When an insurance company offers you a quick settlement after an accident, it always comes with a document called a release of claim. It is so important you understand what this document is: a legally binding contract that permanently ends your right to seek any further compensation for your injuries. A release of claim is a serious legal tool, and signing one without fully understanding it can have lasting consequences on your financial well-being.

Understanding What a Release of Claim Really Means

Think of a release of claim as the final word on your injury case. The moment you sign it and cash that settlement check, you give up all rights to pursue additional money from the at-fault party for that specific incident.

This isn't just about the medical bills on your desk today. It covers absolutely everything, including:

- Future medical care, surgeries, or physical therapy that may become necessary.

- Wages you lose down the line because your injuries prevent you from working.

- Any ongoing or future pain and suffering.

Signing a release is like closing and locking a door forever. You cannot reopen it later if you find out your injuries are more severe than you first believed or if unexpected medical costs surface months or even years later. The insurer is paying you a one-time sum to close its file on you for good.

The Finality of the Agreement

The language in these releases is deliberately broad. Insurers often include phrases stating you release the at-fault party from all claims, "known and unknown." That single phrase is incredibly powerful—it means you are signing away your right to compensation for injuries you don’t even know you have yet.

For example, a back injury that feels like a minor strain today could require major surgery in a year. If you've already signed a release, you are on your own for those medical bills. The settlement you accepted is the only money you will ever see for that accident. A firm grasp of understanding general legal terms is a big help before engaging with such a document.

Here is a look at a Georgia statute that outlines the very right you give up when you sign a release.

This code section establishes your legal right to pursue damages when someone harms you—the exact right a release of claim permanently terminates.

The fundamental trade-off is simple, but the consequences can be life-altering. Here's a clear breakdown of what's happening.

What You Gain vs What You Forfeit When Signing a Release

| What You Receive (The Settlement) | What You Permanently Forfeit (Your Legal Rights) |

|---|---|

| Guaranteed, immediate payment for a fixed sum of money. | The right to sue the at-fault party for any and all damages related to the incident. |

| Certainty and finality, avoiding the time and stress of litigation. | The ability to seek compensation for future medical bills, even if your condition worsens unexpectedly. |

| No further need to negotiate or communicate with the insurance company about this incident. | The right to recover lost future wages or diminished earning capacity resulting from your injuries. |

| Closure on the financial aspect of the incident, allowing you to move forward. | The ability to make a claim for "unknown" injuries that may surface months or years later. |

| A definitive end to the claim process, with no risk of losing in court. | The right to seek damages for ongoing pain and suffering, emotional distress, or loss of quality of life that continues after the settlement. |

This table illustrates the core exchange: you get a check now, but you give up every right to seek more money later, no matter what happens.

The core purpose of a release is to provide absolute certainty for the insurer. They pay a fixed amount, and in exchange, their financial and legal obligation to you is completely and permanently finished.

Because this language can be dense, you can find helpful, plain-English definitions in our firm's legal dictionary. Before signing, you must be certain the settlement amount fully covers every single loss—past, present, and future. Signing this document without a full grasp of its implications could put your financial future at risk.

The Different Types of Release Forms You May Encounter

When you’re dealing with the aftermath of an accident, you need to understand that not all settlement documents are the same. The specific type of release of claim an insurance adjuster hands you can make or break your ability to get fair compensation. Here in Atlanta, you'll generally run into two main types, and knowing the difference is essential for protecting your rights.

Make no mistake, the document an insurer presents is designed to benefit them by closing out their financial responsibility as quickly and completely as possible. The sheer scale of insurance payouts shows why these releases are so vital to their business. For instance, one global review of over 530,000 insurance claims revealed that insurers paid out an average of more than €48 million every single day to cover losses. You can dig deeper into these extensive claim reviews from Allianz, which detail how releases are used to manage massive liabilities from corporate disputes to natural disasters.

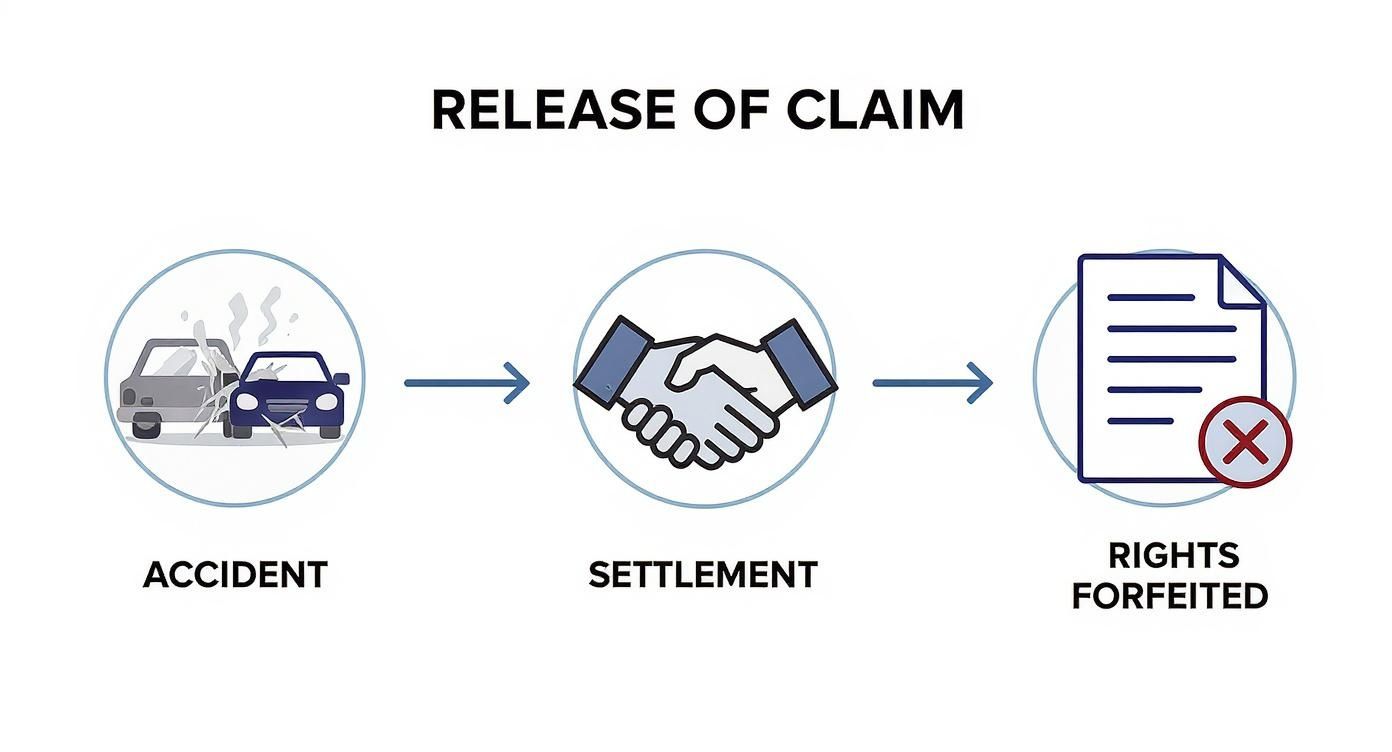

This visual breaks down the typical path from an accident to a settlement, showing how signing a release means you give up any future rights.

The key takeaway here is simple: the settlement handshake is the final step. Once that document is signed, the door to any further claims is permanently locked.

The General Release: A Total and Final Agreement

The most common form you'll see is a General Release. Think of it as a master key that permanently locks every single door related to your claim. When you sign a General Release, you are giving up your right to sue anyone connected to the accident for any reason—both now and forever.

This includes claims against:

- The at-fault driver or property owner.

- Their insurance company.

- Any other party who might share some of the blame.

- Even claims for injuries you don't even know you have yet.

The language is intentionally broad, often stating you release all "known and unknown" claims. This means if you develop a serious medical condition a year later that’s directly tied to the accident, you have no legal path to seek more money. A General Release provides absolute finality, which is exactly what the insurance company is after.

The Limited Release: A Strategic Georgia Option

Fortunately, Georgia law provides a powerful alternative in certain situations: the Limited Release. Unlike the all-encompassing General Release, this document is far more specific. It's like a key that only locks one specific door while leaving others open for you.

Under Georgia law (O.C.G.A. § 33-24-41.1), a Limited Release allows you to accept a settlement from one insurance policy while preserving your right to pursue claims against other available policies.

This is incredibly useful in cases with multiple at-fault parties or when the at-fault driver's insurance just isn't enough to cover all your damages.

Let’s look at a practical example. Imagine you're in a car wreck caused by a driver with a $25,000 liability policy, but your medical bills alone are $50,000. If you have Underinsured Motorist (UM) coverage on your own policy, a Limited Release lets you take the at-fault driver’s $25,000 policy limit while keeping your right to file a claim with your own insurance company for the rest.

Had you signed a General Release in that scenario, you would have been barred from accessing your own UM coverage, leaving you stuck with significant unpaid medical debt.

Understanding which type of release of claim is right for your situation is a massive part of ensuring you are treated fairly after an accident.

Hidden Dangers Within a Standard Release Document

When an insurance adjuster tables a settlement offer, it’s always tied to their standard release of claim form. It's important to remember this document was drafted by their lawyers to serve their interests, not yours. It’s engineered to give the insurance company maximum protection, often at your expense, by using dense legal language that hides serious risks.

Don't think of it as just a receipt for payment. You need to see this document for what it is: a tool to permanently end their financial responsibility. They aren't just paying your current medical bills; they are buying your silence and signature on a contract that shields them from all future obligations tied to your accident. This is exactly why a methodical, clause-by-clause review is a very good idea.

Unpacking the "Known and Unknown" Claims Clause

Look for a phrase that releases all claims, "both known and unknown." These few words carry enormous weight. When you sign, you aren't just settling the claim for the injuries you know about today. You're also giving up your right to seek compensation for any related injuries that might surface weeks, months, or even years from now.

Imagine you settled a car wreck claim for what you thought was a minor back strain. Six months later, you find out you have a herniated disc requiring surgery and extensive physical therapy. Because you released all "unknown" claims, you are legally blocked from going back to the at-fault party for another dime. That massive financial burden is now yours alone.

The Indemnification Clause Explained

Another huge red flag is an indemnification clause, which you might also see called a "hold harmless" clause. This is a particularly tricky bit of legal wording. In plain English, it means that if someone else—like your health insurance company, a hospital, or even Medicare—comes after the at-fault party's insurer for money they paid for your care, you agree to pay the insurer back.

Let that sink in. You could be legally forced to use your settlement money to reimburse the very company that paid you. Here’s how it plays out:

- You sign a release with an indemnification clause.

- Your health insurer, who covered your ER visit, later files a lien to get its money back from the at-fault driver's insurance.

- Because of the clause you signed, that insurer can now turn around and demand you pay them whatever they had to pay your health insurer.

This clause can turn your settlement into a debt overnight, leaving you with nothing. While the concept of indemnification is a normal legal tool, in a personal injury release, it is almost always used against the injured person.

The Confidentiality Clause and Its Impact

Many release forms also contain a confidentiality clause, which functions as a non-disclosure agreement (NDA). This provision legally stops you from discussing the amount or even the existence of your settlement with nearly anyone. It may seem harmless, but it only serves the insurance company by keeping their payout numbers secret.

By signing a confidentiality clause, you may be barred from talking about your experience with family, friends, or even in a support group. Violating the agreement can lead to serious legal and financial penalties, including being forced to return the entire settlement amount.

You probably don't plan on shouting your settlement details from the rooftops, but this clause strips you of the right to share your own story. Insurers use these clauses to prevent other accident victims from finding out what similar cases are worth, giving them a major upper hand in the next negotiation.

These hidden clauses are precisely why you should never sign an insurance company's document without a thorough legal review. Every term is there for a reason—to protect them. Understanding what you’re truly giving up is the only way to protect yourself.

Why You Should Not Sign a Release Without Legal Advice

https://www.youtube.com/embed/1ibvx2qypg0

The moment you put your signature on a release of claim, your personal injury case is over—permanently. There are no do-overs, no second chances, and no going back if you realize later that you made a mistake.

An insurance adjuster's primary job is to protect their company's bottom line, which means settling your claim for the lowest possible amount. They are trained negotiators who handle these documents every single day.

Signing a release without a thorough legal review is one of the biggest financial risks you can take after an accident. The adjuster might seem friendly and helpful, but their goal is fundamentally opposed to yours. They want to close your case for pennies on the dollar, while you need to ensure your financial stability for the months and years to come.

Accepting Far Less Than Your Claim Is Worth

One of the most common pitfalls is accepting a settlement that seems fair at first glance but is actually just a fraction of what your claim is truly worth. Most people simply don't have the experience to accurately calculate the full, long-term cost of an injury.

A fair settlement has to cover far more than just your current medical bills. A comprehensive valuation must include:

- Future Medical Needs: This could involve surgeries, physical therapy, prescription medications, or specialized medical equipment you might need years down the road.

- Lost Earning Capacity: If your injuries prevent you from returning to your old job or limit your ability to work, you deserve compensation for that lost future income.

- Long-Term Suffering: This accounts for the ongoing physical pain, emotional distress, and loss of quality of life that stem from the accident.

An adjuster's quick offer will almost never account for these future damages. They are betting you don’t know how to calculate them, and by accepting their lowball offer, you could be left with enormous financial burdens later.

A quick settlement is rarely a fair settlement. The insurance company's first offer is a starting point for negotiation, not the final word. It's an invitation to settle for less before you understand the full value of your claim.

Releasing the Wrong Parties from Liability

Release forms are often packed with dense legal language that can be incredibly difficult to follow. A common danger is unintentionally releasing the wrong individuals or companies from liability. A standard "general release" is written as broadly as possible to protect not just the at-fault party but also their insurers, affiliates, and anyone else even remotely connected to the incident.

For example, you might think you are only releasing the driver who hit you. But the document you sign could also release the company that employed the driver, the manufacturer of a faulty car part, or even the government entity responsible for a poorly maintained road. By signing, you could give up your right to pursue other liable parties who share responsibility for your injuries.

Overlooking Medical Liens on Your Settlement

Another serious risk is failing to understand medical liens. If your health insurance, Medicare, or Medicaid paid for your medical treatment after the accident, they often have a legal right to be reimbursed from your settlement funds. This is called a lien or a right of subrogation.

If you sign a release and accept a settlement without addressing these liens, you could find yourself in a terrible spot. You are still legally obligated to pay back your health insurer, and you may have to do so out of your own pocket if the settlement funds are already spent. An experienced attorney knows how to identify these liens and negotiate with the insurance companies to reduce the amount you have to pay back, making sure more of the settlement money stays with you.

Before committing to a release, it's a good idea to seek legal advice, especially when understanding why an insurance company might refuse to pay a claim and what options are available. Having an attorney review your release of claim is a small step that provides massive protection for your future. If you have been offered a settlement and need someone to review the documents, we are here to help. You can easily schedule a free, no-obligation consultation with our team to discuss your case.

Georgia Laws That Affect Your Settlement Release

When you’re dealing with a personal injury claim in Atlanta, you’re not just up against the insurance company’s internal playbook. Georgia has specific state laws that directly impact any release of claim you sign. These laws can be your shield or your Achilles' heel, depending on how well you understand them.

These statutes govern everything from your deadline to file a lawsuit to how medical liens get paid from your settlement. Make no mistake: the insurance adjuster on the other end of the line knows these rules inside and out. They may use your lack of knowledge to push you into a quick, lowball settlement before you realize the full extent of your rights.

The Statute of Limitations Pressure

One of the biggest factors looming over any Georgia injury claim is the statute of limitations. Think of it as a legal countdown timer for filing a lawsuit.

Under Georgia law (O.C.G.A. § 9-3-33), you typically have just two years from the date of your injury to file. Miss that deadline by even one day, and your right to seek compensation in court is gone forever.

Adjusters are acutely aware of this ticking clock. They often use it as leverage, sometimes dragging their feet and then making a lowball offer as your deadline approaches. They know you're running out of time and might feel pressured to take whatever you can get. For a deeper dive into this deadline, you can read our guide on the statute of limitations for personal injury in Georgia.

Georgia's Limited Release Statute

We mentioned this earlier, but it’s a Georgia-specific rule so important it’s worth a second look. The Limited Liability Release statute (O.C.G.A. § 33-24-41.1) is a powerful tool for accident victims.

This law allows you to accept a settlement for the at-fault party's insurance policy limits without giving up your right to pursue other sources of compensation. This is incredibly valuable in cases such as:

- Crashes involving multiple at-fault drivers.

- Accidents where the at-fault driver was underinsured, and you have your own Underinsured Motorist (UM) coverage.

Using a Limited Release is a strategic move that can dramatically increase your total financial recovery. An adjuster, however, will almost always offer you a General Release first, hoping you don’t know you have a better option.

How Medical Liens Affect Your Settlement

If your health insurance, Medicare, or a hospital paid for your medical care after the accident, they often have a right to be paid back from your settlement. This is done through a lien.

A lien is a legal claim against your settlement funds. It acts like a debt that must be paid before you can receive your final share of the money.

If these liens aren't handled correctly, they can eat up a huge chunk of your settlement, leaving you with far less than you expected. An experienced attorney knows how to negotiate with lienholders to reduce the amount you owe, which means more of the settlement money stays where it belongs: with you. This is a key step that many people handling their own claims overlook.

The proper use of a release of claim is a cornerstone of how the insurance industry operates. For example, in the first half of one recent year, global insured losses from natural disasters reached $100 billion, and more than 90% of those were in the U.S. In those massive recovery efforts, releases are essential for efficiently distributing funds and closing claims. You can learn more about how insurance handles these major global events from the World Economic Forum.

Understanding how these state-specific laws interact with the document in front of you is the key to protecting your financial future. The finality of a release of claim makes it so important to get every detail right the first time.

Steps to Take Before You Sign Any Insurance Document

After an accident, the insurance adjuster might sound like your best friend, but their job is simple: settle your claim for the lowest amount possible. A key part of their strategy is often pressuring you to sign a release of claim before you’ve had a chance to think.

It’s important to remember you have the right to take your time. This decision protects your future, not their company's bottom line.

Feeling overwhelmed is completely normal. But rushing this step is a mistake that can leave you with a settlement that doesn't even begin to cover your long-term needs. Before you even think about putting pen to paper, you need to slow down and follow a careful, deliberate process.

Your Pre-Signing Checklist

Think of this as a methodical checklist. Each step is designed to bring you clarity and put you back in control of your case's outcome.

- Confirm You’ve Reached MMI: Do not sign a single thing until your doctor says you have reached Maximum Medical Improvement (MMI). MMI means your medical condition has stabilized, giving you a clear picture of any long-term limitations or future medical costs.

- Gather All Your Documents: Pull together every single medical bill, pharmacy receipt, and piece of paper proving your lost wages. You can't know if a settlement offer is fair without a complete financial picture of your losses.

- Request the Release in Writing: Always, always demand a full copy of the proposed release. Never agree to terms over the phone. You need to see the exact legal language they expect you to sign.

- Decline a Recorded Statement: Politely but firmly refuse to give a recorded statement to the at-fault party's insurance company. They are experts at using these recordings to find tiny inconsistencies in your story and weaken your claim.

Taking Control of the Conversation

When the adjuster calls with an offer, it’s easy to feel caught off guard. You can take back control with a simple, prepared response.

You can say, "Thank you for that information. I am not ready to make any decisions right now. I will need time to review everything thoroughly."

This polite refusal buys you the breathing room you need to think clearly without shutting down negotiations.

Ultimately, the single most important step is to have an experienced attorney review the document. A lawyer will immediately spot the hidden clauses and traps designed to limit your rights. This is a standard part of learning how to file a car accident claim in Atlanta and protecting yourself. By following these steps, you ensure you are making a fully informed decision before signing away your rights with a release of claim.

Common Questions About Release of Claim Forms

When a settlement offer finally lands on your table, a lot of questions pop up. That release of claim document can look intimidating and incredibly final. Here in our Atlanta office, we see the same worries and hear the same questions from people just like you.

Let's cut through the legalese and get you some straightforward answers. Understanding these key points is the first step in protecting your rights and making a smart decision for your future.

Can I Cancel a Release After I Sign It?

This is the number one question we get, and the answer is almost always no. A release of claim isn't just a piece of paper; it's a legally binding contract. Once your signature is on that line and the check is cashed, the deal is done. It’s considered final and irreversible.

In extremely rare situations, a contract might be voided for something like outright fraud, but proving that is a massive legal battle. You should always, always operate as if your signature is permanent. This is exactly why you need an attorney to review the document before you sign. It’s your one and only shot to get the terms right.

What Happens If I Discover New Injuries Later?

Unfortunately, if you signed a standard general release, you’ve waived your right to seek more money for injuries that show up later. These documents are written very carefully to include language that releases all claims, "known and unknown."

The insurance company is paying you for one thing above all else: finality. That clause protects them from having to reopen a case if a sore back turns into a herniated disc that needs surgery months down the road. This is precisely why it's so important to wait until you have reached Maximum Medical Improvement (MMI) before you even think about settling. As the Social Security Administration also emphasizes strong identity proofing and other careful processes, it highlights just how important it is to get all details exactly right in official matters.

Do I Have to Sign the First Release Sent to Me?

Absolutely not. The first settlement offer and the release form that comes with it are just that—an offer. Think of it as the opening bid in a negotiation, not the final word. You have every right to reject the offer and push back on the terms in that document.

You can and should negotiate for a settlement that actually covers all your damages, from medical bills and lost wages to your pain and suffering. Signing the first release of claim an insurer sends you without a lawyer's review is one of the biggest mistakes a person can make after an accident.

If an insurance company has sent you a release form, don't sign it alone. At Jamie Ballard Law, we offer a free, no-pressure review of your settlement documents to ensure your rights are protected. Contact us today to get the clarity you need. https://jamieballardlaw.com