify offering you far less than you deserve.

An adjuster might try to argue that:

- Your injuries were pre-existing and not actually caused by this accident.

- There's a "gap in treatment," meaning you waited too long after the wreck to see a doctor.

- The type of care you received—like physical therapy or chiropractic adjustments—was excessive for the injuries documented in the accident report.

This is precisely why consistent and thorough medical documentation is non-negotiable. Every doctor's visit, prescription, and therapy session helps build a rock-solid record that directly links your injuries to the accident, making it much harder for them to dispute your claim.

The Lowball Settlement Offer

Another frequent hurdle is the quick, but unfairly low, settlement offer. The insurance company knows you're likely stressed, facing a mountain of medical bills, and possibly out of work. They dangle a small amount of cash, hoping you’ll take it out of desperation.

Rest assured, that first offer is almost never their best one.

Don't be tempted to accept the first offer, especially if you're still undergoing medical treatment. A fast settlement is often a sign that the insurer knows your claim is worth much more and they want to close it before you realize its true value.

They are betting you don’t understand the full value of your claim. An offer that fails to account for your future medical needs, lost earning capacity, and the real-world impact the injury has had on your life is not a fair offer.

Procedural Roadblocks and Deadlines

Insurance policies are legal contracts, packed with specific rules, procedures, and deadlines you must follow to the letter. Missing a single step can give your insurer the excuse they need to deny your claim entirely. For example, most policies require you to notify them of a potential UIM claim within a very specific timeframe.

Here in Georgia, there’s another important rule: you cannot settle with the at-fault driver's insurance company without first getting written permission from your own UIM carrier. If you cash their check and sign a release without your insurer's consent, you could immediately forfeit your right to any UIM benefits. It’s a simple mistake that can have devastating financial consequences.

Understanding the specific statute of limitations for personal injury in GA is also vital, as these legal deadlines are strict and unforgiving.

Ultimately, knowing what underinsured motorist coverage is only gets you to the starting line. Successfully handling the claims process to get the compensation you're truly owed is a whole different race.

Why You Might Need an Advocate for Your Atlanta UIM Claim

When you’re recovering from a serious accident, the absolute last thing you need is a fight with your own insurance company. You’ve faithfully paid your UIM premiums for this exact scenario, yet when it’s time to file a claim, you might discover your insurer is far less cooperative than you’d expect.

This is precisely where a skilled personal injury attorney becomes your most important asset. An attorney acts as your dedicated advocate, managing the stressful back-and-forth with both the at-fault driver’s insurance and your own UIM carrier. They know exactly what evidence is required to build a powerful claim—from detailed medical records to expert opinions and proof of lost income—freeing you to focus on healing.

Leveling the Playing Field

Insurance companies are not on your side; they are businesses. They process thousands of claims annually, employing teams of adjusters and lawyers whose primary job is to protect the company's bottom line. That often means minimizing payouts or finding reasons to deny claims altogether. Going it alone puts you at a severe disadvantage.

An attorney levels that playing field. They have an in-depth understanding of Georgia's insurance laws, ensuring that every legal notice is correctly filed and every deadline is met without fail.

Here’s how a legal advocate makes a difference:

- Accurate Claim Valuation: An attorney will meticulously assess every facet of your damages—including projected medical needs and long-term pain and suffering—to calculate the true value of your claim, not just the lowball figure an adjuster offers.

- Strategic Negotiation: Armed with compelling evidence, they will negotiate forcefully on your behalf, demanding a settlement that fully and fairly compensates you for your losses.

- Litigation Readiness: If the insurance company refuses to make a fair offer, your attorney is prepared to take them to court and fight for the compensation you are rightfully owed.

The Reality of Underinsured Drivers in Georgia

The need for this advocacy is driven by a sobering fact: Georgia’s roads are filled with underinsured drivers. Your UIM coverage is the safety net designed to protect you when the at-fault driver’s liability limits are too low to cover your medical bills and other losses.

In Georgia, the minimum bodily injury liability limit is just $25,000—an amount that can be exhausted by a single emergency room visit. Consider this: a single night in a trauma center can easily cost over $50,000. According to a 2021 report from the Insurance Research Council (IRC), an alarming 12.4% of Georgia drivers were uninsured. If you’re hit by one of them, your own policy is your primary path to recovery.

Having professional representation ensures you are not just another claim number. It means having someone in your corner who is committed to making sure your voice is heard and your rights are protected.

An experienced lawyer also shields you from the common tactics insurers use to undervalue or outright deny legitimate claims. If you’re injured and facing a frustrating UIM process, you need to understand your options.

Ultimately, having a skilled advocate manage your claim removes an immense burden from your shoulders. It provides the peace of mind to recover without the added stress of legal battles. They handle the paperwork, the phone calls, and the negotiations, ensuring every detail is managed correctly while fighting to secure the financial resources you need to rebuild your life.

Georgia UIM Claims: Your Questions Answered

When you're trying to figure out your next steps after a wreck, the insurance details can feel overwhelming. People often ask us the same key questions about underinsured motorist claims in Georgia. Here are some straightforward answers to the most common concerns.

Can I Still Make a UIM Claim if I Was Partially at Fault?

Yes, you can, but there's an important threshold. Georgia operates under a modified comparative negligence rule. This means you can recover damages as long as you are not found to be 50% or more responsible for the crash.

Your final compensation from the at-fault driver and your own UIM policy will be reduced by your percentage of fault. For example, if you have $100,000 in damages but are found to be 10% at fault, your recoverable amount drops to $90,000. Your UIM coverage would kick in if that $90,000 still exceeds the other driver’s liability limits. These legal standards are outlined in the official Code of Georgia.

What Happens if My Insurance Company Denies My UIM Claim?

A denial from your own insurance company is frustrating, but it is not the final word. You have the right to challenge their decision.

The first step is to demand a detailed, written explanation for the denial. Insurers are legally required to provide a valid reason based on your policy's specific language and the facts of the case.

Common reasons for a UIM denial include:

- Disputes over liability and who was at fault for the accident.

- Arguments that your medical care wasn't necessary or was unrelated to the collision.

- Claims that you missed a deadline or made a procedural error.

An experienced attorney can scrutinize the denial letter, compare it to your policy, and determine if the insurer is acting in bad faith. If they are, you may be able to file a lawsuit directly against them to force them to pay the benefits you're rightfully owed.

How Long Do I Have to File a UIM Claim in Georgia?

This is where things get very time-sensitive. The statute of limitations for filing a personal injury lawsuit in Georgia is generally two years from the date of the accident. Your UIM claim is directly tied to this two-year clock.

While you should always notify your insurer of a potential claim right away, there is a legal step you absolutely cannot miss.

To preserve your right to make a UIM claim, you must file a lawsuit against the at-fault driver and formally serve your UIM insurance company with a copy of that lawsuit. This must be done before the two-year statute of limitations expires.

Missing this strict procedural requirement will permanently bar you from recovering anything from your UIM policy. It’s a simple but unforgiving mistake that can cost you everything. Understanding what does underinsured motorist cover is the first step, but following the correct legal procedures is what ensures you can actually use it.