If you're asking how much car accident settlement to expect after a wreck in Atlanta, you're trying to find clarity in a confusing time. While you might see national figures floating around, like an average of $30,416, that number is practically useless for your specific situation. From our experience as Atlanta personal injury attorneys, we can tell you a settlement isn't a pre-set amount. It's a figure built entirely from the ground up, based on the unique, real-world losses you suffered right here in Georgia. Understanding the factors that go into a typical car accident settlement is the first step toward getting a fair outcome.

Understanding a Typical Car Accident Settlement

It's easy to get fixated on an "average" settlement number, but it is more helpful to see it as a statistical landmark than a reliable map for your own journey. The true value of your claim is a combination of two things: the hard costs you can add up on a calculator and the human costs that don't come with a price tag.

The goal is to put the pieces of your life back together financially. The settlement is meant to compensate you for every single loss you endured because someone else was negligent.

The Building Blocks of Your Claim

The foundation of any settlement is built on two main types of "damages"—the legal term for the losses you can be paid for. These are the core components an insurance adjuster, or a jury, will look at.

- Economic Damages: These are the straightforward, calculable expenses. Think of every medical bill, from the first ambulance ride to your last physical therapy session. This category also covers lost paychecks from missed work and the bill to fix or replace your car.

- Non-Economic Damages: These are the personal, human costs of the crash. This is compensation for your physical pain, the emotional distress and anxiety, and the simple loss of being able to enjoy your life the way you did before. There's no receipt for this kind of suffering, but it's a major part of any fair settlement.

Let's break down exactly what falls into these categories.

Common Components of a Settlement

| Type of Damage | What It Covers |

|---|---|

| Medical Expenses | ER visits, hospital stays, surgery, physical therapy, medication, and future care. |

| Lost Wages | Income lost while you were unable to work, including future earning capacity if disabled. |

| Property Damage | The cost to repair your vehicle or its fair market value if it was totaled. |

| Pain and Suffering | Compensation for the physical pain and emotional distress caused by your injuries. |

| Loss of Enjoyment | Acknowledges your inability to participate in hobbies, activities, or daily routines. |

While recent data suggests a national average settlement is around $30,416 for 2025, that figure is just a starting point. It's often misleading because it blends minor fender-benders with catastrophic injury cases.

To get a real sense of what your claim is worth, you have to understand the full scope of what your personal injury claim can cover. A fair assessment of how much car accident settlement is right for your case depends on a careful accounting of all these factors, not a national average.

Key Factors That Influence Your Settlement Amount

When you're trying to figure out how much a car accident settlement might be worth, it’s important to understand that the final number isn’t just pulled out of a hat. Instead, it's carefully calculated based on several key factors. Think of it like building a case—each piece of evidence adds strength and value.

The single most important element is the severity of your injuries. A minor whiplash case that clears up in a few weeks is valued very differently than a back injury requiring surgery and causing long-term pain. The more the crash disrupts your physical health and daily life, the higher the potential settlement.

The Foundation: Economic Damages

Every settlement starts with a solid foundation of your direct financial losses, legally known as economic damages. These are the tangible, out-of-pocket costs you've incurred because of the accident. Keeping a detailed record of every single expense is absolutely essential here.

These measurable costs include:

- All Medical Bills: This covers everything from the ambulance ride and ER visit to follow-up appointments, physical therapy, prescriptions, and any medical devices you need.

- Lost Wages and Income: If you missed work during your recovery, those lost paychecks are a direct financial hit. This also extends to future earning capacity if your injuries stop you from returning to your old job.

- Property Damage: The cost to fix your car—or its fair market value if it was totaled—is another key component of this calculation.

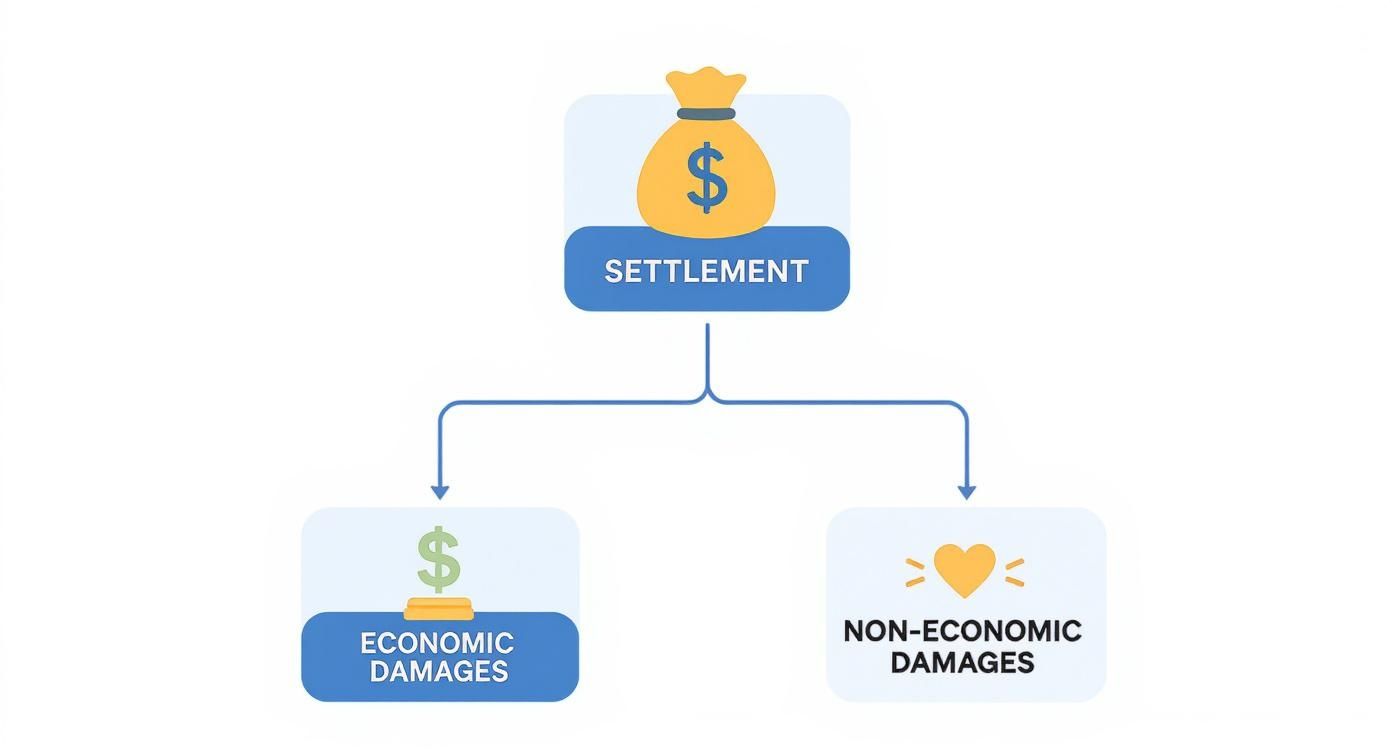

This infographic shows how these concrete economic damages combine with the less tangible non-economic damages to build your total settlement value.

As you can see, both the calculable financial losses and the personal, human costs are essential pillars that support the final settlement amount.

Proving Fault and Georgia's Negligence Rule

Another major piece of the puzzle is establishing who was at fault. In Georgia, this is handled under the "modified comparative negligence" rule. This legal doctrine can directly reduce your settlement if you're found partially responsible.

Under Georgia law (O.C.G.A. § 51-12-33), you can still recover damages as long as you are less than 50% at fault. However, your total compensation will be reduced by your percentage of fault.

Let's look at a simple example. Say your total damages add up to $100,000, but a jury finds you were 20% at fault (maybe you were driving a few miles over the speed limit). Your final award would be cut by that 20%, leaving you with $80,000. If you're found to be 50% or more at fault, you cannot recover anything at all.

The Impact of Insurance Policy Limits

Finally, the insurance policies involved can put a hard ceiling on what you can actually recover, no matter how strong your case is. While every Georgia driver must carry liability insurance, many only have the state-mandated minimums. The Georgia Office of Insurance provides helpful information on these requirements.

If the at-fault driver has only a $25,000 policy limit, that is the most their insurance company has to pay for your injuries—even if your medical bills alone are $75,000. This is precisely why your own Uninsured/Underinsured Motorist (UM/UIM) coverage is so important. It can step in and provide another source of recovery when the other driver’s policy falls short.

Understanding how these elements—injury severity, economic losses, fault, and policy limits—all fit together is the first real step toward answering the question of how much a car accident settlement is worth in your specific case.

How Insurance Companies Calculate an Offer

When you file a claim, you're probably wondering, how much car accident settlement will the insurance company actually offer? They don't just pull a number out of thin air. Insurance adjusters use specific formulas to come up with their initial offer, and knowing their playbook is your first advantage.

Remember, that first number they give you is just their opening move. It's the start of a negotiation, not the final word.

Insurance companies often lean on a formula called the "multiplier method." It’s a straightforward way for them to put a dollar figure on the intangible, human side of your injuries—things like pain, suffering, and the disruption to your life. This is often where the bulk of a settlement's value lies.

The Multiplier Method Explained

The multiplier method is a two-part calculation. First, the adjuster will tally up all your concrete, provable financial losses. In legal terms, these are called special damages.

- Total Medical Bills: This covers everything from the ambulance ride and ER visit to surgery, prescriptions, and ongoing physical therapy.

- Lost Wages: This is the income you lost because the accident kept you out of work.

- Property Damage: The cost to get your vehicle repaired or replaced is also included in this base number.

Once they have that total, they multiply it by a number, usually between 1.5 and 5. This "multiplier" is supposed to reflect the severity of your injuries and their long-term impact on your life.

A low multiplier, like 1.5x, might be used for minor whiplash with a quick recovery. A much higher multiplier, like 4x or 5x, is reserved for serious injuries that cause permanent scarring, a lasting disability, or a major change to your quality of life.

The screenshot below gives a great real-world example of how an adjuster might put this formula to work.

As you can see, that multiplier is the most subjective part of the equation. It's also where you and the insurance company will almost certainly disagree.

Why Their First Offer Is Just a Starting Point

An adjuster's job is to protect their company's profits, which means paying out as little as they can get away with. They will almost always start with a low multiplier and a skeptical view of your damages.

They might challenge whether a certain medical treatment was truly necessary or argue that your pain isn't as bad as you say. This is standard practice.

That’s why their first offer is rarely their best offer. It's a strategic move to see if you'll accept a quick, lowball payout and walk away. While data shows average payouts can be around $37,249, that figure is typically reached after negotiation, not by taking the first number on the table.

Remember, the initial offer is an invitation to negotiate. It reflects the insurance company's interpretation of your case, which is often biased in their favor.

Knowing how they calculated their number gives you the power to counter it effectively. You can learn more about what to expect by reading our overview of the car accident lawsuit process in Georgia. A strong response, backed by solid proof of all your damages—both financial and personal—is the key to getting a fair settlement for your claim.

Understanding Catastrophic Injury Settlements

When people google "how much car accident settlement," they see numbers that mostly reflect minor fender-benders. A catastrophic injury—think spinal cord damage, severe brain trauma, or paralysis—is in a completely different ballpark. Trying to compare it to a standard accident claim is like comparing a routine doctor’s visit to the cost of lifelong, specialized medical care.

These life-altering injuries aren’t just about the medical bills you have today. They demand a meticulous projection of future costs that can easily span decades. The goal isn’t to cover what’s already been spent; it’s to secure a future that was permanently derailed by someone else’s negligence.

Why Averages Don't Apply

The sheer scope of damages in a catastrophic injury case renders typical settlement formulas useless. The common "multiplier method" might work for a broken arm, but it completely fails to account for the immense, lifelong needs that follow a devastating accident.

Instead, the valuation is built from the ground up, based on a lifetime of necessities. This includes things like:

- Lifelong Medical Treatment: This isn't a one-and-done deal. It often means multiple surgeries, continuous physical therapy, prescription drugs, and specialist visits for the rest of a person's life.

- In-Home Care and Assistance: Many victims need 24/7 nursing care or help with basic daily activities like eating, bathing, and getting around.

- Home and Vehicle Modifications: This covers the very real costs of making a home wheelchair-accessible, installing special lifts, or buying a vehicle equipped for a person with disabilities.

- Loss of Future Earning Capacity: This calculation goes far beyond just lost wages. It projects the entire career path that was stolen—promotions, raises, and retirement benefits included.

For the most severe injuries, like a traumatic brain injury, the need for specialized long-term care is a massive component of the claim. This often involves therapies aimed at recovery and adaptation, which is why understanding neurorehabilitation is so important for painting a full picture of future needs. For more information on what these injuries entail, you can consult resources like the Shepherd Center right here in Atlanta, a leader in brain and spinal cord injury treatment.

The Human Cost is Exponentially Higher

Beyond the eye-watering financial costs, the non-economic damages—often called "pain and suffering"—are valued on an entirely different level. The loss of quality of life is profound. It’s about not being able to walk, live independently, play with your kids, or go back to the career you spent years building.

In these cases, compensation isn't just for physical pain. It’s for the permanent loss of normalcy, the emotional distress of dependency, and the complete alteration of one's life path. This is the largest and most significant component of a catastrophic injury settlement.

Real-world jury verdicts show just how significant these damages can be. For instance, in a notable 2025 case, a woman hurt in a T-bone crash was awarded $36.4 million by a jury. That massive verdict included $25 million specifically for future non-economic damages, proving how heavily these human costs are weighted in the most serious cases.

These settlements aren't windfalls; they are carefully calculated figures designed to provide a lifetime of essential support. They are a financial lifeline meant to restore as much stability and dignity as possible after a life-shattering event. Learning what a skilled Atlanta catastrophic injury lawyer does can make it clearer how these types of claims are built and won.

Ultimately, when a catastrophic injury happens, the question of how much car accident settlement is answered not by averages, but by a painstaking, forward-looking assessment of a lifetime of needs.

Practical Steps To Protect Your Claim's Value

When you're trying to figure out how much car accident settlement you might get, the steps you take right after the crash are very important. Every action can either strengthen your claim's value or give an insurance company a reason to reduce its offer. It all starts at the scene.

This screenshot from the Georgia Department of Public Safety shows where to get official documents like an accident report. Having the right paperwork from the very beginning builds a strong foundation for your claim.

Your Post-Accident Checklist

Your health is the top priority after a collision. If you're able to, though, taking these simple actions can protect your financial recovery later.

- Seek Immediate Medical Attention: This is non-negotiable for both your health and your claim. Some injuries don't show symptoms right away. Insurance adjusters see gaps in treatment as a red flag and may argue your injuries aren't that serious.

- Document Absolutely Everything: Think like an investigator. Use your phone to take photos of both vehicles, the crash scene, any visible injuries, and road conditions. Don't forget to get names and contact info from any witnesses.

- File an Official Police Report: A police report is an unbiased, official record of what happened. It contains vital details like the date, time, location, and the officer’s initial assessment of the incident.

Taking these initial steps creates a solid, evidence-based record that's tough for an insurance company to argue with.

What To Do In The Following Days And Weeks

The period after the crash is just as important. The way you handle your medical care and documentation can make or break your settlement amount.

- Follow Your Doctor's Orders: Go to every follow-up appointment, physical therapy session, and specialist visit. Sticking to your treatment plan demonstrates that you are serious about your recovery.

- Keep a Detailed Folder: Start a file for every piece of accident-related paperwork. This means every medical bill, pharmacy receipt, repair estimate, and email from the insurance companies.

- Track Your Out-of-Pocket Expenses: Keep a running list of costs you've paid yourself, like gas for trips to the doctor or over-the-counter medical supplies. These small amounts can really add up.

Be extremely cautious when speaking to the other driver's insurance adjuster. They will likely ask for a recorded statement early on. You are not required to give one, and it's best to decline until you've consulted an attorney. Their questions are designed to get you to say something that minimizes or denies your claim.

Getting your vehicle properly repaired at a fair price is another key part of protecting your claim's total value. There are good resources available for finding trusted auto repair services that can help you vet local shops.

Finally, you must respect the deadlines. Georgia has a strict time limit for filing a personal injury lawsuit. If you miss it, you lose your right to compensation forever. You can learn more about these deadlines in our guide to the statute of limitations for personal injury in Georgia. By taking these practical steps, you put yourself in the strongest position to get a fair answer to the question of how much car accident settlement you truly deserve.

How a Lawyer Can Help Maximize Your Settlement

https://www.youtube.com/embed/1ibvx2qypg0

When you're trying to figure out how much car accident settlement you might get, you'll probably wonder if hiring a lawyer is worth it. This question comes up a lot, especially if the other driver's insurance company calls you right away with a quick offer.

The reality is, an experienced attorney understands the insurance industry's playbook. Their real value is knowing how to counter it.

Insurance adjusters are trained professionals whose job is to protect their company’s bottom line. That means paying you as little as possible. A good lawyer knows their tactics and comes prepared with the evidence to fight back.

Taking the Burden Off Your Shoulders

Recovering from an accident is a full-time job on its own. A lawyer steps in to manage all the important, time-consuming legal tasks so you can focus on getting better.

This includes:

- Handling All Communications: They become the single point of contact for the insurance companies. This prevents you from accidentally saying something that could weaken your claim.

- Managing Paperwork and Deadlines: From filing official notices to gathering medical records, they handle the entire administrative load. They ensure you don't miss any important deadlines set by Georgia law.

- Gathering Evidence: Attorneys know what it takes to build a strong case. They work to collect police reports, witness statements, medical documentation, and expert testimony.

This support system lets you heal without the constant stress of a legal fight hanging over your head.

A landmark study from the Insurance Research Council confirmed what many of us in the field see every day. On average, people who hired a lawyer received significantly higher settlements than those who went it alone—even after accounting for attorney fees.

Uncovering the Full Value of Your Claim

Maybe the single most important role an attorney plays is calculating the true value of your claim. This is a far more involved process than just adding up your current medical bills and calling it a day.

A skilled lawyer identifies every possible source of compensation. They look ahead, projecting future needs like ongoing physical therapy or lost earning potential if you can't go back to your old job.

They are also experienced in putting a fair dollar value on your pain and suffering. This is a major part of your settlement that insurance companies almost always try to undervalue or dismiss entirely.

By presenting the insurer with a detailed, evidence-backed demand package, your attorney sends a clear message: you are serious about getting what you deserve. This thorough preparation is the key to maximizing how much car accident settlement you ultimately walk away with.

Frequently Asked Questions About Car Accident Settlements

After a wreck, it's completely normal to wonder, how much car accident settlement can I expect? People often have the same worries about the process, what it all means, and how long it's going to take. Here are some direct answers to the questions we hear most often from people right here in Atlanta.

Our goal is to provide clear, straightforward information to help you understand the road ahead. Every case is unique, but these answers cover the common ground most people will cross.

How Long Does It Take to Get a Settlement?

This is probably the number one question, and the honest answer is: it really depends. A straightforward case with clear fault and minor injuries might wrap up in a few months. But if your injuries are severe and need long-term medical care, the process is naturally going to take longer.

It is very important not to rush things. A settlement should only be finalized after you’ve reached what’s known as Maximum Medical Improvement (MMI). This is the point when your doctor confirms your condition is stable and isn't expected to get any better. Settling before MMI is a huge gamble because you won't know the full, final cost of your medical treatment—and you only get one shot to get this right.

Do I Have to Pay Taxes on My Settlement?

For the most part, the answer is no. The Internal Revenue Service (IRS) generally does not treat compensation for personal physical injuries or sickness as taxable income.

This means the parts of your settlement that cover things like:

- Medical expenses

- Lost wages from being unable to work due to physical injury

- Pain and suffering directly linked to a physical injury

…are typically not taxed. There are exceptions, though. Compensation for purely emotional distress (not caused by a physical injury) or punitive damages can be taxable. You can find general guidance on this topic from sources like Wikipedia's page on settlement damages. It's always smart to run your specific award by a financial professional.

One of the biggest mistakes you can make is accepting a quick offer before understanding the full extent of your injuries. A fast settlement is rarely a fair one.

What if the At-Fault Driver Has No Insurance?

That’s a scary thought, but you still have options. This is exactly why Georgia law requires insurers to offer Uninsured/Underinsured Motorist (UM/UIM) coverage. If you have this on your own policy, you can file a claim with your own insurance company to cover your losses.

Essentially, your UM/UIM policy steps into the shoes of the other driver's missing insurance. It’s an essential layer of protection that provides a lifeline when you need it most. This is why we always tell our clients to carry as much UM/UIM coverage as they can comfortably afford. It's one of the best ways to protect yourself and your family from a worst-case scenario. We hope this FAQ helps you better understand the factors influencing how much car accident settlement you may receive.

At Jamie Ballard Law, we believe you deserve clarity and strong advocacy after an accident. If you have more questions or need help with your case in Atlanta, we offer a free, no-obligation case evaluation to discuss your options. Visit us online at https://jamieballardlaw.com to learn more.