Getting into a car wreck is jarring. When the other driver speeds off, it adds a whole new layer of confusion and anger to an already stressful situation. One of the first questions that races through your mind is, "Who's going to pay for this?"

This leads to a question we hear all the time from people in Atlanta: does uninsured motorist cover hit and run accidents?

The answer, thankfully, is yes. In Georgia, this specific coverage is designed to protect you in exactly this type of scenario.

Your Guide to Hit-and-Runs and Uninsured Motorist Coverage

Think of your Uninsured Motorist (UM) coverage as your financial safety net. It’s there to catch you when the driver who caused the crash either has zero insurance or, in the case of a hit-and-run, can't be identified.

When a driver vanishes after a collision, you’re left with no one to hold accountable and no insurance company to file a claim against. That’s precisely where your own policy steps in to help.

Georgia law effectively treats that unknown, "phantom" driver as an uninsured one. This legal interpretation is what allows you to turn to your own insurance provider and access your UM benefits to cover your injuries.

How This Coverage Actually Works for You

Your UM policy is specifically there to cover your losses when you're hurt by a driver who can't—or won't—pay. Because the at-fault driver in a hit-and-run is impossible to identify, the insurance industry and Georgia law treat the situation as an uninsured motorist event.

This means your UM coverage can step up to pay for:

- Medical bills from the emergency room, doctors' visits, and physical therapy.

- Lost income if your injuries prevent you from working.

- Pain and suffering and other related damages.

This protection is a foundation of many personal injury claims, giving you a clear path to financial recovery even when the person responsible is long gone.

Key Takeaway: Your Uninsured Motorist policy is your first line of defense after a hit-and-run. It’s designed to fill the void left by the missing at-fault driver, providing a source of funds for your medical treatment and other losses.

Ultimately, your UM coverage was created for this exact nightmare scenario. It ensures that a driver who breaks the law by fleeing doesn't also leave you footing the bill for your own recovery. We'll break down exactly how this works under Georgia law, so you can feel confident in your next steps and understand how an uninsured motorist policy can cover a hit-and-run.

Phantom Drivers vs. Uninsured Drivers: What's the Difference?

When someone hits your car and speeds off, it raises an important question: does uninsured motorist cover hit and run accidents? In Georgia, the answer is usually yes, but it’s helpful to understand the difference between a driver who stays at the scene without insurance and one who vanishes.

If an uninsured driver hits you but remains at the scene, you at least have a target. You know who they are. Even though they don't have insurance, you can hold them accountable by filing a personal injury lawsuit against them directly.

The Problem of the "Phantom Driver"

A hit-and-run driver, on the other hand, is a complete unknown—a "phantom." You have no name, no license plate, and no one to sue. This is exactly where Uninsured Motorist (UM) coverage becomes your lifeline.

Without it, your only option for covering medical bills is often your own health insurance, leaving you to pay deductibles and co-pays out of your own pocket. Your UM policy is designed to step into the shoes of that phantom driver’s missing insurance policy.

In the eyes of Georgia law, an unidentified driver who flees the scene is treated the same as an uninsured one. This legal shortcut is what allows your own insurance policy to cover your damages, so you aren't left holding the bag just because the at-fault driver disappeared.

Using a "John Doe" Lawsuit to Unlock Your UM Benefits

To actually get your UM benefits after a hit-and-run in Georgia, you can't just send your insurer a bill. You first have to legally establish that the unknown driver was at fault. This is done through a special legal action called a "John Doe" lawsuit.

You aren't suing a real person. Instead, you're filing a lawsuit against the placeholder "John Doe," who represents the phantom driver. This formal process serves a few key purposes:

- It officially establishes that an unknown person caused the accident.

- It allows you to legally "serve" your own insurance company with the lawsuit.

- It forces your insurer to step in and act as the defendant on behalf of the phantom driver.

By filing a John Doe suit, you create the legal foundation required to make a formal claim against your UM policy. It’s a necessary step to prove your case and show that since the at-fault driver can't be found, your own insurance must respond. Understanding this process is the first step toward getting the compensation you deserve.

Meeting Georgia's Rules for a Hit and Run UM Claim

Just telling your insurance company you were the victim of a hit-and-run isn't enough to get your claim approved. Georgia law has specific rules designed to prevent fraud, and you have to play by them to access your Uninsured Motorist (UM) coverage.

This means you need to provide concrete proof that the accident actually happened the way you say it did. It all comes down to one requirement.

The Corroboration Rule: Proving Your Claim

Georgia’s legal standard for these cases is known as the “corroboration rule.” In simple terms, this rule says your word alone isn't enough. Your story must be backed up by independent evidence.

You have to provide one of two things to satisfy this rule:

- An Independent Eyewitness: This is someone who saw the collision, was not a passenger in your car, and can confirm that an unknown vehicle hit you and fled. Their impartial testimony is incredibly powerful.

- Physical Evidence of Contact: If you don't have a witness, you must show tangible proof that another car struck yours. This could be paint transfer from the phantom vehicle, a broken piece of their car left behind, or damage to your car that an expert can confirm was caused by a collision.

Meeting one of these conditions is non-negotiable. Without it, your insurance company has every right to deny your UM claim.

The Two Most Important Steps You Must Take

Beyond gathering evidence, your immediate actions after the crash are just as important. There are two procedural steps you absolutely cannot skip.

First, file a police report immediately. Don't wait. Delaying can put your entire claim in jeopardy. An official police report creates the formal record of the incident that your insurer will demand. You can typically request a copy of your report through the Georgia Bureau of Investigation's online portal, which is a very helpful resource.

Here's what the Georgia portal for requesting an accident report looks like:

This official report is the foundation of your claim.

Second, you must notify your own insurance company promptly. Your policy has its own strict reporting timeline, often just a few days. While you generally have two years to file a lawsuit, failing to report the crash to your insurer on their timeline can result in an automatic denial based on their policy terms. To learn more about these legal deadlines, see our guide on the statute of limitations for personal injury in GA.

Even in what seems like a textbook hit-and-run, insurance companies will look for any reason to deny a claim. Failing to meet their procedural requirements—like reporting within 24-72 hours and cooperating with their investigation—is one of the most common reasons claims are rejected. You can find more information about these industry standards from the National Association of Insurance Commissioners.

What to Do Immediately After a Hit and Run

The moments after a hit-and-run crash are pure chaos. Your head is spinning, and it’s easy to feel disoriented and overwhelmed. But what you do in these first few minutes is especially important when it comes to answering the big question: does uninsured motorist cover hit and run?

Your absolute first priority is safety. If you can, get your car over to the shoulder and out of the flow of traffic. Before you do anything else, check on yourself and your passengers for any injuries.

Your Immediate Action Plan

Once you're in a safe spot, it's time to switch gears and start gathering the evidence that will become the backbone of your claim. The key is to stay as calm and methodical as possible. Every small detail you can lock down is a win.

It's tough to think clearly when you're shaken up, so just focus on these four essential steps:

- Call 911 Immediately: This is non-negotiable and the single most important thing you can do. A police officer will respond to the scene to create an official accident report, which your insurance company will absolutely require.

- Document Everything You Remember: While you wait for help, pull out your phone and either type or record a voice memo of every single detail you recall about the other car. What was the make, model, or color? Did you catch even a piece of the license plate?

- Look for Witnesses: Scan the area. Are there other drivers who pulled over? Pedestrians on the sidewalk? Do any nearby businesses have security cameras pointed toward the road? If you find anyone who saw what happened, get their name and phone number.

- Take Photos of Everything: Use your phone to document the scene from every possible angle. Get shots of the damage to your car, any visible injuries you have, the general area, and even debris left behind from the other vehicle, like a busted taillight.

When a driver flees the scene, building a case falls on your shoulders. Advanced tools like Car Security Systems with GPS tracking can sometimes provide invaluable data, but for most people, it comes down to old-fashioned evidence gathering.

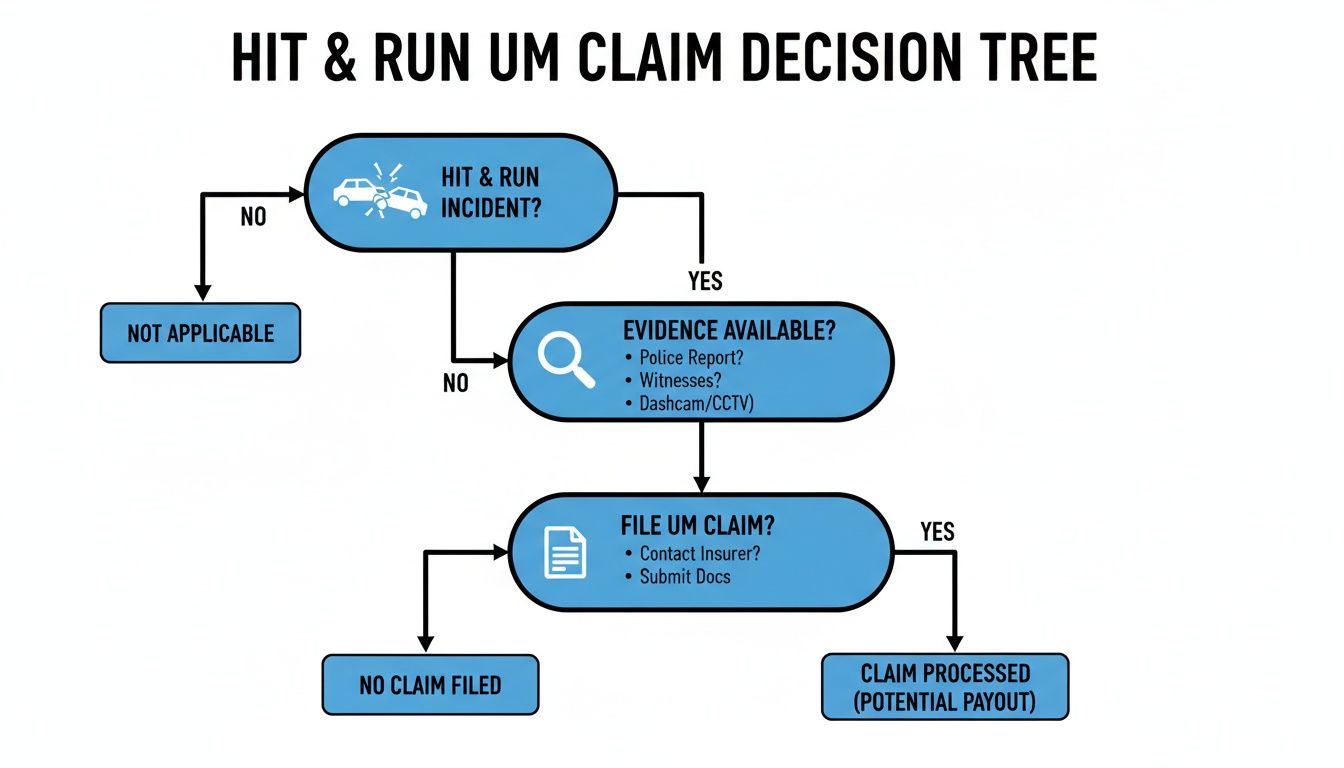

This decision tree gives you a visual guide to the key steps involved in figuring out if you can file a UM claim.

As the flowchart shows, a successful claim is built on having enough evidence and following the right procedures with both the police and your insurer. Each step you take methodically strengthens your position, making it much harder for an insurance company to push back or deny your claim. The proof you gather at the scene is what ultimately shows that uninsured motorist does cover a hit and run.

How to File Your UM Claim and What to Expect

Once you’ve dealt with the immediate aftermath of the crash, your next move is to get the Uninsured Motorist (UM) claim process started. This begins by formally notifying your own insurance company that the hit-and-run happened.

You’ll need to hand over all the evidence you managed to gather at the scene. The official police report number is especially important—think of it as the foundation of your entire claim.

It’s helpful to remember that even though this is your insurance company, the one you faithfully pay every month, your goals are not aligned. Their primary objective is to protect their profits, which often means paying out as little as possible.

The Adjuster and the Investigation

After you file the claim, your insurer will assign an adjuster to the case. This person’s job is to dig into the details of the incident and figure out what your claim is worth—if anything.

The adjuster will go through every piece of information you provide with a fine-tooth comb, including:

- The official police report.

- Statements from any witnesses.

- Photos you took of the accident scene and the damage to your car.

- All medical records related to the injuries you sustained.

Honestly, this process can feel like you’re fighting an uphill battle. The adjuster is on the lookout for any inconsistencies in your story and needs solid proof that the hit-and-run directly caused your injuries and property damage.

Brace yourself for intense scrutiny from the adjuster. They might question how severe your injuries really are or challenge the necessity of your medical treatments. Their goal is simple: verify the claim and calculate its lowest possible dollar value.

What to Say and What to Avoid

When you talk to the adjuster, just stick to the facts. Give them clear, truthful answers, but don’t offer up extra information or guess about things you’re not 100% sure of. Never admit fault or try to downplay your injuries. A seemingly harmless comment like, "I'm just a little sore," can be twisted later to argue your injuries weren't that serious.

Keeping meticulous records is non-negotiable. Maintain a file with all your medical bills, receipts for any out-of-pocket costs, and documentation of missed work to prove lost wages. When you have a clean, organized paper trail, it becomes much harder for an adjuster to poke holes in your claim. For a more detailed guide, you can learn more about how to file a car accident claim in Atlanta.

Ultimately, the objective is to build a well-documented case that leaves no doubt that uninsured motorist does cover a hit and run and fully justifies the compensation you’re asking for.

Why Uninsured Motorist Coverage Is So Important

Some drivers might be tempted to skip Uninsured Motorist (UM) coverage, thinking it’s an easy way to trim a few dollars off their premium. But when you look at the real-world numbers, you quickly realize just how massive that gamble is.

The hard truth is that a shocking number of drivers are on the road without any insurance at all. This isn't some rare, unlucky event; it's a common problem that puts every single responsible driver in Georgia at serious financial risk.

The Real-World Risk on Georgia's Roads

The odds of crossing paths with an uninsured driver are far higher than most people imagine. The Insurance Research Council recently estimated that about one in every seven drivers on U.S. roads was uninsured in 2023.

Think about what that means. With roughly 255 million licensed drivers in the country, there could be as many as 39 million uninsured drivers out there at any given moment. That creates a massive pool of potential accidents where your UM coverage is the only thing standing between you and financial disaster. You can read more about these uninsured driver statistics to see the full scope of the problem.

This risk is only made worse by the sheer number of hit-and-run accidents.

In 2022 alone, there were approximately 859,000 hit-and-run crashes reported in the U.S. These incidents resulted in nearly 3,000 fatalities, highlighting just how dangerous these irresponsible drivers are.

When you combine the high number of uninsured drivers with the thousands of hit-and-runs that happen every year, the value of UM coverage becomes undeniable. It’s not just an optional add-on; it’s an essential layer of financial protection for you and your family.

Consider it an investment in your peace of mind. It ensures you have a reliable way to cover your medical bills and lost wages when the person at fault simply vanishes. This is precisely why it's so important to understand that, yes, uninsured motorist does cover hit and run situations.

Frequently Asked Questions About Georgia Hit and Run Claims

We get a lot of questions about the finer points of Uninsured Motorist (UM) coverage after a hit-and-run. Let's tackle some of the most common ones we hear from our Atlanta clients.

What Happens If the Hit and Run Driver Is Found Later?

This is a great question. If law enforcement actually manages to track down the at-fault driver after you’ve already started your UM claim, the process simply pivots. Your own insurance company will then go after the other driver’s insurance (if they have any) or sue them directly to get back the money they paid you.

This is a legal process called subrogation. For the most part, it happens behind the scenes and you won’t have to do much. However, your policy does require you to cooperate if your insurer asks for your help.

Does UM Coverage Pay for My Car Repairs?

It depends entirely on the specific UM coverage you purchased. In Georgia, Uninsured Motorist coverage is split into two distinct parts:

- UM Bodily Injury (UMBI): This is the part that covers your medical bills, lost income, and pain and suffering.

- UM Property Damage (UMPD): This is optional coverage specifically for repairing or replacing your vehicle.

If you already have Collision coverage on your policy, that will be your primary way to get your car fixed, minus your deductible. But if you also carry UMPD, you can use that to cover the damage, and it often comes with a lower deductible than Collision. It's a choice you make when you buy your policy.

How Long Do I Have to File a Hit and Run Claim?

This is where things can be a bit confusing, because there are two different deadlines you have to worry about.

For a personal injury lawsuit, Georgia’s statute of limitations is generally two years from the date of the accident. But your own insurance policy has much, much shorter deadlines for simply reporting the accident. Most policies require you to notify them "promptly" or "as soon as practicable"—which really means right away. Don't wait.

For more helpful guides and legal information, feel free to explore our free resources section. Understanding these rules is absolutely essential for protecting your rights, especially when you're trying to confirm whether uninsured motorist does cover a hit and run.