After a crash with a drunk driver, the first question on everyone's mind is simple: who pays for all this? Dealing with the aftermath is stressful, and figuring out the financial side can be confusing. Many people ask, does insurance cover a DUI wreck? The short answer is yes. The drunk driver's mandatory liability insurance is specifically there to cover your medical bills and car repairs, up to their policy limits. But as with most things involving insurance, it’s not always that straightforward.

The Direct Answer to DUI Wreck Coverage

When an accident happens, insurance is supposed to be the financial backstop for the people who got hurt. In Georgia, every driver is legally required to carry liability insurance. Think of it as a safety net designed to protect innocent people from the financial fallout of another driver's bad decisions.

This means if an intoxicated driver hits you, their insurance company is on the hook for your losses. This coverage is typically broken down into two parts:

- Bodily Injury Liability: This is the part of the policy that pays for your medical care, any wages you lose from being out of work, and compensation for your pain and suffering.

- Property Damage Liability: This covers the cost to get your vehicle fixed or replaced, along with any other personal items that were destroyed in the collision.

Even when a DUI is involved, this core responsibility doesn't just vanish. The at-fault driver's insurance is still obligated to make the victim whole again, at least from a financial standpoint.

What About the Drunk Driver's Own Car?

While the drunk driver's insurance is set up to protect you, their own situation is a completely different story. Coverage for their own vehicle falls under their collision coverage, which is an optional add-on.

This is where things get tricky for them. Many insurance policies include what's known as a "criminal acts" or "intentional acts" exclusion. The insurer can—and often will—argue that since driving drunk is a deliberate criminal act, they don't have to pay for the at-fault driver's car repairs.

For the innocent victim, the at-fault driver's liability coverage is almost always secure. For the driver who caused the crash, however, a DUI can spark a major dispute with their own insurance company, often leaving them to pay for their car repairs entirely out-of-pocket.

To make this clearer, here's a quick breakdown of how different policies come into play after a DUI-related crash in Georgia.

Quick Guide to Insurance Coverage After a DUI Wreck

This table shows which insurance policy typically handles different damages following a crash caused by an intoxicated driver in Georgia.

| Type of Damage | Who It Typically Covers | Important Considerations |

|---|---|---|

| Victim's Medical Bills | At-Fault Driver's Bodily Injury Liability | Your own health insurance or Uninsured Motorist coverage may also apply. |

| Victim's Vehicle Repairs | At-Fault Driver's Property Damage Liability | You can also use your own collision coverage and have your insurer subrogate. |

| Drunk Driver's Medical Bills | Their Own Health Insurance or MedPay | Liability insurance from their auto policy will not cover their own injuries. |

| Drunk Driver's Vehicle Repairs | Their Own Collision Coverage (Maybe) | The claim is often denied due to a "criminal acts" exclusion in the policy. |

Understanding these distinctions is key to the claims process and ensuring you're looking to the right policy for payment.

The Impact on the Claims Process

A DUI conviction changes an already stressful claims process. While the at-fault driver's insurer is obligated to pay, their goal is always to pay as little as possible. The DUI charge gives you powerful, undeniable proof of the other driver's negligence, which massively strengthens your claim.

But it also puts the insurance adjuster on high alert. They will scrutinize every single detail of your case, from the extent of your injuries to the value of your damaged property. This is why knowing your rights from the very start is so important.

In short, the answer to "does insurance cover a DUI wreck" is a firm yes for the victim. But the DUI itself guarantees that the journey to getting fair compensation will be a more intense and challenging one.

How Liability Insurance Responds to a DUI Accident

After you've been hit by an intoxicated driver, their liability insurance is the primary source for your financial recovery. Understanding how this coverage works is the first step toward getting your life back on track. So, does insurance cover a DUI wreck? The answer starts with the at-fault driver's policy.

In Georgia, every single driver is required by law to carry liability insurance. This isn't just a suggestion; it’s a legal mandate designed to protect innocent people. Think of it like a financial firewall. The at-fault driver’s poor decision shouldn’t burn down your financial stability, and their liability policy is there to contain the damage.

This mandatory coverage is made up of two distinct parts that address different types of losses.

The Two Pillars of Liability Coverage

When you file a claim against the drunk driver's policy, you are seeking compensation from two specific types of coverage:

- Bodily Injury (BI) Liability: This is the portion of the policy that pays for the human cost of the accident. It covers your emergency room visit, follow-up doctor appointments, physical therapy, prescription medications, and any other medical care you need. It also compensates you for income you’ve lost if your injuries keep you from working.

- Property Damage (PD) Liability: This part pays for the physical damage to your property. Most commonly, this means the full cost to repair your vehicle. If the car is declared a total loss, this coverage pays for its fair market value so you can replace it.

These two coverages are the foundation of any claim filed against an at-fault drunk driver. You can learn more about the specifics of handling these types of cases by reviewing information on personal injury claims.

The Problem of Policy Limits

While liability insurance is required, it has its boundaries. Every policy has a policy limit, which is the absolute maximum amount the insurance company will pay out for a single accident.

For example, a driver might have a policy that covers $25,000 for bodily injury per person and $25,000 for property damage. If your medical bills are $40,000 and your car repairs cost $15,000, the insurer will only pay up to those limits, leaving a significant shortfall.

This is a very common issue, especially in accidents involving serious injuries where medical costs can quickly escalate. When your expenses exceed the at-fault driver's policy limits, you may need to explore other options for recovery, like your own Uninsured/Underinsured Motorist (UM/UIM) coverage.

Even with clear evidence like a DUI arrest, remember that the at-fault driver’s insurance provider is a business. Their main objective is to protect their bottom line by minimizing what they pay out. They will still require extensive documentation for every expense and will not make the process easy. Understanding these basics—how liability coverage works and its limits—is your first move in securing a fair outcome.

What a DUI Means for the At-Fault Driver's Insurance

For the driver who caused the accident, a DUI conviction is far more than a legal headache. It's a financial catastrophe waiting to happen. To an insurance company, a DUI isn't just another mark on your record; it's a massive red flag signaling extreme risk.

That single event sets off a chain reaction of expensive, long-term consequences that completely rewires the relationship between the driver and their insurer. The question, "does insurance cover a DUI wreck?" gets a lot more complicated when you're the one at fault.

The first and most immediate hit is a huge spike in insurance premiums. Across the United States, drivers with a new DUI conviction can expect their rates to jump by an average of 60% or more compared to someone with a clean record.

Long-Term Financial Consequences

The pain doesn't stop with higher monthly bills. Insurance companies will often take more severe steps to protect themselves from the new, higher risk you represent.

These actions frequently include:

- Policy Non-Renewal: When your current policy is up, your insurer may simply refuse to offer you a new one. This forces you back into the market, now labeled as a high-risk driver.

- Outright Cancellation: Depending on the policy's fine print and the specifics of the offense, some insurers have the right to cancel your coverage right in the middle of the term.

- SR-22 Requirement: The state of Georgia will almost certainly require you to file an SR-22 form. This isn't insurance itself, but a certificate your insurer files to prove you have the state-mandated minimum liability coverage. You'll have to maintain this for several years, effectively branding you as high-risk to any carrier you approach.

A DUI conviction fundamentally changes how insurers see you. You're no longer an average driver but a significant liability, triggering financial penalties that can follow you for years.

Coverage for the At-Fault Driver's Own Vehicle

So, what about the damage to the drunk driver's own car? While their liability policy is on the hook for the victim's damages, their own collision coverage is another story entirely.

Many insurance policies include a "criminal acts" exclusion clause. Insurers will often point to this clause to deny a claim, arguing that because driving under the influence is an illegal act, they have no obligation to pay for the at-fault driver's vehicle repairs.

Understanding the full scope of these consequences is important. It’s important to research the impact of points on insurance premiums, as a DUI conviction adds significant points to your license. Anyone facing these charges should also understand the legal road ahead, which is where an Atlanta drunk driving accident lawyer becomes essential.

While insurance may cover the victim's damages after a DUI wreck, the driver who caused it is left facing a very steep and difficult climb back to normalcy.

Getting to the Bottom of Policy Exclusions in a DUI Claim

When you buy car insurance, you're essentially buying a promise—a promise of financial backup if something goes wrong. But every policy comes with fine print, and that fine print contains exclusions. These are the specific situations where the insurance company won't pay a claim.

And when it comes to a DUI wreck, those exclusions are everything, especially for the driver who caused the crash.

Insurance companies are in the business of managing risk. A DUI is a massive, unpredictable risk they don't want to cover. To protect themselves, they rely on a couple of key clauses to deny claims: the "criminal acts" or "intentional acts" exclusions.

At first, that might sound strange. A car wreck is an accident, isn't it? Well, not in the eyes of an insurance carrier.

The "Criminal Acts" Exclusion: Why It Matters

From the insurer's point of view, the decision to drive while intoxicated isn't an "accident." They see it as a deliberate, willful criminal act. Because of that, they can argue that their policy doesn't have to cover the at-fault driver's own damages under their collision or comprehensive coverage.

What does that look like in the real world? It means if a drunk driver totals their own car, the insurance company can legally walk away. They are left holding the bag for the entire cost of a new vehicle. Many policies are written with specific language that reduces or outright eliminates coverage for any crash where the driver was intoxicated, because it's seen as such an extreme form of negligence. You can get more information on how a DUI affects insurance claims at mitchellhoffmanwolf.com.

A Note for Victims: These exclusions are almost always aimed squarely at the person who caused the wreck. State laws, including here in Georgia, are designed to protect innocent people. An insurer generally cannot use a "criminal acts" clause to get out of paying for your medical bills or vehicle repairs under the at-fault driver's liability policy.

What About Punitive Damages?

Another place where exclusions pop up is with punitive damages. These aren't meant to pay you back for a specific loss, like a hospital bill. Instead, they are awarded by a court to punish the defendant for truly outrageous behavior and send a message.

- What are they? A financial penalty designed to punish extreme recklessness.

- Why they matter in DUI cases: Drunk driving is a textbook example of the kind of conduct that justifies punitive damages.

- The insurance problem: Most insurance policies explicitly exclude coverage for punitive damages. This means the insurer will pay for compensatory damages (like medical bills and lost wages) but not the punishment part of the court's award.

This leaves the drunk driver personally on the hook for any punitive damages awarded. They have to pay that amount out of their own pocket. Understanding how these exclusions work is vital for setting realistic expectations after a crash. Knowing whether insurance covers a DUI wreck really depends on who you are in the accident and what kind of damages you're trying to recover.

Your Options When the Drunk Driver Is Uninsured

It's a nightmare scenario, but one that plays out on Atlanta roads far too often: the drunk driver who hit you either has no insurance at all or carries a policy so minimal it won't even scratch the surface of your medical bills. So, does insurance cover a DUI wreck when the at-fault driver is uninsured? The answer, thankfully, often lies within your own policy.

This is precisely why we stress the importance of Uninsured/Underinsured Motorist (UM/UIM) coverage. This is a specific part of your auto insurance that you buy to protect yourself when the other driver can't pay. Think of it as a financial safety net for the worst-case scenario.

When a drunk driver is uninsured, your UM coverage can step in to pay for your medical bills, lost income, and even your pain and suffering—exactly what the at-fault driver's liability insurance should have done. If they're underinsured (meaning their policy limits are too low to cover everything), your UIM coverage is there to bridge the gap.

Your First Lines of Financial Defense

When you're reeling from a crash like this, knowing where to turn for immediate financial help is important. Acting quickly can protect both your physical and financial well-being.

- Uninsured/Underinsured Motorist (UM/UIM) Coverage: This is your primary resource. You'll need to open a claim directly with your own insurance company.

- Medical Payments (MedPay) Coverage: If you carry this optional coverage on your auto policy, it can start paying your initial medical bills right away, regardless of who was at fault.

- Personal Health Insurance: Don't forget about your own health insurance. It can cover your medical treatments while all the car insurance details get sorted out.

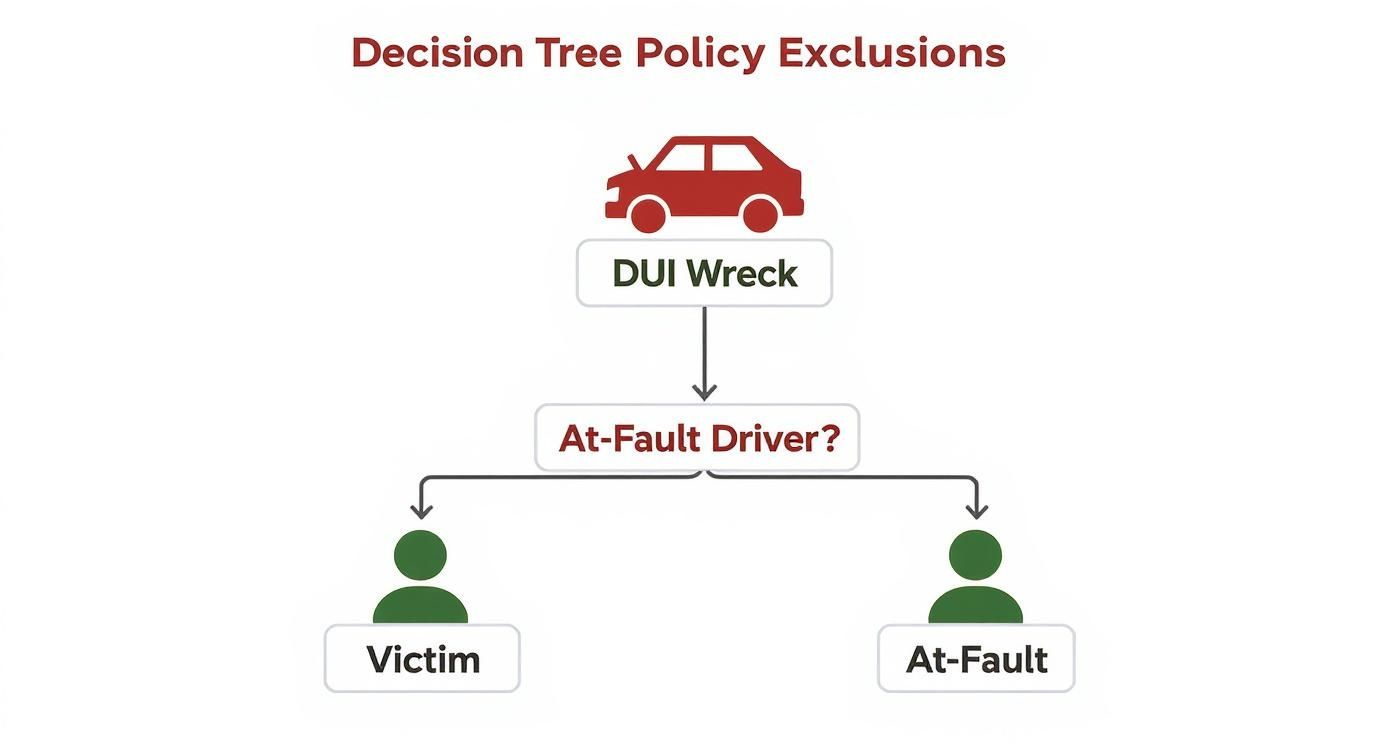

This decision tree shows how an insurance claim can unfold after a DUI crash, highlighting the different paths available.

As you can see, while the at-fault driver's own claims might be denied, victims have several avenues to pursue the compensation they need.

Looking Beyond Insurance Policies

What if your UM/UIM coverage isn't enough, or worse, you don't have it? You still have another powerful option: filing a personal injury lawsuit directly against the drunk driver. This legal action allows you to seek compensation from their personal assets, like savings, property, or investments. Filing a claim against an uninsured driver requires a specific strategy, and you can learn more about how to file a car accident claim in Atlanta.

A lawsuit can be a more involved process, but it's often the only way to get the full compensation you deserve when an uninsured drunk driver turns your life upside down. Rest assured, Georgia law is on your side.

Because victims are so vulnerable in these situations, we strongly advise every Georgia driver to carry as much UM/UIM coverage as they can comfortably afford. It is truly one of the best financial protections you can give yourself and your family. The bottom line is that you have options, even in a worst-case scenario where a drunk driver's insurance can't cover the wreck they caused.

Why a DUI Accident Claim Is Taken So Seriously

When you ask, "does insurance cover a DUI wreck," it's important to understand the larger picture. Insurers and the legal system don't see a simple fender-bender. They see an incident with a devastating potential for human harm, which is why the scrutiny applied to these claims is so intense.

This isn't just a local problem; it's a global crisis. Alcohol-related road fatalities number around 273,000 worldwide every single year. Here in the United States, the impact is just as staggering. Roughly 30% of all fatal traffic crashes involve a driver impaired by alcohol.

That translated to approximately 12,429 deaths in 2023—about 34 lives lost every day. You can find more of this data directly on the NHTSA’s official drunk driving prevention page.

The Human Cost Behind the Statistics

These aren't just numbers on a page. They explain why insurance companies react so forcefully to a DUI. This isn't a minor traffic violation; it's a high-stakes gamble with people's lives. When an insurer sees a DUI on a driving record, they see a pattern of behavior statistically proven to lead to catastrophic outcomes.

This is exactly why premiums skyrocket after a conviction and why claims involving a DUI are investigated with such rigor. The increased risk isn't a guess—it's backed by decades of data linking impaired driving to severe, often fatal, accidents.

The screenshot below from the National Highway Traffic Safety Administration (NHTSA) drives home the deadly reality of this choice.

The data is clear: someone is killed in a drunk-driving crash every 45 minutes in the United States. This fact alone underscores the constant and predictable danger that impaired drivers create on our roads.

The seriousness of a DUI claim is a direct reflection of the potential for tragedy. It is the reason why Georgia law provides strong protections for victims and imposes severe penalties on those who drive impaired.

This shared understanding of the human cost is precisely why our legal and insurance systems are built to respond so forcefully. The goal is to hold at-fault drivers accountable and ensure victims have a clear path to recovery—reinforcing just how important it is to know if your insurance covers a DUI wreck.

Common Questions About DUI Accident Claims

When you've been hit by a drunk driver, your mind is probably racing with questions. Getting clear, straightforward answers is the first step toward understanding your rights and what comes next. Let's tackle some of the most common concerns we hear from victims trying to figure out if insurance covers a DUI wreck.

Will My Own Insurance Rates Go Up?

This is a huge worry for a lot of people, but you can set your mind at ease. If you were not at fault for the crash, your insurance company should not raise your premiums.

This holds true whether you file a claim against the at-fault driver's liability policy or you need to use your own Uninsured Motorist (UM) coverage. Georgia law is designed to protect innocent drivers from being penalized for accidents they didn't cause.

Can I Sue the Drunk Driver Personally?

Yes, absolutely. An insurance claim and a personal injury lawsuit are two completely different legal actions, and you have the right to pursue both.

A lawsuit is often the only way to get full compensation if the drunk driver's insurance policy isn't large enough to cover all of your medical bills, lost wages, and other damages. It's also the primary path for seeking punitive damages, which are intended to punish the driver for their shockingly reckless behavior and deter others from doing the same.

Just be aware that there are strict deadlines for filing a lawsuit. You can learn more about the statute of limitations for personal injury in GA to make sure you don't lose your right to sue.

In Georgia, a DUI injury case is one of the clearest examples where punitive damages can be awarded. This is because getting behind the wheel while intoxicated shows a willful and conscious disregard for the safety of everyone else on the road.

Unlike almost any other type of personal injury case, there is often no cap on punitive damages in Georgia for DUI accidents. This is a very important factor when deciding whether to file a lawsuit, as it provides a powerful way to hold the drunk driver fully accountable for their actions. Understanding if insurance does cover a DUI wreck is the starting point, but knowing all your legal options is what truly matters.