After you’ve been through an injury, getting a settlement should feel like the finish line. But then you hear from Medicare, and a new worry pops up: how much will Medicare take from my settlement? It’s a question we hear all the time from our clients here in Atlanta.

There’s no flat percentage. The amount Medicare needs to be repaid is tied directly to the medical bills they covered for your accident-related injuries. This guide will help you understand the process.

Understanding Medicare's Claim On Your Settlement

As Atlanta personal injury attorneys, we see this question cause a lot of stress. Our goal is to make the process clear and predictable for you.

When you're hurt, Medicare often steps in to cover your medical costs immediately. This ensures you get the care you need without having to wait for the at-fault party’s insurance to pay up.

Think of it as Medicare fronting the cost of your treatment. The settlement you receive from the responsible party is meant to cover those exact medical expenses, plus other damages like lost wages and pain and suffering.

Why Does This Happen?

The legal foundation for this is the Medicare Secondary Payer Act. This federal law makes it clear that if another party is responsible for your medical bills, their insurance is the "primary payer." Medicare is only supposed to be the "secondary payer."

Because resolving personal injury claims in Georgia can take months or even years, Medicare makes what are called "conditional payments" for your care. They are "conditional" because they are made on the condition that Medicare will be reimbursed if you later receive a settlement.

This right to get paid back creates a legal claim against your settlement funds, often called a "Medicare lien." It isn't a penalty—it's just the government’s way of recovering taxpayer money when another party was financially responsible for the bills.

This system makes sure Medicare’s funds are preserved for everyone who needs them. To learn more about Medicare's structure and enrollment, you might find an essential Medicare planning guide helpful.

Knowing these rules is the first step toward protecting your settlement. We'll walk you through exactly what to expect so you can feel prepared and understand exactly how much Medicare will take from your settlement.

Why Medicare Has a Right to Your Settlement Funds

It’s often a shock when clients learn that a government program like Medicare has a claim on their personal injury money. This whole process comes from a federal law called the Medicare Secondary Payer (MSP) act. The rule is actually pretty straightforward: if another party is responsible for your medical bills—like the at-fault driver's insurance—they are considered the "primary payer."

Medicare, by design, is supposed to be the "secondary payer." But since personal injury cases here in Georgia can drag on, Medicare often steps in to pay for your medical care right away. This is a good thing, as it ensures you get the treatment you need without waiting for your case to settle.

These payments are officially known as "conditional payments." They are made on the condition that Medicare gets reimbursed if and when you receive a settlement or judgment from the party who caused your injuries.

The Basis of the Medicare Lien

This right to be paid back creates a legal claim against your settlement, which everyone calls a "Medicare lien." It’s important to understand this isn't some kind of penalty. It’s simply the government's way of recovering taxpayer money when another party was ultimately responsible for the injuries that led to your medical bills.

Think of it like this: You borrow money from a friend to fix your car after an accident, promising to pay them back once the other driver's insurance check comes in. When you get the settlement, it includes money for those repairs, so you pay your friend back as promised. Medicare's system works in a very similar way.

The official Medicare website explains how it works with other types of coverage.

This visual from Medicare.gov shows that in liability claims, the other insurance is primary. Understanding this pecking order is the key to seeing why they have a right to get their money back from your settlement.

A Medicare lien is limited to the amount it paid for medical services directly related to your accident. They cannot touch the parts of your settlement meant for non-medical damages like pain and suffering or lost wages.

Managing this process carefully is an important step in protecting your final recovery amount. It ensures you meet your legal obligation while keeping as much of your settlement as possible. The goal is to verify every single charge and confirm you are only repaying what is legally required, which is how we figure out how much Medicare will take from my settlement.

How Medicare Figures Out What You Owe

So, you’ve reached a settlement. The big question now is, how much of that does Medicare get? It’s not a simple percentage, but there is a clear process, and it all starts with one important first step.

You or your attorney must report your personal injury case to Medicare’s official recovery arm, the Benefits Coordination & Recovery Center (BCRC). Think of this as officially putting Medicare on notice. Once you do, they get to work.

The BCRC will pull together an itemized list of every medical payment they believe is connected to your injury. This is their opening number, but it’s rarely the final one.

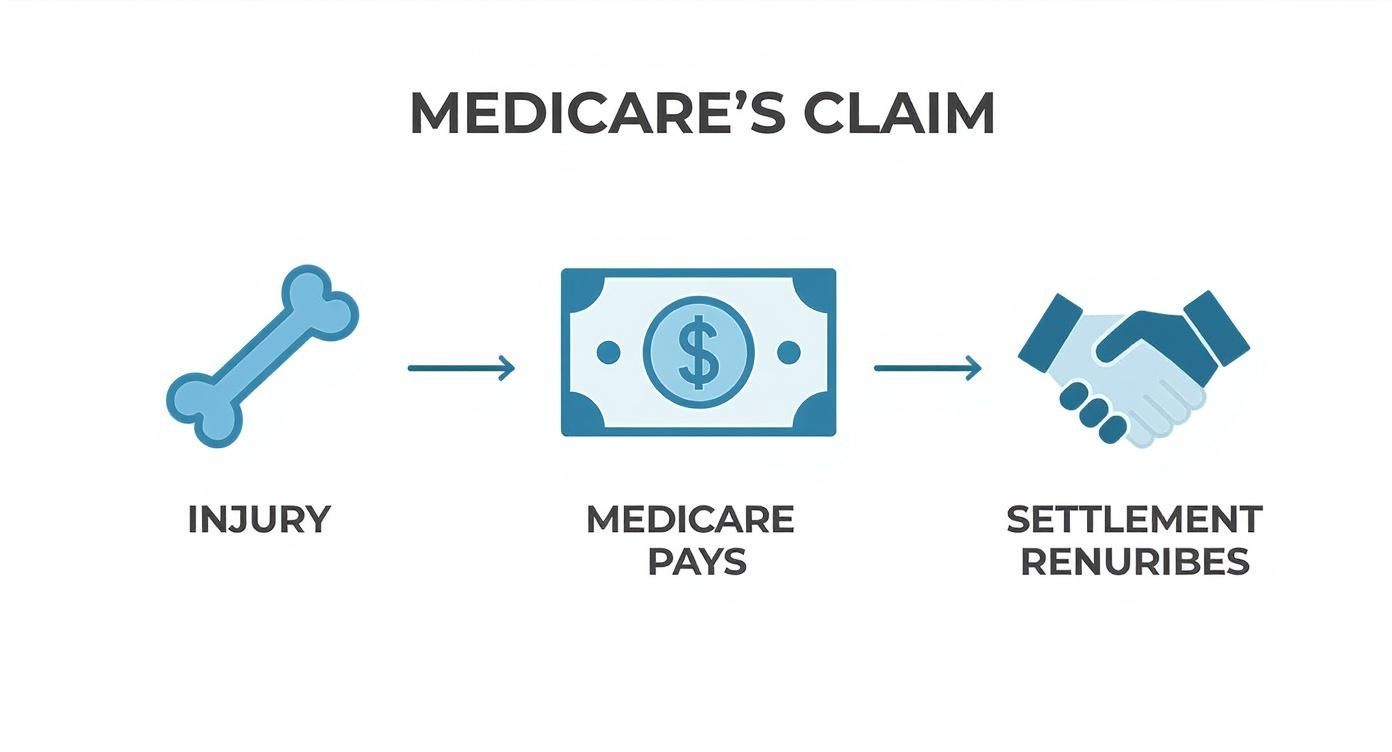

This visual breaks down how your settlement money flows back to reimburse Medicare for the bills it covered while your case was pending.

Essentially, the settlement becomes the primary payer, and Medicare gets its conditional payments paid back from that fund.

Scrutinize and Dispute Every Charge

This is where a sharp eye pays off. You and your lawyer need to review that list of charges line by line. It’s surprisingly common for Medicare’s initial list to include treatments that have absolutely nothing to do with your accident.

You have every right to dispute these unrelated charges. For instance, if you see a bill for a routine physical that was scheduled long before your injury, that doesn’t belong there. Every incorrect charge you successfully remove directly reduces the amount of the lien. This is one of the most effective ways to lower what you ultimately have to pay back.

The Final Calculation: Factoring in Reductions

Once the list contains only accident-related medical bills, there’s some good news. The final amount you owe is almost always less than the total on that list. Why? Because Medicare automatically reduces its claim to account for your legal fees and costs.

This is called a "procurement cost" reduction. It’s the government’s way of acknowledging that you had to spend money to get the settlement that’s now paying them back.

Here’s a simple example of how it plays out:

- Total Related Medical Bills: Let's say Medicare paid $10,000 for your injury-related care.

- Calculate Procurement Costs: Add up your attorney’s fee and case expenses as a percentage of your total settlement. For this example, let's say those costs come out to 40% of the settlement.

- Apply the Reduction: Medicare reduces its $10,000 claim by that same percentage (40%). That means they knock $4,000 off their lien, and your final repayment amount is $6,000.

This reduction is a standard, built-in part of the process. It ensures Medicare contributes its fair share toward the expenses of securing the settlement fund, making the whole system more equitable for you.

One last thing to keep in mind: taxes. While most personal injury settlements aren't taxable, some portions can be. If any part of your settlement is considered taxable income, a 1.45% Medicare tax could apply in 2025. On a $100,000 taxable portion, that would be $1,450. You can find more details on how the Medicare tax rate works and how it might impact your net recovery.

By challenging unrelated charges and ensuring all reductions are applied, you get a much clearer, and often smaller, answer to the pressing question: how much will Medicare take from my settlement?

Proven Strategies to Reduce Your Medicare Lien

After months of fighting for a fair settlement, getting that final demand letter from Medicare can feel like a punch to the gut. But that initial number isn't the final word.

The federal government has official pathways to request a reduction. Knowing how to use them is key to protecting your settlement funds. You aren't automatically stuck with the first bill they send.

We primarily use two strategies to lower what clients have to pay back: requesting a compromise or a waiver.

The Compromise Request

Think of a compromise as a formal negotiation with the government. You're asking the Centers for Medicare & Medicaid Services (CMS) to accept less than the full amount they've demanded.

This isn't just about asking nicely for a discount, though. You need to build a solid case based on the specific facts of your claim.

Common grounds for a compromise include:

- Disputed Liability: If it was a tough fight to prove the other party was 100% at fault, your settlement was likely reduced to reflect that risk.

- Low Settlement Amount: Sometimes, the at-fault driver has minimal insurance coverage. If your settlement is small compared to your total medical bills and losses, we can argue that paying the full lien would be deeply unfair.

In these situations, the goal is to show CMS that collecting the entire debt isn't practical or fair given the unique circumstances of your case.

The Waiver Request

A waiver is a request to have the entire Medicare debt forgiven. As you might expect, this is a much higher bar to clear and is reserved for cases of genuine financial hardship.

To secure a waiver, you must prove that repaying the debt would deprive you of money needed for essential living expenses like food, housing, and medicine. It requires a complete and honest look at your financial picture.

You'll need to gather substantial documentation to prove your financial state, including:

- Income statements and recent tax returns

- Monthly household bills, like rent or mortgage statements and utility bills

- A full accounting of your assets and debts

The objective here is to clearly demonstrate that you simply cannot afford to repay Medicare without putting your basic financial stability at risk. Successfully handling the personal injury lawsuit process is one thing; making sure you keep enough of your settlement to actually live on is another.

Options for Reducing Medicare Repayment

Both strategies require careful preparation and strong documentation. Here’s a quick breakdown of how they compare.

| Method | Description | Best For Situations Where… |

|---|---|---|

| Compromise | A negotiation to reduce the lien amount based on case-specific facts, like disputed fault or a low policy limit. | The settlement amount doesn't fully cover all your damages, or liability was difficult to prove. |

| Waiver | A request to completely forgive the lien debt due to significant financial hardship. | Repaying the lien would prevent you from affording basic necessities like housing, food, and medicine. |

By understanding your options and building a compelling case, you can proactively challenge Medicare’s demand. This is a vital step in ensuring you keep more of the funds you rightfully deserve.

Planning for Future Medical Costs with a Medicare Set-Aside

Sometimes, settling up with Medicare for past medical bills isn't the final chapter. If your injury is serious enough to need ongoing medical care—the kind Medicare would typically cover—you may need to establish a Medicare Set-Aside (MSA).

Think of an MSA as a dedicated savings account funded with a piece of your settlement. Its sole purpose is to pay for all future medical care related to your injury. The fundamental rule is that your settlement money must be the primary payer for these future costs. Only after the MSA funds are completely and properly spent can Medicare start paying for your accident-related treatments again.

When Is a Medicare Set-Aside Needed?

MSAs have been a fixture in workers' compensation cases for years, but now they are becoming much more common in personal injury claims. The Centers for Medicare & Medicaid Services (CMS) has a vested interest in making sure its future financial obligations are protected when a settlement involves someone who is on Medicare or will be soon.

An MSA is generally recommended in two specific situations:

- You are a current Medicare beneficiary, and your total settlement is more than $25,000.

- You have a "reasonable expectation" of enrolling in Medicare within 30 months of your settlement, and the total settlement amount exceeds $250,000.

It's helpful to see an MSA not as a penalty, but as a planning tool. Setting up and managing it correctly is what protects your future eligibility for all your Medicare benefits—not just those tied to your injury.

Managing MSA Funds and Tax Considerations

Once the right amount for the MSA is determined, usually after a detailed projection of your future medical needs, the money is deposited into a separate, interest-bearing account. From there, you have to keep meticulous records of every dollar spent and submit annual reports to CMS. This is how you prove the funds were used correctly.

As you look at the bigger financial picture, don't forget that other deductions will affect your net settlement. Federal and state income taxes, for instance, can take a significant bite. In 2025, federal income tax brackets range from 10% to 37%. A large settlement could easily push you into a higher bracket, increasing your tax liability.

Getting a handle on these requirements is a non-negotiable part of the settlement process. To help you prepare for the road ahead long after your case is closed, please check out the resources we have available. This will bring more clarity to the all-important question of how much Medicare will take from my settlement.

Common Questions About Medicare and Settlements

When you're trying to put the pieces back together after an injury, facing a Medicare lien can feel like one more hurdle. To help bring some clarity, here are direct answers to some of the questions we hear most often from our clients here in Atlanta.

Knowing the answers can make a real difference in how you approach your settlement. It helps you set realistic expectations and understand your rights.

Can Medicare Take My Entire Settlement?

No, absolutely not. This is a common fear, but it's unfounded. Medicare's claim is strictly limited to the amount it paid for medical treatments directly related to your accident.

They cannot touch the portions of your settlement meant to compensate you for other damages, such as:

- Pain and suffering

- Lost wages from time off work

- Loss of enjoyment of life

Their recovery is tied only to the specific medical bills they covered for you. Think of it as a reimbursement, not a penalty.

How Long Does It Take to Resolve a Medicare Lien?

Patience is key here. The process isn't instant and can take several weeks or even a few months after your case settles.

The timeline involves several steps: notifying Medicare of the settlement, waiting for them to issue their final demand letter, reviewing that letter for accuracy, and finally, making the payment. Rushing this can lead to overpayment, so it's important to let the process unfold correctly. It's also vital to be aware of the timeline for your case overall, as you can learn more about the statute of limitations for personal injury in Georgia in our detailed guide.

Can I Just Pay Medicare Myself?

While you technically can, it's generally not a good idea. The process has many procedural requirements and deadlines that are easy to miss.

An experienced personal injury attorney manages this entire process for you. We handle the communication with the BCRC, dispute any unrelated charges, and ensure all possible reductions are applied before a single dollar is sent. This proactive management is designed to protect your final recovery.

It's important to remember that ignoring a Medicare lien has serious consequences. The government can take legal action against you, the at-fault party, and even your attorney to recover the funds. It is a legal obligation that must be satisfied.

By understanding these key points, you can feel more in control of the situation. The goal is always to ensure Medicare is repaid correctly and fairly, which helps you get a clearer final answer to how much will Medicare take from my settlement.