As an Atlanta personal injury attorney, I often see the real-world impact of car accidents. A frequent question I hear is about the Georgia minimum car insurance requirements. In Georgia, every driver is legally required to carry a baseline of liability insurance. The numbers are specific: $25,000 for bodily injury to one person, $50,000 for total bodily injury per accident, and $25,000 for property damage.

This is known in the insurance world as "25/50/25" coverage, and it’s the absolute floor for what you need to legally operate a vehicle in our state.

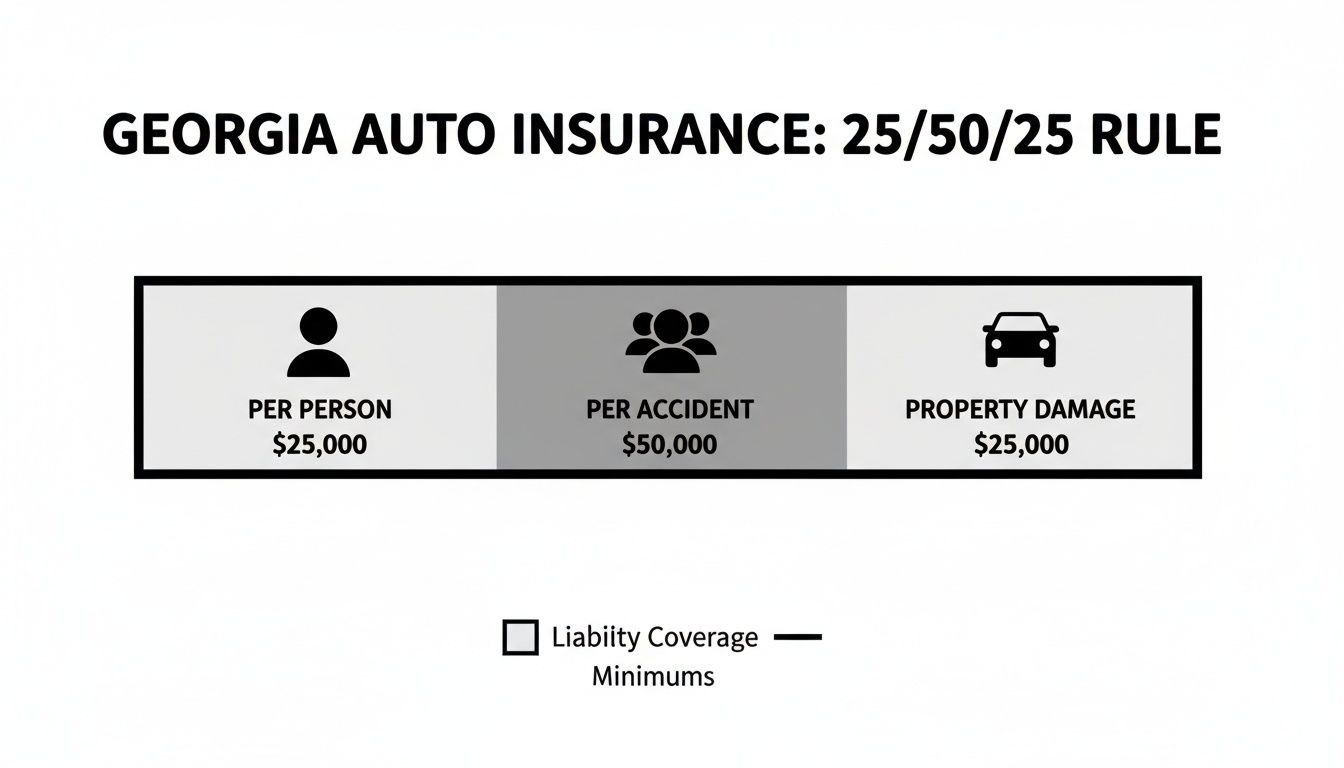

What Georgia's 25/50/25 Rule Really Means for You

Think of the Georgia minimum car insurance requirements as your ticket to drive on Georgia roads. It’s the baseline level of financial responsibility the state says you must have in case you cause an accident. Because Georgia is a "fault" state (a concept you can learn more about on sites like Wikipedia)), the driver who causes the collision is responsible for the damages. This minimum coverage is their first line of defense.

These numbers aren't just pulled out of thin air; they represent the hard caps on what your insurance company will pay out if you’re at fault. For years, these figures have been the standard, though as medical and repair costs climb, their real-world value is constantly being tested. A recent FOX 5 Atlanta report on rising insurance costs highlights just how long this 25/50/25 standard has been in place to protect drivers.

Breaking Down the Numbers

So, what does each part of that 25/50/25 formula actually do? Let’s get practical.

- $25,000 Bodily Injury Liability (Per Person): This is the most your insurance will pay for a single person's medical bills if you injure them in a crash.

- $50,000 Bodily Injury Liability (Per Accident): If you injure two or more people, this is the total pot of money your policy will pay for all of their combined medical expenses. No single person can get more than the $25,000 individual limit.

- $25,000 Property Damage Liability (Per Accident): This bucket of money covers the cost to repair or replace the other person’s car. It also covers any other property you might have damaged, like a mailbox or a storefront.

It’s important to get comfortable with these concepts, as they’re the building blocks of any auto policy. For a closer look at these and other key insurance terms, our firm’s legal dictionary is a great resource.

To help visualize it, here's a simple breakdown of the state's required minimums.

Georgia's 25/50/25 Minimum Liability Coverage at a Glance

| Coverage Type | Minimum Required Limit |

|---|---|

| Bodily Injury Liability (per person) | $25,000 |

| Bodily Injury Liability (per accident) | $50,000 |

| Property Damage Liability (per accident) | $25,000 |

This table shows the absolute minimums, but as you'll see, these amounts can be exhausted very quickly after a serious crash.

Here's the most important takeaway: Liability insurance pays for their bills, not yours. It is designed to cover the other party's injuries and property damage when you are the one who caused the accident.

That distinction is key. This basic coverage does absolutely nothing for your own medical bills or your own car repairs if you’re at fault. That’s where other, optional coverages come into play. Understanding the Georgia minimum car insurance requirements is just the first step—making sure you're truly protected is the next.

Why Minimum Coverage Often Falls Short After a Crash

Meeting the Georgia minimum car insurance requirements keeps you legal on the road, but let’s be clear: it rarely keeps you financially safe. Think of the state-mandated 25/50/25 policy as a small bandage for a serious wound. It's better than nothing, but it’s almost never enough to cover the real costs of a significant car wreck.

Let's walk through a common scenario right here in the Atlanta area to see just how quickly those minimum limits evaporate. Imagine you’re found at fault for a collision on I-285 during rush hour. The other driver is taken to the hospital by ambulance with a broken arm and a concussion.

The Real Cost of a "Minor" Injury

The expenses start piling up immediately. An ambulance ride in metro Atlanta can easily top $1,500. A trip to the emergency room for X-rays, a CT scan, and initial treatment can add another $5,000 to $10,000 without breaking a sweat.

Right there, that one person's medical bills are already eating up half of your $25,000 bodily injury liability limit. And that doesn't even begin to account for the other costs that are sure to follow:

- Follow-up Appointments: The injured driver will need to see specialists, like an orthopedist for their broken arm.

- Physical Therapy: Recovering from these injuries will almost certainly require weeks or even months of rehabilitation.

- Lost Wages: They can't work while they recover, and your policy is on the hook for that lost income.

When you add it all up, it's incredibly easy for one person's medical claim to blow past the $25,000 per-person limit. Once your insurance pays out that maximum amount, the injured party’s attorney will come after you personally for the rest.

What About the Car?

Now, let's look at the property damage. The $25,000 limit might sound like a decent number, but the price of new vehicles has gone through the roof. Many new cars, trucks, and SUVs on Georgia roads are valued at well over $30,000. Even a fender-bender can result in thousands in repairs thanks to all the advanced sensors, cameras, and safety features packed into modern bumpers.

If you cause a multi-car pileup or hit a more expensive vehicle, that $25,000 can disappear in an instant. You'll be left paying the remaining balance directly out of your own pocket.

This visual breaks down the basic structure of Georgia's 25/50/25 liability coverage.

Each of these limits—per person, per accident, and for property damage—is a hard cap on what your insurer will pay. This is where your personal financial exposure begins.

The bottom line is that minimum coverage is designed to protect other people from the damage you cause, but its low limits offer very little protection for your own financial future. When the damages exceed your policy limits, your personal assets, savings, and even future wages could be at risk.

This is exactly why so many insurance and legal professionals strongly recommend carrying liability limits far higher than the state minimums. Understanding the different facets of personal injury claims can make it even clearer why adequate coverage is so important for protecting yourself. While this isn't legal advice, it turns abstract policy numbers into a tangible financial risk, showing why relying solely on the Georgia minimum car insurance requirements is a gamble most people can't afford to lose.

The Real Reasons Your Car Insurance Costs Are Rising

If you've opened your car insurance bill recently and felt a bit of sticker shock, you’re not alone. It's a frustrating reality for drivers all across Georgia. That feeling that your rates are climbing for no good reason is common, but the truth is several powerful factors are pushing premiums upward for everyone, regardless of your personal driving record.

The core of the issue is shared risk. Insurance companies don't just set your rates based on your personal driving habits; they look at the collective experience of all drivers in a specific area. When the overall risk of accidents, theft, and expensive claims goes up in Georgia, everyone's premiums feel the impact. Think of it like a group project—the final grade is affected by everyone's performance, not just your own.

The Financial Squeeze on Georgia Drivers

The numbers paint a pretty stark picture of this financial pressure. Recent data shows a startling trend for drivers in our state. The sharp 22% rise in Georgia car insurance premiums from 2022 to 2023—jumping from $1,617 to $1,973 annually for full coverage—is a direct result of the state's minimum 25/50/25 requirements struggling to keep up with escalating claims and accidents.

This increase actually outpaced 30 other states. It was fueled by a shocking 35.4% spike in traffic deaths per million miles from 2019-2021, on top of higher vehicle thefts and urban crashes, especially in areas like Atlanta. This isn't some abstract economic trend; it has a direct and painful effect on household budgets across our communities. When the cost of covering potential accidents rises so dramatically for insurers, they inevitably pass those costs on to you.

Several key issues are contributing to this environment:

- Increased Traffic Density: Metro Atlanta is one of the fastest-growing regions in the country. More cars clogging I-75, I-85, and the Perimeter simply means a higher statistical likelihood of collisions.

- Higher Accident Severity: Modern cars are safer for the people inside, but they're also far more expensive to repair. The advanced sensors and technology packed into bumpers, windshields, and side panels mean a simple "fender bender" can now easily turn into a multi-thousand-dollar repair bill.

- Rising Medical Costs: Just like vehicle repairs, medical expenses have surged. The cost of an ambulance ride, an emergency room visit, and the physical therapy that follows has climbed, meaning injury claims now cost insurers much more than they did a decade ago.

- Vehicle Theft Rates: Unfortunately, Georgia has also seen a rise in auto thefts. Beyond your driving record, installing certain features can influence what you pay. For instance, you can save on premiums with anti-theft devices for cars insurance.

The Problem of Uninsured Drivers

One of the biggest factors driving up costs for responsible drivers is the sheer number of uninsured motorists on our roads. When a driver who has followed the law and bought insurance is hit by someone with no coverage, the responsible driver's own policy often has to cover the damages, particularly if they carry Uninsured Motorist coverage.

This creates a system where insured drivers are essentially subsidizing the risks created by those who break the law. Insurers factor this added risk into their rate calculations, which means you pay more because a notable percentage of other drivers pay nothing at all.

This problem is widely recognized, and there are ongoing discussions at the state level about how to tackle both rising costs and the enforcement of insurance laws. For anyone looking for more information on related legal topics, our firm provides a variety of helpful materials in our online resources section. These legislative conversations are slow, but they show an understanding that the current Georgia minimum car insurance requirements are under serious strain in today's economic environment.

Protecting Yourself with Uninsured Motorist Coverage

While Georgia’s minimum insurance laws keep you legal on the road, they operate on a huge assumption: that every other driver is just as responsible as you are. That’s a risky bet to make.

This is exactly why Uninsured and Underinsured Motorist (UM/UIM) coverage is so important, even though it’s not part of the official georgia minimum car insurance requirements. It’s your personal financial backstop in a state with a surprising number of drivers who have no coverage at all.

Think of UM/UIM coverage as a shield you buy for yourself and your family. It’s an optional add-on that kicks in when you’re hit by someone with no insurance (uninsured) or whose policy is too small to cover your bills (underinsured).

How Uninsured Motorist Coverage Works in Real Life

Let’s play out a common Atlanta scenario. You’re driving home from work when another driver runs a red light and T-bones your car. They’re clearly at fault. But when the police arrive, you learn the other driver let their insurance policy lapse. They have zero coverage.

Without UM coverage, you’re in a tough spot. Your only option is to sue the at-fault driver personally, which is often a long, expensive, and ultimately frustrating process. If they don’t have assets, you may never see a dime.

But with UM coverage, the story changes. Your own insurance company steps up to fill the gap left by the uninsured driver. They will pay for your medical bills, lost income, and pain and suffering up to your UM policy limits—doing the job the other driver's insurance should have done.

The Uninsured Driver Problem in Georgia

This isn't just a theoretical problem; it’s a daily reality on our roads. With somewhere between 12% and 18% of Georgia drivers operating without insurance, our state ranks among the top 10 worst in the nation for uninsured motorists. That’s a lot higher than the national average.

This fact alone makes the state's 25/50/25 minimums feel inadequate. When you’re sharing the road with so many drivers who can’t pay for the damage they cause, having your own protection is essential. For more context on how these numbers impact Georgia drivers, you can explore details about state car insurance.

This coverage is your safety net. It ensures that your financial recovery isn’t dependent on the responsibility—or irresponsibility—of another driver. It’s a proactive way to protect your own well-being.

Stacking vs. Non-Stacking UM Coverage

When you add UM coverage, your agent will ask if you want "stacking" or "non-stacking." The choice you make has a massive impact on how much coverage is available after a crash.

- Non-Stacking Coverage: This is the standard, more affordable option. Your UM coverage limit is a fixed amount per accident, period. If you have a $100,000 non-stacking UM policy, that is the absolute most you can recover from it.

- Stacking Coverage: This lets you combine—or "stack"—the UM coverage limits for multiple vehicles on your policy. If you insure two cars, each with $100,000 in UM coverage, a stacking policy gives you a total of $200,000 in available benefits after being hit by an uninsured driver.

Stacking policies cost a bit more, but the extra layer of protection can be a lifesaver after a severe injury. In fact, Georgia law considers this coverage so important that insurance companies are required to offer it to you. You must formally reject it in writing if you don’t want it, a clear sign that it’s a vital protection that goes far beyond the basic georgia minimum car insurance requirements.

Consequences of Driving Without Insurance in Georgia

Getting caught driving in Georgia without insurance is a far bigger deal than a simple traffic ticket. It’s a serious misdemeanor offense, and the consequences are immediate, expensive, and designed to send a clear message: the risk isn't worth it.

Forget about fumbling for a paper insurance card. Law enforcement officers can now verify your coverage status instantly using the Georgia Electronic Insurance Compliance System (GEICS). Insurance companies continuously update this statewide database, giving police real-time access. If GEICS shows your policy has lapsed, there’s no talking your way out of it.

Immediate Legal and Financial Penalties

The moment you're pulled over—or worse, after an accident—and found to be uninsured, a cascade of problems begins.

For a first-time offense, the penalties are no slap on the wrist. Here’s a look at what you can expect to face immediately:

To summarize the consequences, here is a breakdown of what a first-time offender can anticipate.

Penalties for a First-Time Uninsured Driving Offense in Georgia

| Penalty Type | Description of Consequence |

|---|---|

| Misdemeanor Charge | You will be charged with a criminal offense that goes on your permanent record. |

| Significant Fines | Expect fines ranging from $200 to $1,000, plus additional court costs and fees. |

| License Suspension | Your driver's license will be suspended for a mandatory period of 60 to 90 days. |

| Vehicle Registration Suspension | The registration for the vehicle involved will be suspended, rendering it illegal to drive. |

These are just the initial penalties. Getting your license and registration reinstated involves paying steep fees that can add hundreds more to your total bill. For a deeper look at these issues, you can review this general guide on what happens if you don't have insurance.

The Added Burden of an SR-22 Filing

After a conviction, the state will almost certainly require you to get an SR-22 filing. This isn't a type of insurance. It's a certificate your insurer files directly with the state to prove you are carrying the legally required liability coverage.

An SR-22 essentially brands you as a high-risk driver. The second you need one, you can expect your insurance premiums to skyrocket, often for several years.

This filing requirement becomes a long-term financial burden that sticks with you long after the initial fines are paid. It is Georgia's way of keeping you on a short leash to ensure your coverage doesn't lapse again. Between the fines, fees, and inflated insurance rates, driving without coverage is an incredibly costly mistake—one that can easily total many times more than a year's worth of premiums for the georgia minimum car insurance requirements.

Steps to Take After an Accident with an Uninsured Driver

It’s a gut-wrenching moment: you’ve just been hit, and the other driver has no insurance. Suddenly, the stress of the crash multiplies. You’re not just dealing with a damaged car and potential injuries; you're facing the very real possibility of paying for everything yourself. This is when the gaps in Georgia’s minimum car insurance requirements become painfully clear.

But don’t panic. Taking the right steps in the immediate aftermath can protect your legal rights and pave the way for a financial recovery.

First, focus on safety. If you can, move your vehicle out of traffic. Check on everyone involved and call 911 immediately. An official police report is non-negotiable in an uninsured motorist situation—it’s the primary piece of evidence that documents the other driver’s lack of insurance.

Document Everything at the Scene

While you wait for law enforcement, use your phone to become your own investigator. Your goal is to create a clear, undeniable record of what happened.

- Vehicle Damage: Take detailed photos of both cars from every angle. Capture close-ups of the impact points and wider shots showing the full extent of the damage.

- The Scene: Photograph the entire area. Include skid marks, traffic signals, stop signs, and the general road conditions.

- Driver Information: Even without an insurance card, get the other driver's name, phone number, and license plate. Take a picture of their driver's license if they'll allow it.

- Witnesses: If anyone stopped, politely ask for their name and contact information. A neutral third-party account can be invaluable for establishing fault.

Seek Medical Attention Immediately

Even if you think you’re fine, you need to be evaluated by a doctor. The adrenaline from a crash can easily mask serious injuries like whiplash or internal damage that won't show symptoms for hours or even days.

Getting prompt medical care does two important things: it protects your health and creates an official record linking your injuries directly to the accident. This is an important piece of evidence that insurance companies require when assessing a claim.

A delay in seeking treatment is one of the first things an insurance adjuster will use to argue that your injuries weren't caused by the crash. Protecting your health and your claim starts with that initial medical evaluation.

Notify Your Own Insurance Company

Once you are in a safe place, report the accident to your own insurance provider as soon as you can. State clearly that the at-fault driver is uninsured and that you need to open an Uninsured Motorist (UM) claim. This is exactly what that coverage is for.

Stick to the facts you documented at the scene. Avoid speculating about fault or downplaying your injuries. For a complete overview of the process, you can learn more about how to file a car accident claim in Atlanta on our site.

Before you accept any settlement, it is wise to speak with an attorney. Remember, even your own insurance company has a financial interest in minimizing payouts. An experienced lawyer on your side ensures you are treated fairly and receive the compensation you deserve—reinforcing why having more than just Georgia's minimum car insurance requirements is so vital.

Georgia Auto Insurance: Your Questions Answered

Understanding Georgia's insurance laws can feel overwhelming, but it doesn't have to be. Below are straightforward answers to the questions we hear most often from Atlanta drivers.

If I Cause a Wreck, Will the State Minimum Insurance Pay for My Car's Repairs?

No, and this is an important point that trips up many drivers. The Georgia minimum car insurance requirements only cover damages you cause to other people. Think of it as a shield for your assets, not a repair fund for your own vehicle.

To get your own car fixed after an accident you caused, you need Collision coverage. For other incidents like theft, hail damage, or a tree falling on your car, you'd need Comprehensive coverage. Both are optional but highly recommended.

Is Uninsured Motorist Coverage Required in Georgia?

It's not legally required, but Georgia law recognizes how important it is. Insurance companies are mandated to offer you Uninsured Motorist (UM) coverage when you buy a policy, and you must formally reject it in writing if you don't want it.

Given Georgia's high rate of uninsured drivers, declining UM coverage is a major gamble. It’s a small investment that protects you and your family if an uninsured driver hits you.

What Exactly Is an SR-22 Filing?

An SR-22 isn't insurance itself. Instead, it's a certificate your insurance provider files with the Georgia Department of Driver Services to prove you have active liability coverage.

You'll only need an SR-22 if you've been ordered to get one, typically after a serious violation like a DUI or driving without insurance led to a license suspension. The state will notify you directly by mail if you are required to have one to reinstate your driving privileges.

What If My Medical Bills Exceed the At-Fault Driver’s Policy Limit?

This is an unfortunately common scenario, especially with the state's low $25,000 per-person liability limit. If your medical expenses and lost income are higher than what the other driver’s policy will pay, you have two primary paths forward:

- Use Your Own Underinsured Motorist (UIM) Coverage: This is precisely what UIM is for. Your own policy steps in to cover the gap between your total damages and the at-fault driver's limit, up to your own policy's maximum.

- File a Lawsuit Against the At-Fault Driver: You can pursue the driver’s personal assets—like bank accounts, property, or other investments—to recover the remaining amount.

When your injuries are serious, dealing with the limitations of the Georgia minimum car insurance requirements becomes extremely challenging. Understanding your legal rights is essential to avoid being stuck with massive bills for an accident that wasn't your fault.

If you've been injured in an accident and are struggling with insurance companies or medical bills, you don't have to handle it alone. At Jamie Ballard Law, we provide a free case evaluation to help you understand your options and protect your rights. Visit our website at https://jamieballardlaw.com or call us to get the help you deserve.