When you see “bodily injury liability coverage” on your auto insurance policy, what does it actually mean? As an Atlanta personal injury attorney, I can tell you it’s your primary financial shield. It’s the part of your car insurance that protects you if you cause an accident that injures another person. It's designed to pay for their medical bills, lost wages, and even their pain and suffering. Understanding what is bodily injury liability coverage is the first step to making sure you and your assets are properly protected.

Understanding Your Financial Shield After a Crash

Bodily injury liability coverage is truly the backbone of any car insurance policy. Its job is to cover the costs when you are legally responsible—or "at fault"—for injuring someone else in an accident. Without it, your personal assets, like your home and savings, could be at risk in a lawsuit.

It's important to understand this coverage is for others, not for you. That’s a common point of confusion. If you get hurt, other parts of your policy (or the at-fault driver's policy) would apply. This coverage kicks in to pay for the harm done to other drivers, their passengers, or even a pedestrian you hit.

In fact, carrying this insurance isn't just a good idea—it's the law in nearly every state, including Georgia. State authorities like the Georgia Department of Driver Services set the minimum requirements. Driving without it leaves you personally exposed to what could be staggering medical and legal costs.

What Does Bodily Injury Liability Pay For?

So, when you're at fault, what specific costs does this coverage handle for the injured party? It pays for a range of damages, but only up to the limits you selected for your policy (we’ll dive into that next).

To give you a clearer picture, here’s a quick summary of what this coverage pays for when you are at fault in an accident.

Bodily Injury Liability At a Glance

| What It Covers for the Other Party | Real-World Example |

|---|---|

| Medical Expenses | Ambulance transport, ER visits, surgery, hospital stays, and ongoing physical therapy. |

| Lost Wages | If the injured driver is a contractor who can't work for two months, it covers their lost income. |

| Pain and Suffering | Compensation for the physical agony and emotional trauma resulting from the crash. |

| Legal Fees | If the person you injured files a lawsuit, your policy helps pay for your legal defense team. |

The core idea behind this coverage is financial responsibility. It ensures the people you accidentally harmed get the financial support they need to recover, all while protecting you from financial ruin.

Grasping the role of bodily injury liability insurance is the first, most important step toward ensuring you're properly protected every time you get behind the wheel.

Decoding Your Policy Limits: What the Numbers Mean

When you look at your car insurance declaration page, you’ll see a string of numbers that probably looks something like 25/50/25 or maybe 100/300/50. These aren't just random figures; they are the heart of your financial protection if you cause an accident.

These numbers are your policy limits—the absolute maximum dollar amount your insurance company will pay out when you are found at fault. They always appear in a sequence of three, and each number corresponds to a specific type of coverage.

Let’s break down exactly what each number in that sequence means, using a common Georgia minimum policy, $25,000/$50,000/$25,000, as our guide.

The First Number: Per-Person Limit

The very first number in the sequence sets the maximum amount your insurer will pay for the bodily injuries of a single person you hurt in a collision.

- Scenario: Let’s say your per-person limit is $25,000. You cause a crash, and the other driver ends up with $40,000 in medical bills. Your insurance will pay the first $25,000. That leaves you personally responsible for the remaining $15,000.

This limit applies to each individual person injured, which brings us to the second number.

The Second Number: Per-Accident Limit

The second number is the total cap your policy will pay for all bodily injuries combined in a single accident, no matter how many people are hurt.

This is a very important distinction. The per-accident limit is the total pot of money available for everyone's injuries, and it can never pay out more than the per-person limit to any one individual.

- Scenario: Your policy is 25/50/25. You cause a multi-car accident that injures three people.

- Person A has $30,000 in medical bills.

- Person B has $15,000 in medical bills.

- Person C has $10,000 in medical bills.

- Your insurance pays Person A up to their $25,000 per-person limit. They are still owed $5,000, which you’ll have to cover out-of-pocket.

- Person B receives their full $15,000, and Person C gets their full $10,000.

- The total payout is $25,000 + $15,000 + $10,000 = $50,000. This hits your per-accident limit exactly.

If the total medical bills had exceeded $50,000, you would be on the hook for every dollar above that cap. For more plain-English explanations of insurance terms, you might find our legal dictionary for personal injury cases helpful.

The Third Number: Property Damage

Finally, the third number represents the maximum your policy will pay for property damage you cause. This coverage is entirely separate from the bodily injury limits.

It’s designed to pay for things like:

- Repairing or replacing the other person's vehicle.

- Damage to public property, like a guardrail or telephone pole.

- Damage to a building, fence, or someone’s front yard.

If your property damage limit is $25,000 and you total a brand-new SUV valued at $50,000, your insurance pays the first $25,000. You are personally liable for the other $25,000. This is exactly why understanding these numbers—and seriously considering higher limits—is so important. Your policy limits are your primary defense against financial ruin after a crash.

What Bodily Injury Liability Does Not Cover

Understanding what your Bodily Injury liability coverage is for also means knowing what it isn't for. Think of it this way: BI coverage is designed to help the people you hurt in an accident you cause. It’s strictly for others. It does not and will not pay for your own injuries or vehicle damage.

Grasping these boundaries is very important. If you don’t, you could be facing a massive, unexpected financial hit after a wreck. Let's break down exactly what falls outside the scope of this coverage.

Your Own Injuries and Medical Bills

First and most importantly, your own Bodily Injury liability policy will never pay for your own medical expenses. If you are at fault for a crash and get hurt, you must look elsewhere to cover your hospital bills, physical therapy, and lost wages.

Your options for covering your own medical costs typically include:

- Medical Payments (MedPay) Coverage: This is an optional add-on to your policy that pays for medical treatment for you and your passengers, no matter who caused the accident.

- Your Personal Health Insurance: This will be a primary resource for your medical needs after you’ve been injured in a collision.

- The Other Driver's Policy: If the other driver was at fault, their Bodily Injury liability coverage is what kicks in to pay for your injuries.

So, if you run a red light and break your leg in the collision, your BI coverage is there to help the other driver. You'd have to rely on your own MedPay or health insurance to handle your broken leg.

Damage to Your Own Vehicle

Similarly, Bodily Injury liability has nothing to do with fixing your car. Its sole focus is on the "bodily injury" part of the equation—for other people.

If your car is damaged in an accident you caused, you need a different tool in your insurance toolbox. That tool is called collision coverage. Without collision coverage on your policy, you are on the hook for every penny of your own vehicle repairs. You can find more details on Georgia's auto insurance requirements from state resources like the Georgia Office of Commissioner of Insurance and Safety Fire.

Remember the key distinction: Liability coverage pays for damage you do to others. Collision and Comprehensive coverages pay for damage done to your vehicle.

Injuries to Family Members in Your Household

This is a detail that surprises many people. In almost all standard auto policies, you cannot make a Bodily Injury liability claim for injuries to a family member who lives with you. This is due to a common policy provision often called a "household exclusion" or "family member exclusion."

Insurers include this to prevent certain legal situations and potential fraud from intra-family lawsuits. If your spouse or child is hurt while riding as a passenger in an accident you cause, you'll need to turn to your MedPay coverage or their personal health insurance to pay their medical bills, not your BI liability. It's a key detail for understanding the true scope of your policy.

Why Georgia's Minimum Insurance Is Often Not Enough

In Georgia, every driver must legally carry car insurance. Meeting that bare minimum requirement keeps you compliant with the law, but it can create a dangerous—and false—sense of security. Relying solely on the state-mandated limits is a huge financial gamble. What’s legally required is rarely enough to protect you in a real-world crash.

The law, specifically O.C.G.A. § 33-7-11, mandates that drivers carry at least $25,000 per person and $50,000 per accident for bodily injury liability. Those numbers might seem substantial on paper, but they can be completely exhausted by even a moderately serious collision.

The Real Cost of an Injury

Let’s put those numbers into a practical context. Imagine you cause a wreck on I-285 in Atlanta. The other driver suffers a concussion and a broken arm—common injuries in a significant impact. Their immediate medical journey could look something like this:

- Ambulance and ER Visit: Easily $5,000 – $10,000

- Hospital Stay: A few nights of observation and care can quickly exceed $15,000

- Surgery and Follow-Up Care: Setting the broken bone could add another $10,000 – $20,000+

- Lost Wages: If they can't work for a month, that's thousands more in losses.

In this entirely realistic scenario, the medical bills alone will blow past your $25,000 per-person limit. Once your policy pays out that maximum, you are personally responsible for every dollar that remains. Your savings, your home, and even your future wages are now at risk.

The purpose of liability insurance isn't just to be legal; it's to protect your financial future. The state minimums were set years ago and have not kept pace with the dramatic rise in medical costs and legal awards.

And what if more than one person is hurt? Your $50,000 per-accident limit could be wiped out almost instantly, leaving multiple injured people with valid claims directly against your personal assets.

Rising Claims and Verdicts

The financial danger of carrying minimum coverage is magnified by the current trend of larger jury verdicts and higher claim settlements. Bodily injury claim costs are soaring, putting immense pressure on underinsured drivers.

Recent industry data reveals a sharp spike in claim severity and litigation that can financially ruin those without proper protection. As one example, a report from the Insurance Information Institute noted that the average bodily injury liability claim was already over $20,000 in 2020 and has only increased. This environment makes carrying higher limits not just a smart choice, but an essential one.

For drivers in dense urban areas like metro Atlanta, the risk is even greater. More cars, constant congestion, and high speeds create a recipe for serious collisions with significant injuries. Robust bodily injury liability coverage isn't a luxury; it's a fundamental part of responsible car ownership. Protecting your assets means looking beyond the bare minimum and choosing limits that reflect the real-world costs of an accident today.

How a Bodily Injury Claim Works After an Accident

If you get hurt in a wreck someone else caused, their bodily injury liability coverage is supposed to pay for your damages. But how does that money actually get from their insurance company to you? The process isn't instant; it's a journey that starts at the crash scene and follows a series of distinct steps.

First things first: seek immediate medical care. Always. Even if you think you’re okay, some injuries don't show up for hours or days. Getting checked out by a doctor right away creates a vital medical record that ties your injuries directly to the accident. At the same time, call 911 to get police on the scene so an official report is filed.

Notifying the Insurance Company and Starting the Investigation

Once you've taken care of your health, the next step is to notify the at-fault driver's insurance company that you're filing a claim. This is what kicks off their internal process. The insurer will assign an insurance adjuster to your case. It’s important to remember the adjuster's role: their job is to protect the insurance company's bottom line by closing your claim for the least amount of money possible.

The adjuster will launch an investigation to figure out who was at fault and how much your damages are worth. They will dig into several key pieces of evidence:

- The Official Police Report: This gives them an objective rundown of the crash, including the officer's initial thoughts on who was responsible.

- Your Medical Records: These documents are proof of your injuries, the treatments you've received, and the associated costs.

- Proof of Lost Income: Pay stubs or a letter from your employer will show how much work you missed and the wages you lost because of it.

- Witness Statements: The adjuster will likely reach out to anyone who saw the accident to get their version of events.

When you've suffered physical injuries, especially ones that need ongoing treatment like chiropractic care after a car accident, the adjuster will scrutinize every detail. For a deeper dive into the initial steps, you can check out our guide on how to file a car accident claim in Atlanta.

Dealing with the Adjuster and Settlement Offers

After looking over the evidence, the adjuster will make a settlement offer. Brace yourself, because the first offer is almost always a lowball. Adjusters use specific tactics to minimize what they pay, like questioning how serious your injuries really are or trying to argue you were partially at fault. They may also rush you to accept a quick payout before you even know the full extent of your medical needs.

A common strategy is to ask for a recorded statement early on. It's often best to politely decline this request until you have spoken with an attorney, as your words can be used to undervalue your claim later.

This back-and-forth is exactly why having a legal advocate is so important. An experienced personal injury attorney knows these tactics inside and out. We know how to build a strong case with solid evidence, handle all the communication with the insurer, and negotiate for a settlement that actually covers your medical bills, lost income, and pain and suffering.

The financial toll of a serious injury can be massive, and claim payouts are on the rise. According to the National Association of Insurance Commissioners (NAIC), the average cost per bodily injury liability claim has been steadily increasing, highlighting the growing financial risk of accidents. With costs climbing, the risk of being left with a pile of bills is very real.

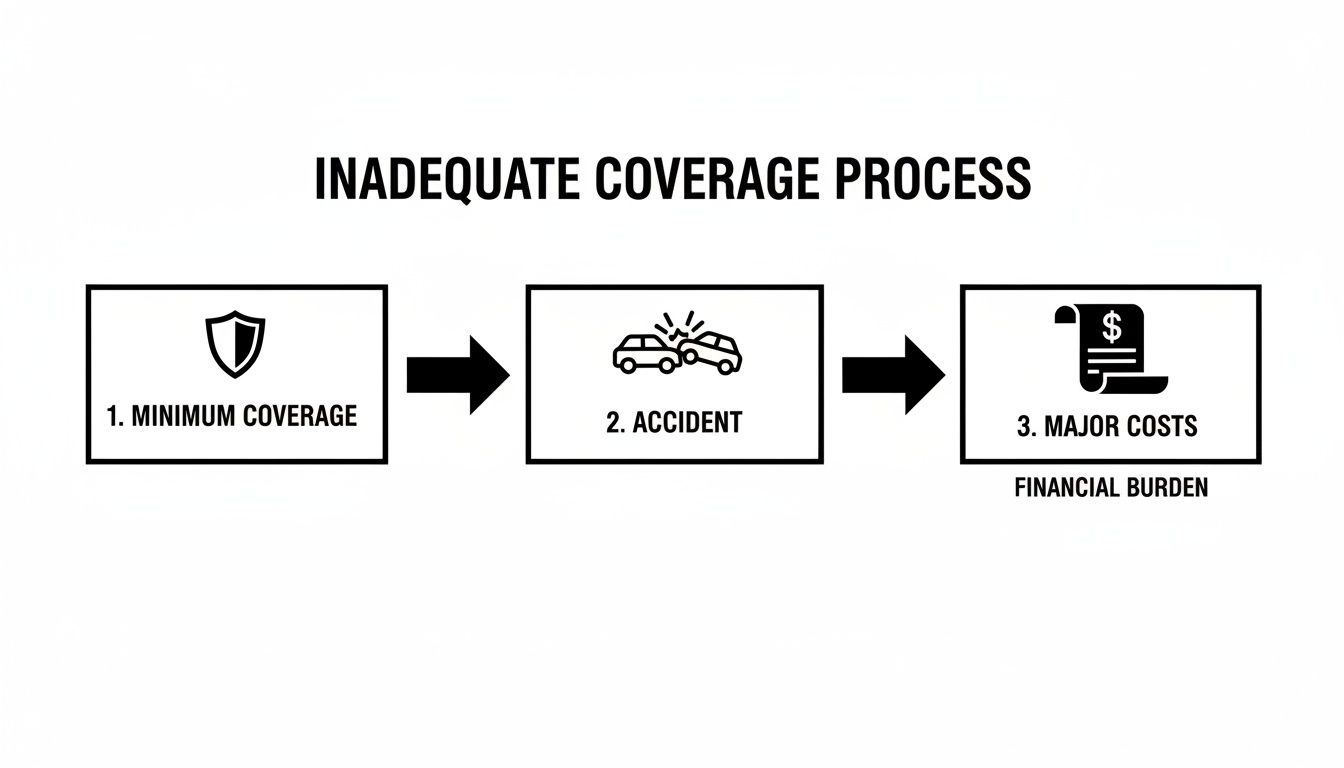

This flowchart shows just how dangerous it is to rely only on minimum coverage.

As you can see, what starts as legally compliant insurance can quickly become a financial disaster when faced with the true costs of a serious accident. Understanding the claim process and knowing when to get help are the keys to protecting your rights and getting the compensation you deserve.

When the Other Driver Has Little or No Insurance

You’ve done everything right. You bought a robust bodily injury liability policy to protect your assets if you ever cause an accident. But what happens when another driver hits you, and they either have no insurance at all or carry only the bare-bones state minimum?

It’s a frightening and all-too-common scenario on Georgia roads.

This is exactly where your own policy can come to the rescue, but only if you have the right kind of protection. We’re talking about Uninsured/Underinsured Motorist (UM/UIM) coverage. Think of it as your personal financial safety net, designed to step in and pay for your injuries when the at-fault driver simply can't.

The Role of Uninsured Motorist Coverage

Uninsured Motorist coverage is an optional but very important part of your own auto insurance policy. It effectively acts as a substitute for the bodily injury liability coverage the other driver should have had.

If a driver with no insurance hits you, your UM coverage can pay for:

- Your medical bills and any future medical care you need.

- Lost wages from being unable to work.

- Compensation for your pain and suffering.

Without it, you’d be left trying to sue an uninsured driver—a person who almost certainly has no assets to pay a judgment. Your only other option would be your health insurance, which won't cover lost income or pain and suffering.

Uninsured/Underinsured Motorist coverage lets you file a claim with your own insurance company. Your insurer then stands in the shoes of the at-fault driver's missing or inadequate insurance carrier.

What About Underinsured Motorist Coverage

The second part of this protection, Underinsured Motorist coverage, tackles a different but equally serious problem. This applies when the at-fault driver does have insurance, but their policy limits are too low to cover the full extent of your injuries.

For instance, let’s say your medical bills total $75,000, but the at-fault driver only has Georgia’s minimum $25,000 BI limit. Their insurance will pay out its $25,000 max. Your UIM coverage can then step in to cover the remaining $50,000, up to your own policy's limits. Situations like these highlight why understanding the car accident lawsuit process in Atlanta is so helpful.

Many drivers carry insufficient coverage simply because of cost. Bodily injury liability premiums vary widely across the country, as shown in reports by organizations like The Zebra. This economic pressure is a key reason so many drivers are underinsured.

Having UM/UIM coverage is a proactive step to protect yourself from the financial fallout of another driver's bad choices. It ensures your recovery isn't limited by someone else’s lack of insurance. When asking what is bodily injury liability coverage, it's just as vital to understand how to protect yourself when others don't have enough of it.

Common Questions About Bodily Injury Liability

We've covered a lot of ground on what bodily injury liability coverage is, but it’s completely normal to have a few more questions. Let's dig into some of the most common issues we hear about from drivers here in Atlanta to clear up any confusion.

Will My Rates Go Up If I File a Claim on Someone Else's Policy?

This is a widespread myth, and the answer is no. Filing a claim against another driver's insurance because they caused the wreck should not impact your premium.

Your own insurance rates are tied to claims made against your policy. Seeking the compensation you're owed from the at-fault driver's insurer is your legal right and doesn't count against you.

Does Bodily Injury Liability Pay for My Passengers?

Yes, in most cases. If you cause an accident, your bodily injury liability coverage is there to pay for injuries to people in the other vehicle and for passengers who were riding in your own car.

The main exception, as we mentioned earlier, is usually for family members who live with you. Standard policies often exclude them. For their injuries, you would typically turn to your Medical Payments (MedPay) coverage instead.

What Should I Do if the Other Driver's Insurance Company Calls Me?

Proceed with caution. The other driver’s insurance adjuster is not on your side—their job is to protect their company's bottom line by minimizing what they have to pay out.

You can provide basic, factual information, but you should never give a recorded statement or accept a quick settlement offer. You need time to understand the full extent of your injuries and your legal rights first. Remember, any delay can be costly, so it's a good idea to know the Georgia statute of limitations for personal injury claims.

Understanding these details helps you feel more prepared and confident after a crash. Hopefully, these answers reinforce the key takeaways from our guide and give you a clearer picture of what bodily injury liability really means for you.

If you've been injured in an accident and are getting the runaround from an insurance company, you don't have to face them alone. The team at Jamie Ballard Law is here to help you understand your rights and fight for the compensation you deserve. Contact us for a free, no-obligation case evaluation at https://jamieballardlaw.com.