When you're trying to resolve a claim, you'll almost always be asked to sign a document. So, what is a release of liability form? In the simplest terms, it's a legal contract where you agree to give up your right to sue someone over an injury. In return, you typically get something of value—usually, a settlement check.

Think of it as the final, legally binding handshake that closes the door on your claim for good.

Breaking Down a Release of Liability

Let's use a common Atlanta scenario. Imagine you're in a wreck on I-285, and the at-fault driver's insurance company offers you a settlement. Before they cut that check, they'll insist you sign a release of liability. This document is their ironclad guarantee that once you cash that check, you can never come back asking for more money.

This holds true even if your injuries turn out to be far more serious than you initially realized.

The legal language can get thick, but the core idea is simple. The person or company responsible for your harm (the “releasee”) pays you an agreed-upon sum. In exchange, you (the “releasor”) agree to drop all current and future legal claims tied to that specific incident. For a closer look at terms like these, our legal dictionary is a great resource.

Key Parts of a Release of Liability Form

Here is a quick summary of the common elements you will find in a typical release of liability document.

| Element | What It Means for You |

|---|---|

| The Parties | Clearly identifies you (the releasor) and the at-fault party (the releasee). |

| The Incident | Specifies the exact date, location, and nature of the accident or event being settled. |

| The Payment | States the exact dollar amount of the settlement (the "consideration"). |

| The Release Language | This is the core of the document, where you formally give up your right to sue for any known or unknown injuries. |

| Governing Law | Names the state whose laws will interpret the agreement (usually Georgia). |

| Signatures | Your signature makes the contract legally binding and enforceable. |

Understanding these components is the first step in knowing exactly what you're agreeing to.

Where You Might See This Form

While they're a fixture in personal injury cases like car accidents and slip-and-falls, these forms pop up elsewhere, too. They are standard in many business transactions, such as employment terminations where a severance package is offered. You’ll also find them in workers' compensation settlements and commercial dispute resolutions. They give businesses a clean break and protection from future lawsuits.

The Core Purpose From the Insurer's Viewpoint

For an insurance company, the release is non-negotiable. It provides finality. Without your signature, they’d live with the constant risk of you reopening the claim months or even years down the road. By getting you to sign, they can close their file on your case for good, knowing their financial duty is done.

Key Takeaway: A release of liability form is a binding contract. Signing it means you are accepting a settlement as the full and final payment for your injuries, forever giving up your right to seek further compensation for that event.

This is precisely why you must fully understand every word of that document before your pen ever touches the paper. Your signature carries serious, permanent weight and directly impacts your ability to be made whole after an injury.

Common Scenarios for Liability Waivers in Georgia

You might be surprised how often you’ll run into a release of liability form, especially after an unexpected injury here in Georgia. They aren't just for extreme sports; they frequently appear when an insurance company wants to resolve a claim—fast. Knowing when to expect one is the first step in protecting your rights.

The most common situation is a car wreck. It doesn't matter if it's a major collision on I-75 or a simple fender-bender in a quiet suburb; the script is usually the same. The at-fault driver's insurance adjuster will call you, often within days, with a settlement offer.

That offer might sound tempting, but it always comes with a catch: you have to sign their release form. The adjuster’s only goal is to close the file for the lowest amount possible before you fully understand the extent of your injuries and property damage. They’re betting you’ll take the quick money without realizing you're signing away your rights for good.

After a Slip and Fall Incident

Slip and fall incidents are another prime example. Let's say you slip on a spilled drink at a grocery store in Buckhead or trip over a broken paver at an outdoor shopping center. The business’s insurance provider will investigate and, more often than not, present you with a release.

Their motive is straightforward: avoid a lawsuit. By offering a small, upfront payment, they hope to eliminate their liability for your ongoing medical care, lost income, and the pain you've had to endure. That document is their legal shield against any future claims related to the hazardous condition that caused your fall.

Important Reminder: The party asking you to sign a release—whether it’s a massive insurance company or a local business—is protecting their bottom line, not your well-being. Their priority is to cap their financial exposure and end their legal responsibility.

Injuries From a Dog Bite

Liability waivers are also standard after an animal attack. If a neighbor's dog bites you at a local park, the owner’s homeowners insurance will typically get involved. An adjuster will reach out to settle your claim for medical bills and other immediate damages.

Just like with a car accident, this settlement is entirely dependent on you signing away any future right to sue. This is especially risky with dog bites, where injuries can lead to permanent scarring or infections requiring long-term treatment—costs a quick, lowball settlement will never cover.

Recognizing the Pattern in Personal Injury Claims

The pattern is the same across all these scenarios. You get hurt because of someone else's negligence, and their insurance company swoops in. The insurer offers you a check in exchange for your signature on a document that permanently absolves their client of all responsibility.

Here are a few other instances where you might be pressured to sign a release:

- Truck Accidents: After a crash with a commercial truck, the trucking company’s insurer will aggressively push for a release to shut down a potentially high-value claim.

- Defective Products: If a faulty product injures you, the manufacturer may offer a settlement tied to a release to head off a larger product liability lawsuit.

- Medical Malpractice: In some cases, a hospital or doctor’s insurance carrier may try to settle a claim early by using a release form.

Understanding what’s at stake in different types of personal injury claims is important. Recognizing what a release of liability form is—and why it’s being handed to you—is your best defense.

The Legal Strength of a Signed Release Form

When you put your signature on a release of liability form, it carries serious legal weight. In the eyes of the law, you're entering into a formal contract. Georgia courts operate on the assumption that an adult who signs a legal document has read it, understood it, and agreed to its terms. This is the core of enforceability.

An enforceable release acts as a powerful legal barrier. It effectively stops you from filing a lawsuit for any injuries covered in that agreement. Think of it like a locked door. Once you sign and accept the settlement money, that door closes on your right to seek any more compensation for that specific incident. For the insurance company, that finality is the whole point—it lets them close their file for good.

But that door isn't always bolted shut. The real strength of any release comes down to the specific language used in the document and the circumstances surrounding your signature. Its power is not absolute, and there are times when a signed waiver can be challenged and even thrown out by a judge.

When a Release Might Not Be Enforceable

Even with your signature on it, a release can be invalidated if it fails to meet certain legal standards. In Georgia, courts will scrutinize these documents to ensure they are fair and clear. If a release is fundamentally unfair or goes against public policy, it may not hold up.

Here are a few key situations where a release form might be overturned:

- Fraud or Misrepresentation: This happens if the insurance adjuster intentionally tricked you. A classic example is being told you're just signing a receipt for an initial payment when, in reality, it’s a full and final release. That’s fraud.

- Signing Under Duress: This means you were forced or coerced into signing. If an adjuster used extreme pressure, made threats, or cornered you when you were heavily medicated and vulnerable, a court could decide your signature wasn't voluntary.

- Vague or Ambiguous Language: Georgia law is clear on this: the language in a release must be unmistakable. If the text is so convoluted that a reasonable person couldn't figure out what rights they were giving up, a judge may rule it’s unenforceable.

- Gross Negligence or Willful Misconduct: You cannot legally sign away your right to sue someone for intentionally harming you. A release can't shield a person from the consequences of their own gross negligence—a reckless disregard for the safety of others.

It's a common myth that a signed waiver is an unbreakable shield for the at-fault party. The reality is quite different. While these forms offer protection, their legal power is often much weaker than their intimidating language suggests.

The Importance of Legal Interpretation in Georgia

Georgia’s state laws and court precedents are the rulebook for how contracts, including liability releases, are interpreted. Judges rely on this legal guidance to decide if a release is valid, always looking for fairness and clear intent from both parties.

This is precisely why having a professional legal review is so beneficial. An experienced attorney analyzes the document through the specific lens of Georgia law, spotting the weaknesses and loopholes that could invalidate the entire agreement.

To truly understand a release’s power, it’s helpful to know how courts approach legal agreements by mastering contract interpretation principles. This knowledge highlights why the exact phrasing of a what is a release of liability form matters so much. To learn more, take a look at our guide on the personal injury lawsuit process in Atlanta.

Spotting Unfair Clauses and Red Flags

Not all release forms are created equal, and the devil is always in the details. When an insurance adjuster hands you a document, remember it was drafted to give their company maximum protection—not you. Understanding what is a release of liability form means learning to read between the lines and recognize language that is unfair or overly aggressive.

Think of it like inspecting a used car. You wouldn't just kick the tires; you'd look under the hood for warning signs that could cost you thousands later on. The same principle applies here. You have to examine the document’s engine—the specific clauses—to spot the red flags.

Legal jargon can feel overwhelming, but certain phrases should immediately get your attention. These are the parts of the document designed to strip away more of your rights than is fair or necessary for a standard settlement.

Decoding Common Legal Clauses

Before you can spot the problems, it helps to understand the standard parts of a release. Insurance companies use specific legal phrases, or clauses, to define the scope of the agreement. Knowing what they mean is your first line of defense.

Here are a few of the most common clauses you’ll see:

- Release of All Claims: This is the core of the document. It states you are giving up your right to sue for any and all claims related to the incident, including physical injury, emotional distress, and property damage.

- Known and Unknown Injuries: This is a big one. This clause ensures the release covers not only the injuries you know about now but also any complications or new injuries that might surface later.

- Assumption of Risk: While more common in waivers you sign before an activity (like zip-lining), this language sometimes appears in post-injury releases. It’s an attempt to suggest you understood and accepted the potential for harm.

When looking at a release, an understanding of clear legal language is essential. The clearer the language, the easier it is to see when something isn’t right.

Major Red Flags to Watch For

Now, let's get to the problem areas. If you see language like this, it’s a signal to stop and seek legal advice immediately. Don't sign anything. These are clauses that go far beyond a standard, fair settlement.

1. Overly Broad and Vague Language

A huge red flag is any language that isn't specific to the accident you're settling. The release should clearly state it only covers claims arising from the specific incident on a particular date.

Watch out for phrases like "all claims whatsoever, from the beginning of time to the present day." This is a classic tactic to trick you into signing away your rights for completely unrelated issues you might have with that person or company.

2. Releasing Future Unrelated Claims

The release should never include language that absolves the at-fault party from responsibility for future, unrelated actions. Your settlement for a car accident in May shouldn't protect them if they hit you again in December.

3. Waiving Gross Negligence

As we've covered, Georgia law generally does not allow a person to waive their right to sue for someone else's gross negligence or intentional harm. Any clause that tries to release a party from liability for reckless or willful misconduct is a significant red flag and may be unenforceable in court.

4. Indemnification Clauses

This one is tricky but dangerous. An indemnification clause means that if someone else sues the at-fault party because of your injuries (like a health insurer wanting reimbursement), you would have to pay for the at-fault party’s legal defense. This is profoundly unfair and has no place in a standard personal injury release.

To help you tell the difference between what's normal and what's not, take a look at this quick comparison table. It shows how subtle wording changes can have a huge impact on your rights.

Red Flag Language vs. Standard Language

| Clause Type | Standard Language Example | Red Flag Example To Watch For |

|---|---|---|

| Scope of Release | "Releasor forever discharges Releasee from all claims arising from the accident on January 1, 2024." | "Releasor discharges Releasee from any and all claims, demands, and causes of action of every kind." |

| Covered Parties | "This release applies to John Smith and his insurer, XYZ Insurance." | "This release applies to the Releasee and their heirs, employees, agents, successors, and assigns." |

| Future Liability | The document is silent on future, unrelated events. | "Releasor agrees to indemnify and hold harmless the Releasee from any future claims…" |

Ultimately, identifying these red flags is important. The presence of any unfair clause in a release form is a clear sign that the other side is asking you to give up far more than you should.

Your Action Plan When an Insurer Presents a Release

It often happens fast. Shortly after an accident, the at-fault party's insurance adjuster is on the phone. They might sound sympathetic and eager to help, dangling a quick check to "make things right." But that offer is always attached to a document they need you to sign—a release.

This is a key moment. How you handle it can make or break your ability to get fair compensation. Knowing what is a release of liability form is the first step, but knowing what to do when one lands in your inbox is what truly protects you.

The most important thing you can do is simple: do not sign anything immediately. It's tempting to take the quick money, especially when you're stressed. But an adjuster’s job is to close your claim for as little as possible. A fast payout is their best tool.

The danger of a quick settlement is that you rarely know the full scope of your injuries right away. What feels like minor soreness can easily become a chronic back problem that requires extensive medical care down the road. Once you sign that release, your right to claim compensation for future medical bills, lost wages, or long-term suffering is gone forever.

Your Immediate Three-Step Response

When an adjuster calls and mentions a settlement, stay polite but firm. Your goal is to gather information without signing away your rights. Here’s a straightforward plan:

- Politely Decline to Sign: Simply state that you are not ready. You can say something like, "Thank you for the offer, but I won't be signing any documents until I fully understand my injuries and have had a chance to review everything."

- Request a Copy of All Documents: Ask the adjuster to email you the proposed release and the written settlement offer. This gives you a physical document to review without being pressured on the phone.

- Document Everything: Keep a log of every conversation. Note the date, time, the adjuster's name, and a summary of what you discussed. This record can be invaluable if a dispute comes up later.

This strategy puts you back in control. It slows down the insurance company's process and gives you the space you need to make an informed decision about your health and your financial future.

Why Legal Advice Is Your Strongest Asset

With the release form in hand, your next call should be to an experienced attorney. A lawyer can cut through the dense legal jargon and explain exactly what rights you're being asked to give up. Many people worry about the cost, but getting a professional opinion is more accessible than you might think.

According to data from legal service marketplaces, the average cost for an attorney to review a release of liability document is around $380.00. But most personal injury firms, including ours, work on a contingency fee basis. That means you pay no upfront costs, and we only get paid if we recover money for you. This makes getting a professional review completely risk-free. You can learn more about these legal service costs from ContractsCounsel.com.

A skilled attorney does more than just read the fine print. They will assess whether the settlement offer is actually fair by considering all your damages—current and future medical bills, lost income, and pain and suffering—to calculate the true value of your claim.

This is also where legal deadlines become a factor. Understanding the statute of limitations for personal injury in GA is non-negotiable, as waiting too long could bar you from filing a lawsuit altogether. Taking these steps ensures you don't accept a lowball offer and permanently sign away your right to the compensation you deserve.

Frequently Asked Questions About Liability Release Forms

When you’re trying to recover after an accident, the last thing you want is a confusing legal document shoved in front of you. We get it. Here are some straightforward answers to the questions we hear most often from our Atlanta clients about liability release forms. Knowing what this document really means is your first line of defense.

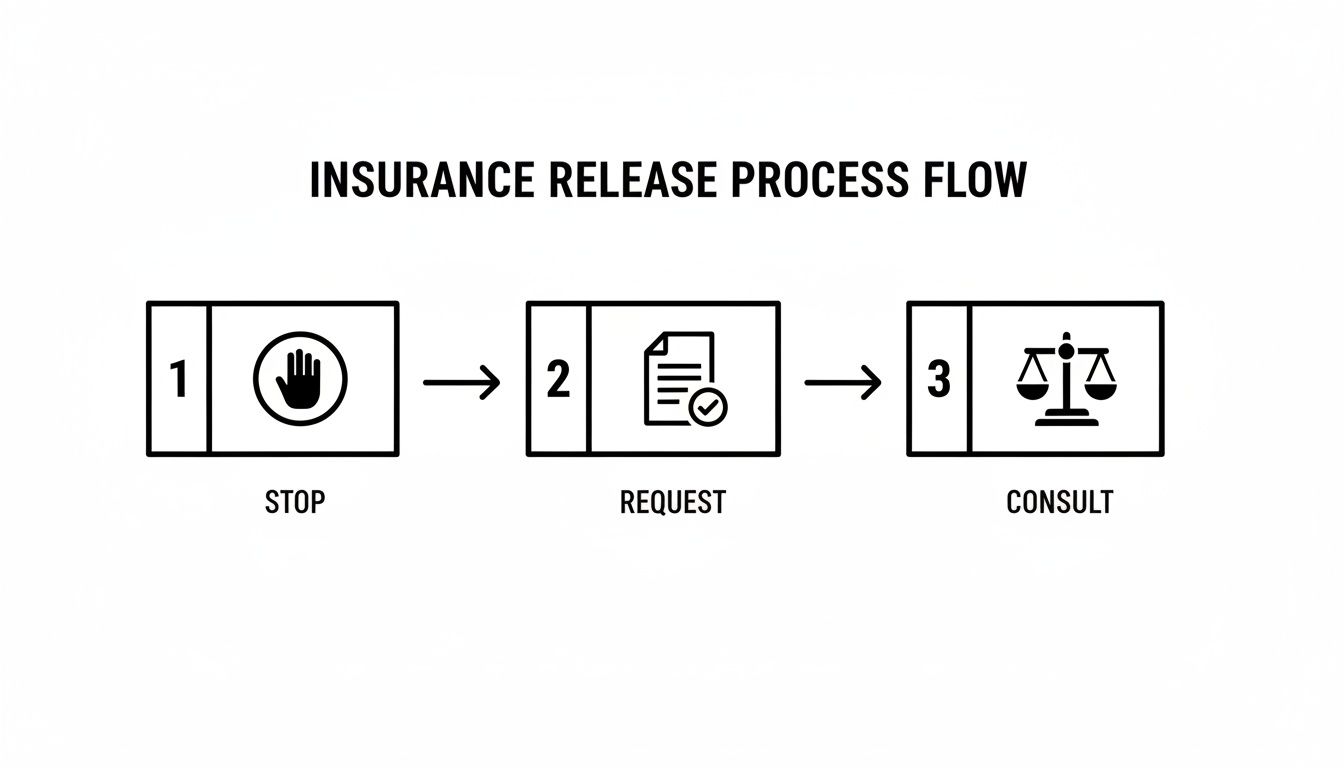

The insurance company wants you to act fast, but your best move is to slow down. This simple three-step process is a good approach.

This visual guide breaks it down: stop before you sign anything, request a copy of the document to review, and always consult with a professional before making a final decision.

Can I sue if I already signed a release of liability form?

This is a tough spot to be in, and honestly, the answer depends entirely on the specific facts of your case. While signing a release makes it much harder to pursue a claim, it's not always the end of the road.

A Georgia court might invalidate a waiver if you can prove you signed it under duress (meaning you were unfairly pressured), because of fraud (you were lied to about what you were signing), or if the terms are just plain against public policy—like trying to waive responsibility for intentional harm.

The language in the release also has to be crystal clear. If it’s vague, poorly written, or ridiculously broad, a judge may rule that it's unenforceable.

Your best bet is to have an experienced personal injury attorney look at the document and the circumstances under which you signed it. We can analyze the language and the context to see what legal options might still be on the table. A signature doesn't always close the door for good.

What is the difference between a waiver and a release of liability?

People often use these terms interchangeably because they both involve giving up your right to sue. The real difference comes down to timing.

-

A waiver is something you sign before you participate in an activity. Think about signing up for a gym or going rock climbing. You’re agreeing in advance not to sue for injuries that are considered a normal risk of that activity. You can learn about different types of waivers from helpful resources like Wikipedia.

-

A release of liability, on the other hand, is signed after something has already happened, usually as part of a settlement. After a car wreck, you sign a release to get the settlement check from the insurance company. In doing so, you release them from any future claims related to that specific accident.

Basically, a waiver deals with potential future risks, while a release settles a claim for an injury that has already occurred.

Why shouldn't I accept the insurance company's first offer?

It’s simple: insurance companies are in business to make a profit, and that means paying out as little as possible on claims. Their first offer is almost always a lowball figure, far less than what your claim is actually worth. They are banking on you taking the quick cash before you understand the true, long-term cost of your injuries.

Once you sign that release and cash that check, it’s over. You can’t go back and ask for more money, even if your injuries get worse. A back sprain that seems minor today could require surgery six months from now.

By waiting, you give yourself the time to get a full medical picture from your doctors and consult an attorney who can calculate the true value of your claim. This ensures you’re fighting for fair compensation, not just a fast payout.

That initial offer isn't a gesture of goodwill; it's a business tactic. Protecting your health and financial future requires a more patient and strategic approach.

Does a release cover injuries I don't know about yet?

Yes, it absolutely does—and this is one of the biggest traps. A standard release form will include broad language that releases the at-fault party from "all claims, known and unknown." That phrase isn't there by accident. It’s written specifically to give the insurance company total protection from any future costs.

This means you’re giving up your right to sue for any injury related to the accident, even one that hasn't shown up yet. If you accept a few thousand dollars and later find out you have a herniated disc that needs surgery, you will almost certainly have no legal recourse to get compensation for it.

This "unknown claims" clause is precisely why you should never sign anything until you've reached what doctors call "maximum medical improvement" (MMI). MMI is the point where your condition has stabilized, and your doctor has a clear understanding of your long-term prognosis and any future medical needs. Until you hit MMI, you can't possibly know the full value of your claim, making it impossible to sign away your rights fairly. This is a key part of understanding what is a release of liability form and its permanent impact.

If you've been injured and an insurance adjuster is pressuring you to sign a release of liability form, don't give up your rights. Contact Jamie Ballard Law for a free, no-obligation case evaluation. We will help you understand your options and fight for the full and fair compensation you are owed. Visit us at https://jamieballardlaw.com.