After a serious accident, the financial decisions you make can shape the rest of your life. As an Atlanta Personal Injury attorney, I've seen firsthand how important it is to understand the choice between a structured settlement vs lump sum payout. The distinction is simple enough: a lump sum delivers all your money at once, while a structured settlement provides guaranteed payments over a set period. Making the right choice for your family's future starts with understanding how each option works.

Choosing Your Settlement Path in Georgia

Deciding how you'll receive your settlement funds is a deeply personal choice, one that has to align with your immediate needs and long-term financial goals. There's no single "right" answer here. The key is understanding exactly what each path offers so you can make an informed decision that secures your future.

The two options couldn't be more different in how they deliver your compensation.

- Lump Sum Payout: You get a single, large payment. From that moment on, the money is entirely yours to manage, invest, or spend however you see fit. It gives you immediate access and total control.

- Structured Settlement: This route provides a steady, predictable income stream. Payments are scheduled over an agreed-upon timeline—whether that’s a few years or a lifetime—offering built-in financial security.

Key Differences at a Glance

To put it in perspective, let's lay out the main distinctions between a structured settlement and a lump sum. This table gives a high-level view of how they stack up.

| Feature | Structured Settlement | Lump Sum |

|---|---|---|

| Payment Method | A series of scheduled payments over time | A single, one-time payment of the full amount |

| Financial Control | Limited; funds are paid out on a fixed schedule | Complete and immediate control over all funds |

| Long-Term Security | High; provides a guaranteed, predictable income stream | Lower; security depends entirely on your financial management |

| Tax Implications | Payments are generally 100% income tax-free | The initial amount is tax-free, but any investment gains are taxable |

| Market Risk | None; payments are guaranteed and not tied to the market | High; your funds are subject to market risk if you invest them |

Ultimately, a lump sum offers freedom, while a structured settlement provides certainty.

One of the most powerful benefits of a structured settlement is the built-in financial discipline. It acts as a safety net, ensuring you have funds for future needs without the risk of mismanagement or spending it all too quickly.

This stability is why structured settlements are so often recommended for people with long-term injuries or ongoing medical needs. In fact, studies show that roughly 60-70% of settlement recipients choose structured payments precisely for that kind of long-term security. You can dig deeper into the advantages of settlement planning to see if it's the right fit for you.

At the end of the day, the choice of a structured settlement vs lump sum comes down to balancing what you need right now with what you'll need for years to come.

The Reality of a Lump Sum Payout

Getting your entire settlement at once gives you immediate and total control over the money. That’s a powerful advantage in the structured settlement vs lump sum debate. This single payment is incredibly useful for tackling the big, immediate costs that almost always follow a serious accident. You can wipe out medical bills, clear away debt, or pay for accessibility upgrades to your home right away.

Of course, that level of control comes with an equal measure of responsibility. The psychological weight of managing a large sum of money can be intense. It absolutely demands discipline and a rock-solid plan to make sure those funds last for the long haul.

Financial Management and Potential Pitfalls

For many accident victims, the single biggest challenge of a lump sum is managing it effectively. While the settlement itself is generally not taxable for personal injury claims, any money you earn by investing it almost certainly is. That's an important distinction that can have a major impact on your financial future.

Without a sound strategy, it's easy to fall into common traps:

- Overspending: The urge to make big purchases or lend money to loved ones can drain funds that were meant to cover a lifetime of care.

- Poor Investment Choices: Without good advice, you can easily sink your money into risky investments that lead to devastating losses.

- No Budget: If you don't create a detailed financial plan, the money can vanish much faster than you ever thought possible.

These risks aren't just possibilities; they're common outcomes. It's why disciplined financial planning is non-negotiable if you take a lump sum.

Suddenly coming into a large settlement is overwhelming. We've all heard stories about lottery winners who end up broke within a few years due to mismanagement. The exact same risk applies to settlement payouts.

If a lump sum is your choice, learning to manage and grow that money is your top priority. You’ll need to evaluate investment opportunities to make your settlement work for you. A lump sum gives you the power to invest, but it also means you carry 100% of the risk.

Real-World Scenarios for a Lump Sum

Despite the risks, a lump sum is sometimes the clear best choice. It gives you the capital needed for major life investments that can improve your quality of life or open up new opportunities.

Think about these situations where a lump sum really makes sense:

- Paying Off a Mortgage: Getting rid of your single biggest monthly bill provides incredible financial breathing room and stability for the rest of your life.

- Starting a Business: For anyone with an entrepreneurial drive, a lump sum can be the seed money needed to launch a new venture and build a new source of income.

- Funding Education: You could use the money to pay for your own college degree or set up a secure education fund for your children.

Each of these examples is about using the settlement for a significant, one-time investment aimed at building a stronger future. The decision between a structured settlement vs lump sum comes down to whether you have the discipline and the right circumstances to manage these responsibilities and opportunities.

Building Security with a Structured Settlement

When you're weighing a structured settlement vs lump sum, think of the structured settlement as a financial safety net. It's built for one thing: long-term stability. Instead of getting all your compensation at once, this option provides a steady, predictable stream of payments over months, years, or even a lifetime. It’s a method specifically designed to safeguard your future.

At its core, a structured settlement is an annuity—a financial product bought from a top-rated life insurance company. The defendant in your case uses the settlement funds to purchase this annuity for you. From that point on, the insurance company is legally obligated to send you guaranteed payments on a pre-set schedule. This shifts the payment responsibility away from the defendant and places it in the hands of a secure financial institution.

How a Structured Payment Plan Works

The real power of a structured settlement is its predictability. Once the agreement is signed, your payments are locked in. They're insulated from stock market volatility and economic downturns. You know exactly how much money you’ll get and when you’ll get it, creating a reliable foundation for your life after an accident.

This consistency is valuable for managing ongoing needs like:

- Long-term medical care: This covers everything from future surgeries and physical therapy to prescription drugs and in-home assistance.

- Monthly living expenses: Your payments can replace lost income, helping you cover rent, groceries, and other daily essentials without worry.

- Adaptive equipment: Funds can be scheduled to align with the future costs of replacing or upgrading medical devices or home modifications.

By its very nature, this approach removes the pressure of managing a large sum of money and protects it from being spent too quickly. It’s a disciplined financial tool that ensures the money is there when you truly need it.

Customizing Your Payments for Life's Milestones

It’s a common myth that structured settlements are inflexible. The truth is, they can be highly customized to fit your specific life circumstances and goals. Your payment schedule doesn’t have to be a simple monthly check; it can be strategically designed around life’s biggest moments.

The flexibility to plan for future lump sums is a powerful, often overlooked feature of structured settlements. You can build a payment schedule that aligns directly with your family’s most important financial milestones.

For example, you can design a plan that includes:

- Scheduled Lump Sums for Education: You could arrange for a larger payment to arrive when your child turns 18 to help cover college tuition.

- Retirement Planning: The structure can provide larger payments or a lump sum when you reach retirement age, supplementing other income sources.

- Major Future Purchases: If you know you'll need a new, specially equipped vehicle in ten years, a payment can be scheduled to cover that exact cost.

This level of customization provides incredible peace of mind. It lets you plan for what’s ahead with confidence, knowing the funds for major life events are already secured and guaranteed to arrive on time. The choice between a structured settlement vs lump sum often comes down to whether this kind of predictable, long-term security serves your life better than immediate access to all the cash.

Comparing Tax Rules and Market Risks

When weighing a structured settlement vs lump sum, the conversation almost always turns to taxes and market risk. Here's why: while personal injury settlement funds are generally not considered taxable income by the IRS, the way you receive that money completely changes your financial future.

This single difference—guaranteed, tax-free security versus the potential for higher growth paired with market risk—is often the deciding factor for our clients.

Tax Treatment Side by Side

The tax rules for personal injury settlements are a huge advantage, but they don't apply equally to each payout method. You can find official guidance on this in IRS Publication 525.

Periodic payments from a structured settlement are 100% income tax-free. Period. Every dollar that hits your bank account from the annuity is yours to keep, and you don't even have to report it on your tax return.

A lump sum is also tax-free initially. That first check is not considered income. But the moment you invest that money, any interest, dividends, or capital gains it earns are almost always taxable. This means you've just signed up for an ongoing tax management job that simply doesn't exist with a structured settlement.

This screenshot from IRS Publication 525 clarifies which settlement proceeds are taxable and which are not.

The bottom line is that compensation for physical injuries is non-taxable. This is why the initial lump sum and all structured settlement payments are tax-free. However, any money you make by investing a lump sum is not covered by that protection.

To give you a clearer picture, let's break down the key financial implications.

Financial Implications Side by Side

| Financial Factor | Structured Settlement | Lump Sum |

|---|---|---|

| Tax on Payments | 100% tax-free. No federal or state income tax on payments. | Initial amount is tax-free. |

| Tax on Growth | Not applicable. Payments are guaranteed and not invested in the market. | Taxable. Interest, dividends, and capital gains are subject to taxes. |

| Market Exposure | Zero market risk. Payments are guaranteed by a life insurance company. | Fully exposed. Your principal is subject to market volatility and potential loss. |

| Long-Term Value | Predictable, guaranteed income stream for life or a set period. | Potential for higher growth but also significant depletion from losses or poor decisions. |

As you can see, the path you choose creates two very different financial realities. One is built on certainty, the other on potential.

Market Exposure and Growth Potential

Your appetite for risk is the other major piece of this puzzle. A structured settlement is completely insulated from market volatility. Your payments are backed by a highly-rated life insurance company, so they won't change whether the stock market is up or down. For many, that provides incredible peace of mind.

A lump sum, on the other hand, is directly tied to the market once you invest it. This is both its biggest advantage and its greatest weakness.

- Potential for Higher Growth: Smart investing could grow your lump sum far beyond what a structured settlement would pay out over time.

- Risk of Significant Loss: A market crash or a few bad investment calls could wipe out a large portion of your funds, leaving your future uncertain.

If you take the lump sum, you'll need to get smart about investing—fast. Understanding concepts like these tax loss harvesting strategies becomes important to protecting your money. While the statute of limitations for a personal injury claim in Georgia dictates the timeline for filing your case, the financial choices you make after a settlement will follow you for the rest of your life.

An important finding from legal research shows that companies often offer to buy out structured settlements for a lump sum at a massive discount—sometimes as high as 70% of the total value. This practice alone highlights just how valuable that guaranteed, long-term payment stream really is.

Ultimately, the choice comes down to your personal risk tolerance. Do you value the guaranteed safety of tax-free payments, or are you comfortable taking on market risks for a shot at greater financial growth? Answering that question is the key to the structured settlement vs lump sum decision.

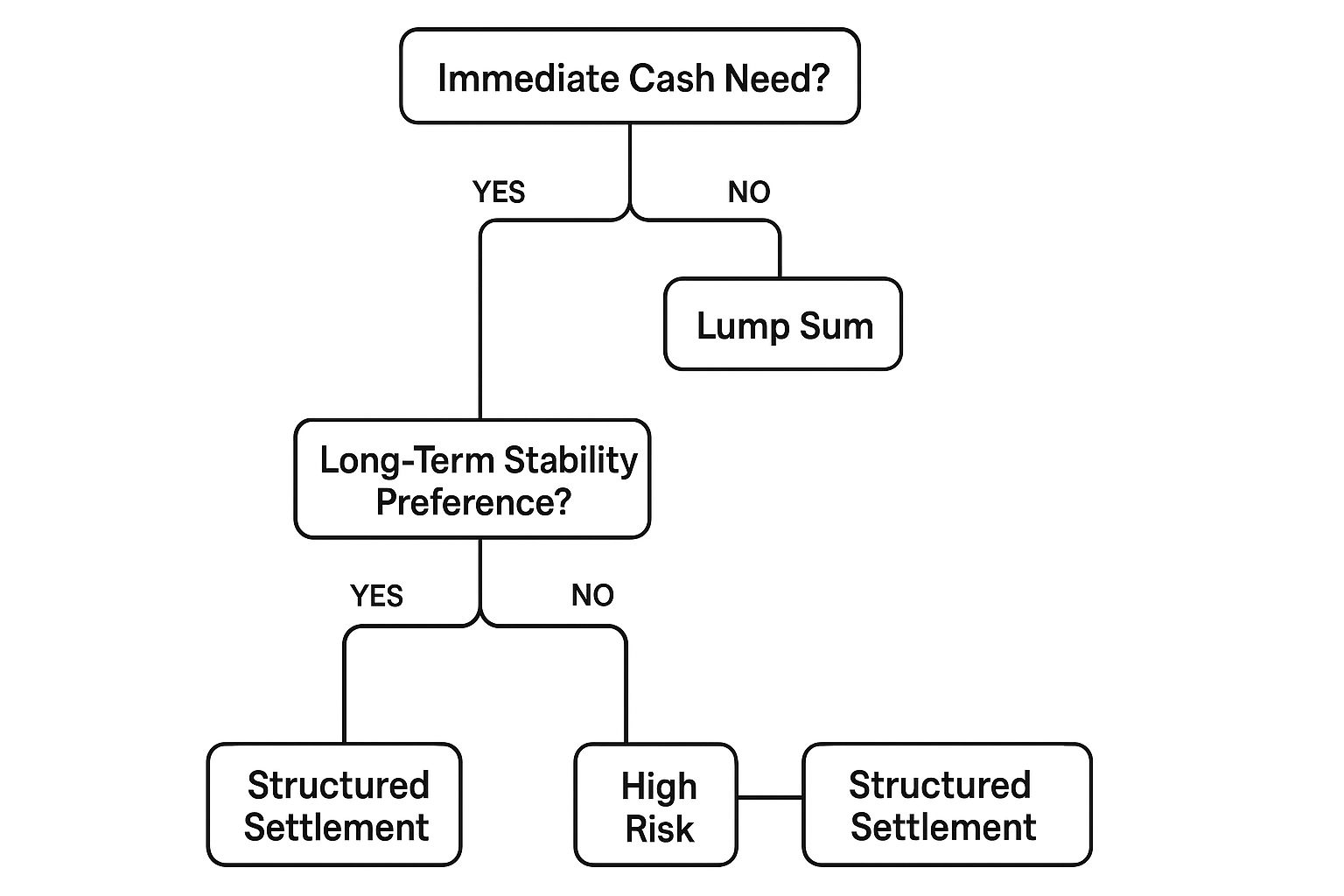

Deciding Which Settlement Option Fits Your Life

When you're facing the structured settlement vs lump sum decision, there's no universally correct answer. The best choice is deeply personal—it has to align with your life, your goals, and your financial discipline. This isn't just about what looks better on paper; it's about securing the resources you need to move forward with stability after an injury.

Making an informed choice starts with creating a comprehensive financial plan that maps out your long-term needs. A solid plan gives you a clear roadmap, pointing you toward the option that best serves your future.

Questions to Guide Your Decision

To determine which path aligns with your reality, take some time to reflect on these important questions. Your honest answers will illuminate the right direction.

- What are my immediate financial needs? Do you have towering medical bills, outstanding debts, or a mortgage that needs to be paid off now? If you're facing large, upfront costs, a lump sum might be the more practical solution.

- What are my long-term financial goals? Are you planning for decades of future medical care, replacing lost income, or ensuring a stable retirement? For long-range security, a structured settlement often provides a more reliable foundation.

- How comfortable am I with managing a large sum of money? Be realistic about your financial experience. If budgeting and investing aren't your strong suits, a structured settlement provides built-in financial management and protects the funds from mismanagement.

The decision tree below can help you visualize how your answers to these core questions guide your choice.

As the visual guide shows, the decision often comes down to balancing immediate financial pressures against long-term security and your personal tolerance for risk.

Real-World Scenarios

Let's look at how these choices play out in different situations. Context is everything, and seeing these options in a real-world light can make the best path forward much clearer.

Scenario 1: The Catastrophic Injury

An Atlanta construction worker sustains a severe spinal cord injury, leaving him unable to work and in need of lifelong medical care. For this individual, a structured settlement is almost certainly the superior option.

- Why it works: It provides a guaranteed, tax-free income stream to cover ongoing medical treatments, in-home assistance, and daily living expenses for the rest of his life. This removes the immense pressure of managing investments while handling serious health challenges.

Scenario 2: The Savvy Investor

A marketing executive is injured in a car accident but is expected to fully recover and return to her high-paying job within a year. She has a strong financial background and a detailed plan for her settlement funds.

- Why a lump sum works: She can take a lump sum to immediately eliminate medical debt and pay off high-interest loans. Confident in her ability to manage investment risk, she can use the remaining funds to diversify her portfolio, potentially generating returns that outpace a structured annuity.

Choosing your settlement path is one of the most significant financial decisions you will ever make. It is not a choice to be made lightly or alone. Discussing your specific situation with a legal professional can provide the clarity needed to protect your future.

If you are weighing these options and need guidance tailored to your specific case in Georgia, we are here to help. You can contact us for a free evaluation to discuss your circumstances and determine which path best secures your financial well-being.

Ultimately, the right choice in the structured settlement vs lump sum debate depends entirely on your personal needs, your long-term vision, and your comfort level with financial management.

Frequently Asked Questions About Georgia Settlements

Deciding between a structured settlement vs. a lump sum is a major financial crossroad, and it’s completely normal to have a lot of questions. When you’re dealing with the aftermath of an accident in Georgia, you need clear answers about the details that will shape your future for years to come.

We've compiled the most common questions our clients ask to provide straightforward, practical answers and help you make a better choice. Think of this as a starting point to prepare you for deeper conversations with your legal and financial teams.

Can I Combine a Lump Sum and a Structured Settlement?

Yes, you can—and it’s a very popular strategy. This "hybrid" or "blended" settlement approach often gives people the best of both worlds.

Here's how it works: you take an initial lump sum to handle immediate financial pressures. This could mean paying off outstanding medical bills, wiping out high-interest debt that's been piling up, or funding necessary home modifications for accessibility. With those urgent needs covered, the rest of the settlement funds are used to purchase an annuity. This creates a structured settlement that provides a guaranteed income stream for the long haul.

This strategy delivers immediate relief without sacrificing long-term financial security.

What Happens to My Structured Settlement if I Pass Away?

This is a very important concern, especially for anyone with dependents. Your structured settlement is an asset, and you have the right to name a beneficiary who will receive any remaining payments if you die before the annuity term is over.

During the settlement agreement process, you'll officially designate who should inherit any guaranteed payments. This ensures that your loved ones continue to receive that financial support, providing stability after you're gone. The payments simply continue on the original schedule until the term is complete.

One of the most important aspects of naming a beneficiary is that the tax-free status of the payments typically passes to them. This means your family gets the full value of the remaining funds without being hit with an unexpected income tax bill.

Are Structured Settlements Flexible After They Are Set Up?

Once a structured settlement agreement is signed and the annuity is purchased, the payment schedule is legally locked in. You cannot alter the amount or the timing of the payments. This rigidity is intentional; it's what ensures the income stream remains stable and guaranteed for its entire term.

Because of this inflexibility, it is absolutely essential to design a payment schedule that anticipates your future needs before signing anything. While you technically can sell your future payments to a factoring company for a lump sum, it's almost always a poor financial move. These companies buy the payments at a massive discount, meaning you'll receive only a fraction of their true value.

How Does Inflation Affect My Settlement Choice?

Inflation is a key factor in any long-term financial decision and should not be overlooked.

- Lump Sum: If you take the money upfront and invest it, your goal is for your investment returns to beat inflation. This can grow your wealth, but it also comes with market risk. There's no guarantee your investments will perform as expected.

- Structured Settlement: You can build inflation protection right into your agreement. This is done with a Cost-Of-Living-Adjustment (COLA) rider. A COLA automatically increases your periodic payments by a fixed percentage—say, 3% each year—to help your income keep pace with the rising cost of living.

A COLA provides significant peace of mind, ensuring your future income doesn’t lose its purchasing power over the years. For more insights into your legal options, feel free to explore the articles in our Atlanta personal injury resources.

Will a Settlement Affect My Government Benefits?

Yes, it can, and this is an important detail to get right. Receiving a large settlement—especially as a lump sum—can push your assets over the strict limits for needs-based government programs like Medicaid and Supplemental Security Income (SSI). This could disqualify you from receiving essential benefits.

A well-designed structured settlement can help protect your eligibility. By keeping the periodic payments below certain income thresholds, you may be able to maintain your benefits. For more complex situations, establishing a Special Needs Trust is often the best strategy to manage settlement funds without jeopardizing government assistance. It's vital to discuss this with your attorney to ensure your settlement doesn't accidentally cut you off from the support programs you rely on.

Understanding these finer points is necessary to making the right choice between a structured settlement vs. a lump sum.

At Jamie Ballard Law, we understand that the aftermath of an accident is filled with difficult decisions. If you're weighing your options and need clear guidance tailored to your specific situation in Georgia, we are here to help you secure the best possible outcome for your future.