Understanding what an auto accident settlement involves is the first step toward getting your life back on track after a crash. It's a formal agreement between you and the at-fault driver's insurance company that resolves your claim and helps you avoid a long court battle. This isn't about getting a windfall; it's about securing the financial support you need to cover your losses and move forward.

What Your Settlement Is Meant to Accomplish

After the initial shock of a car wreck wears off, the pressure from medical bills and missed paychecks can be immense. A settlement’s main job is to provide you with compensation that makes you "whole" again, at least from a financial standpoint. It’s the method we use to get the resources you need to handle the aftermath of the collision.

The entire settlement process is built on the legal idea of damages—a term for the specific, measurable losses you've gone through. These damages are the building blocks of your claim and what a fair settlement should cover. Instead of a drawn-out, unpredictable trial, a settlement offers a more direct path to getting things resolved.

Statistically, only about 4% of personal injury claims ever make it to a trial courtroom. The vast majority are resolved through settlement agreements, as both sides often prefer to avoid the time, cost, and uncertainty of litigation.

Why Settling Is Often the Practical Choice

Choosing to settle is about regaining control. A court case can drag on for years, leaving your future uncertain. A settlement provides a definite outcome, allowing you to move forward much sooner.

To give you a clearer picture, let's break down the main elements that make up a typical settlement package.

Key Components of Your Settlement

| Component | What It Covers |

|---|---|

| Medical Expenses | This covers everything from the initial ER visit to surgery, physical therapy, and any future medical care you might need. |

| Lost Income | This reimburses you for the wages you lost while out of work and for any diminished ability to earn in the future. |

| Pain and Suffering | This is compensation for the physical pain, emotional distress, and disruption the accident caused in your daily life. |

| Property Damage | This pays for the repair or replacement of your vehicle and any other personal property that was damaged in the crash. |

Ultimately, the goal is to secure a fair amount that reflects the full scope of your experience. Understanding the basics of what a personal injury claim entails can give you a clearer picture of how these elements come together. A fair auto accident settlement is your pathway to financial recovery.

How Your Settlement Amount Is Calculated

Figuring out the value of an auto accident settlement isn't just guesswork. It's a careful process of identifying and adding up every single loss you've suffered. In legal terms, we call these losses "damages."

Insurance adjusters group these damages into specific categories. Understanding how they work is the first step toward knowing what your claim is truly worth. The two main categories are economic and non-economic damages, and each one is vital to the final calculation.

The Foundation: Economic Damages

Economic damages are the most straightforward part of your claim because they have a clear, verifiable dollar value. Think of them as the hard numbers—the tangible costs that are backed up by bills, receipts, and pay stubs. They form the financial foundation of your settlement.

These costs typically include:

- Past and Future Medical Bills: This covers everything from the ambulance ride and ER visit to surgery, physical therapy, medication, and any ongoing care you'll need for your recovery.

- Lost Wages and Income: If you couldn't work while recovering, this reimburses you for that lost income. It also accounts for any diminished future earning capacity if your injuries permanently affect your ability to do your job.

- Property Damage: This is the cost to repair or replace your vehicle. For severe accidents, the cost of major vehicle work, like specialized engine repair services, can significantly impact this part of your claim.

As your attorney, I would meticulously document every single expense to build the strongest possible foundation for your case.

Valuing the Human Cost: Non-Economic Damages

While economic damages cover the measurable financial toll, non-economic damages address the intangible, human side of the accident. These losses are just as real and often more devastating, but they don't come with a neat price tag. This is where having a skilled attorney becomes so important.

Non-economic damages provide compensation for:

- Pain and Suffering: This accounts for the physical pain, chronic discomfort, and overall suffering you have endured because of your injuries.

- Emotional Distress: A serious wreck often leaves deep psychological scars, including anxiety, depression, a fear of driving, or post-traumatic stress disorder (PTSD).

- Loss of Enjoyment of Life: This compensates you for the inability to participate in hobbies, activities, or daily routines that brought you joy before the collision.

To calculate non-economic damages, insurers often use a "multiplier" method. They take your total economic damages and multiply that amount by a number, typically between 1.5 and 5, depending on the severity of your injuries and their long-term impact on your life.

This is why simply adding up your medical bills is never enough. It completely fails to capture the full story of how an accident has upended your life. While there are many legal terms involved, you can explore our legal dictionary to better understand the language used in personal injury cases.

Putting It All Together for a Fair Offer

Once both economic and non-economic damages are calculated, they are combined to establish a total settlement value. This figure serves as the baseline for negotiations with the insurance company. It is important to remember that every case is unique.

While figures vary widely, some data suggests the average settlement for an injury-related car accident is around $30,416, with the median closer to $25,000. These numbers show that while catastrophic injuries can lead to six-figure settlements, most cases involve more modest recoveries.

A complete and accurate calculation of all your damages is the single most important factor in securing a fair auto accident settlement.

The Typical Timeline From Accident to Payout

When you're recovering from a car wreck, the last thing you need is more uncertainty. One of the first questions we always get is, "How long will my auto accident settlement actually take?" While no two cases are identical, the process follows a predictable path.

Think of it less like waiting and more like building. Each stage is a necessary step, laying the foundation for a strong claim. It all starts at the scene of the accident, and from there, we move through a structured process to document every loss and fight for the compensation you deserve. Knowing the roadmap can help you manage expectations during a very unpredictable time.

The Immediate Aftermath and Investigation

The first 24 to 72 hours after a collision are so important. Your top priorities are getting medical attention—even if you feel fine—and calling the police to file a report. These two actions create the initial cornerstones of your case: official medical records and a formal police report.

Once you’re safe, the investigation kicks into high gear. This is where we gather the hard evidence needed to prove what happened and who was at fault.

This phase usually involves:

- Collecting Official Reports: We secure the full police report and any records from first responders.

- Speaking with Witnesses: We contact anyone who saw the crash to get their statements while the memory is still clear.

- Documenting the Scene: This includes photos of vehicle damage, skid marks, road conditions, and any relevant traffic signals or signs.

Treatment and Reaching Maximum Medical Improvement

After the initial fact-finding, the focus shifts to what matters most: your health. This is often the longest and most unpredictable part of the timeline, as it’s dictated entirely by the seriousness of your injuries. Your job is to follow your doctor’s orders, attend every appointment, and focus on getting better.

It’s absolutely essential not to settle your case too early. We can't even begin to negotiate a fair settlement until we know the full extent of your injuries and your long-term prognosis. The key milestone we're waiting for is called Maximum Medical Improvement, or MMI.

MMI is the point where your medical condition has stabilized and is not expected to improve any further with treatment. This doesn't always mean you're 100% recovered, but it gives us a clear picture of your future medical needs, potential long-term limitations, and the total cost of your care.

Once you hit MMI, we can gather every medical bill and record to calculate the true value of your claim.

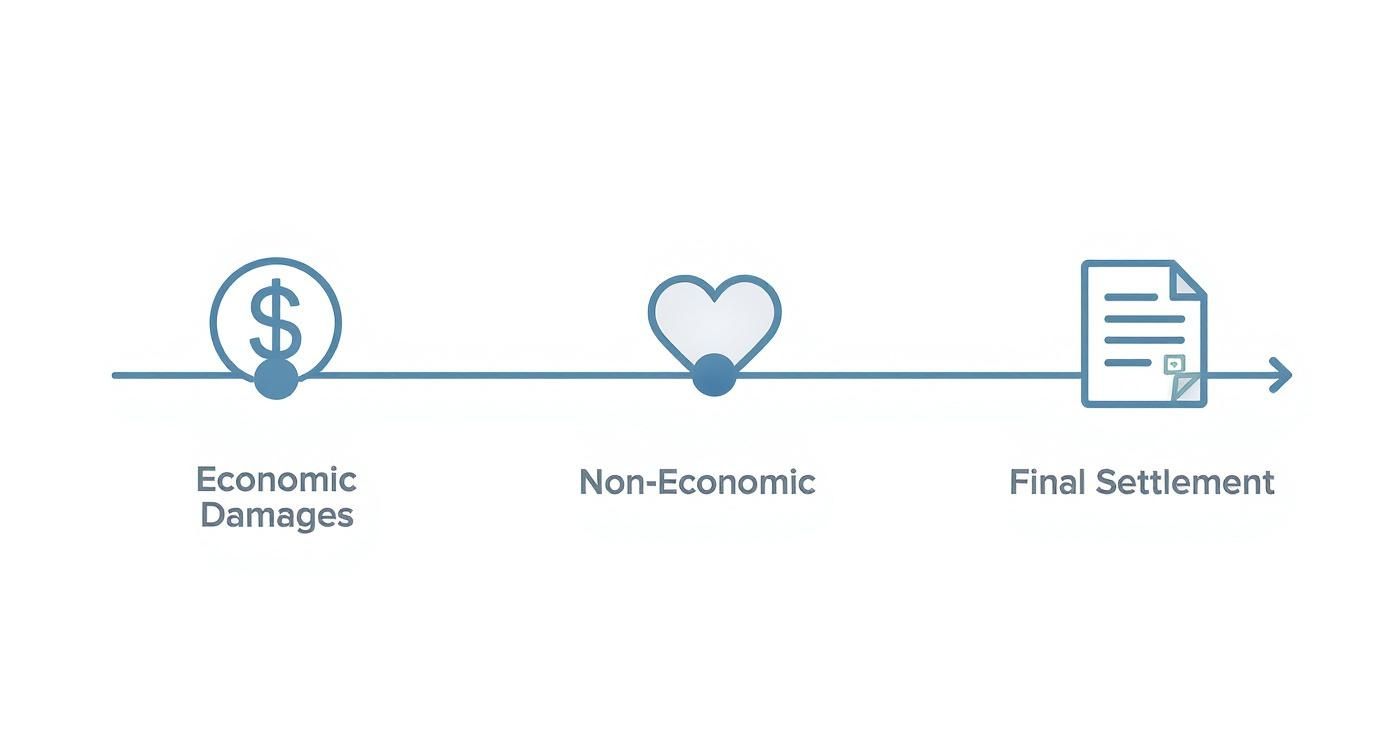

This infographic shows how we organize those damages to build your settlement demand.

As you can see, the final number is a combination of tangible financial losses (economic damages) and the very real human cost of the crash (non-economic damages).

Demand, Negotiation, and Final Payout

With a complete picture of your damages, we draft a formal demand letter and send it to the at-fault driver's insurance company. This document lays out the facts, proves liability, and provides a detailed breakdown of your losses, demanding a specific settlement amount.

The insurance adjuster will respond with an initial offer. Be prepared: it’s almost always a lowball number. This is where the real work begins. The negotiation phase can involve several rounds of offers and counteroffers over a few weeks or even several months.

Once we reach a number you agree with, the final steps happen quickly. You’ll sign a release form, which officially closes the claim. The insurance company processes the paperwork and issues the check for your auto accident settlement.

Georgia Laws That Will Affect Your Claim

When you're pursuing an auto accident settlement in Georgia, the final outcome isn't just about the facts of the crash. Our state has a specific rulebook that governs your claim, and these laws influence everything from how long you have to file a lawsuit to how much money you can actually recover. Getting familiar with these rules is a must.

While every case has its own unique details, three Georgia laws almost always play a major role: the statute of limitations, the comparative negligence rule, and the state's minimum insurance requirements. Each one can drastically change the value and direction of your settlement.

The Clock Is Ticking: The Statute of Limitations

One of the most unforgiving rules in personal injury law is the statute of limitations. Here in Georgia, you typically have just two years from the date of the accident to file a lawsuit. If you let that deadline pass, your right to seek compensation is likely gone for good, no matter how strong your case might be.

This two-year window is incredibly strict and has very few exceptions. It exists to make sure evidence is still fresh and that disputes get resolved promptly. To get a deeper look at this important deadline, we break it all down in our article on the [statute of limitations for personal injury in GA](https://jamieballardlaw.com/statute-of- limitations-for-personal-injury-ga/).

Modified Comparative Negligence: What It Means for You

Georgia follows a legal doctrine known as modified comparative negligence. This rule is a huge factor in calculating your settlement, especially if the insurance company tries to argue you were partially responsible for the crash.

Here’s the bottom line: you can recover damages as long as a court finds you less than 50% at fault. If your share of the blame hits 50% or more, you are legally barred from recovering a single penny. If you are less than 50% to blame, your final award is simply reduced by your percentage of fault.

For example: Let's say your total damages add up to $100,000, but a jury decides you were 10% responsible for what happened. Under Georgia's rule, your $100,000 recovery would be cut by 10%, leaving you with a maximum of $90,000.

Because of this rule, building a rock-solid case that minimizes any fault on your part is absolutely essential.

How Georgia's Comparative Negligence Rule Works

This table shows exactly how your share of fault can directly reduce your financial recovery.

| Your Percentage of Fault | Total Damages | Your Final Recovery Amount |

|---|---|---|

| 0% (Not at fault) | $100,000 | $100,000 (Full amount) |

| 10% | $100,000 | $90,000 (Reduced by 10%) |

| 25% | $100,000 | $75,000 (Reduced by 25%) |

| 49% | $100,000 | $51,000 (Reduced by 49%) |

| 50% or more | $100,000 | $0 (Recovery is barred) |

As you can see, every percentage point of fault assigned to you matters, making it essential to fight back against any unfair blame.

State Minimum Insurance Requirements

There's also a practical limit to what you can recover: the amount of insurance coverage available. Georgia law mandates that every driver must carry a minimum level of liability insurance.

The current minimums are:

- $25,000 for bodily injury liability per person.

- $50,000 for bodily injury liability per accident.

- $25,000 for property damage liability per accident.

Frankly, these amounts are often nowhere near enough to cover the medical bills and lost wages from a serious injury. If the at-fault driver only has this basic coverage, it can put a hard cap on what you can get from their policy. This is precisely why it's so important to have your own Uninsured/Underinsured Motorist (UM/UIM) coverage.

These Georgia laws create the legal landscape for every negotiation we undertake. Understanding how they apply to your case is the first step toward securing the fair auto accident settlement you deserve.

Dealing With Insurance Adjusters and Red Flags to Watch For

After a crash, it won’t be long before you get a call from the other driver’s insurance adjuster. This is where the negotiation for your auto accident settlement officially begins, and you need to understand exactly who you’re talking to. The adjuster is a trained professional, and their primary job is simple: protect their company's profits by paying you as little as possible.

While most adjusters are polite and professional, their goal is the exact opposite of yours. They aren’t there to make sure you have what you need to fully recover. They are there to close your claim for the lowest cost to their employer. That’s why every single word in your conversations with them matters.

Common Tactics Adjusters Use

Insurance adjusters don't just make things up as they go; they use a playbook of proven tactics designed to lower the value of your claim. Knowing these strategies is your first line of defense against mistakes that could cost you dearly.

One of the first things they'll ask for is a recorded statement. They'll frame it as a routine step, just a way to "get your side of the story." In reality, their goal is to get you on record saying something they can twist against you later—maybe you downplay your injuries or accidentally say something that sounds like you're admitting fault. You are under no legal obligation to provide one.

Another favorite is the quick, lowball offer. An adjuster might call within days of the accident, offering a check that seems like a fast and easy solution. It’s tempting, especially with medical bills showing up. But it's a trap. Once you accept that offer, you sign away your right to seek any more compensation, even if you find out weeks later your injuries are far more serious than you first realized.

Red Flags to Watch For in Your Conversations

You need to recognize when an adjuster’s behavior shifts from standard negotiation to something more predatory. These red flags are clear signals that you need professional legal help to level the playing field.

Be extremely cautious if an insurance adjuster tries to talk you out of hiring an attorney. This is one of the biggest red flags you can get. They'll say a lawyer will just complicate things or take a huge cut of your money. What they really mean is that an experienced attorney makes it impossible for them to underpay your claim.

Here are a few specific warning signs to look for:

- Rushing You to Settle: They push you to accept an offer before your medical treatment is complete or before you even know the full extent of your injuries and future needs.

- Unexplained Delays: The adjuster goes silent, stops returning your calls, or drags their feet processing your claim without giving you a legitimate reason.

- Misrepresenting the Policy: They tell you that certain damages, like pain and suffering, aren't covered by the at-fault driver's policy when they actually are. For official guidance, you can always consult the Georgia Office of Insurance and Safety Fire Commissioner.

- Requesting Full Access to Medical Records: The insurance company only has a right to see medical records directly related to the accident. A demand for your entire medical history is usually a fishing expedition to find a pre-existing condition they can blame for your pain.

If you spot any of these tactics, it’s a clear sign the insurance company is not acting in good faith. Your top priority should be protecting your right to a fair auto accident settlement.

When to Partner With an Atlanta Car Accident Attorney

You might be wondering if you really need a lawyer for your auto accident settlement. For a minor fender-bender with no injuries, you can probably handle the claim yourself. But when you’ve been seriously hurt, the stakes get much higher, and partnering with an experienced attorney can make all the difference.

This isn’t about being aggressive; it’s about leveling the playing field. Insurance companies have vast resources and teams of lawyers dedicated to protecting their bottom line. An attorney ensures your rights are protected from day one.

The Value an Attorney Brings to Your Claim

From the moment you hire an attorney, you get a shield. We immediately take over all communications with insurance companies. No more calls from adjusters trying to get a recorded statement or pressure you into a quick, lowball offer. This lets you focus on what's most important: your recovery.

An attorney also brings investigative resources to your case. We work to:

- Gather Important Evidence: We secure the official police report, track down witness statements, and obtain any available traffic camera footage.

- Hire Necessary Experts: For serious crashes, we may bring in accident reconstruction specialists to prove how the collision occurred or medical experts to testify about your long-term care needs.

- Accurately Value Your Claim: This is perhaps our most important role. We know how to calculate the full scope of your damages—not just current medical bills, but future ones, too. We also know how to place a fair value on your pain and suffering, which is often the largest part of a settlement.

An attorney’s involvement sends a clear message to the insurance company: you are serious about your claim and will not be taken advantage of. This simple fact often encourages adjusters to negotiate in good faith and offer a more reasonable settlement from the start.

Managing the Legal Process for You

Beyond the investigation, we manage every detail of the claim. This involves preparing and submitting a comprehensive demand package that tells your story and documents every single loss. We then handle all the back-and-forth negotiations, fighting to get you the best possible outcome.

If a fair settlement cannot be reached, we are prepared to take the next step. Understanding the car accident lawsuit process in Atlanta can provide peace of mind, knowing you have a dedicated advocate ready to fight for you in court if necessary.

Ultimately, our goal is to make sure you have the financial resources needed to rebuild your life. Partnering with a skilled Atlanta attorney ensures you have a professional on your side, working tirelessly to secure a comprehensive auto accident settlement.

Common Questions About Auto Accident Settlements

Here are clear, direct answers to some of the most common questions we hear from people going through the process of an auto accident settlement. We hope this provides helpful insight as you plan your next steps.

How Long Does an Auto Accident Settlement Take?

This is the number one question on everyone’s mind, and the honest answer is: it depends. A straightforward case with minor injuries and clear fault might settle in just a few months. However, most cases take longer.

The process of reaching a settlement can take anywhere from six months to three years, with more involved cases involving shared fault or disputed liability often taking longer to resolve. In Florida, for example, recent settlements have ranged from $50,000 to $6.1 million, reflecting the wide variation in outcomes based on the specific circumstances of each case. You can discover more about settlement examples to see how diverse these cases can be.

Do I Have to Pay Taxes on My Settlement Money?

This is another common concern, and the news is generally good. According to the IRS, compensation you receive for physical injuries or sickness is not considered taxable income. This means the portion of your settlement that covers medical bills, lost wages, and pain and suffering is typically tax-free.

However, there are a few exceptions:

- Punitive Damages: If you are awarded punitive damages (meant to punish the at-fault party), that portion of the settlement is taxable.

- Interest on the Settlement: Any interest that accrues on the settlement amount may also be subject to taxes.

For specific advice, it's always wise to consult the official IRS guidelines or speak with a tax professional.

Is the First Settlement Offer Usually Fair?

Almost never. The first offer from an insurance adjuster is a starting point for negotiations, and it's intentionally low. The adjuster's job is to resolve your claim for the least amount of money possible for their company.

Accepting the first offer is one of the biggest mistakes you can make. It's often made before you even know the full extent of your injuries or future medical needs. Never feel pressured to accept a quick payout.

It's a clear sign that the insurance company is trying to close your case cheaply and quickly. A fair negotiation takes time and requires a full understanding of all your damages. It’s about ensuring the final number truly reflects what you’ve lost. The goal is to secure an auto accident settlement that provides for your complete recovery.

At Jamie Ballard Law, we believe everyone deserves a fair chance at justice and a full recovery. If you have questions about your case or need help understanding your options, we're here to provide clarity and support. Contact us for a free, no-obligation case evaluation today. https://jamieballardlaw.com