How much will Medicare take from my settlement is one of the most urgent questions injured Georgians face when a case nears resolution. You worked hard to build your claim. You went through treatment, missed work, and fought for fair compensation. Then someone mentions a Medicare lien — and suddenly your settlement feels like it belongs to someone else. How much will Medicare take from my settlement depends on what Medicare paid for your injury-related care, whether you negotiate the lien, and which legal tools your attorney uses to reduce it. This guide explains exactly how that process works in Georgia.

You Settled — Now Medicare Wants Its Money Back

If you receive Medicare benefits and you were injured in an accident, Medicare almost certainly paid some of your medical bills. Under federal law, Medicare is a secondary payer. That means it steps in to cover care when another party — like an at-fault driver’s insurer — should have paid first.

When you settle your personal injury claim, that settlement represents the primary payment. Medicare then asserts a lien — a legal right to recover what it spent on your injury-related treatment from your settlement proceeds.

This Is Not Optional

The Medicare Secondary Payer Act gives the federal government the right to recover its payments from any settlement you receive. This is not a courtesy request. If you settle and fail to reimburse Medicare, the government can pursue you — and your attorney — directly for double the amount owed.

Practical rule: If you receive Medicare and you settle a personal injury claim without addressing the Medicare lien, you could owe the full lien amount out of pocket after the fact.

Medicare Liens Are Not the Same as Medicaid Liens

Many clients confuse the two. Medicare is the federal program for people 65 and older — or those with qualifying disabilities. Medicaid is the state-run program for low-income individuals. Both create liens on settlements, but the rules differ significantly. This guide focuses on Medicare liens in Georgia personal injury cases.

How Much Will Medicare Actually Take From My Settlement in Georgia

The short answer: Medicare takes back exactly what it paid for your injury-related care — but that number can often be reduced through negotiation.

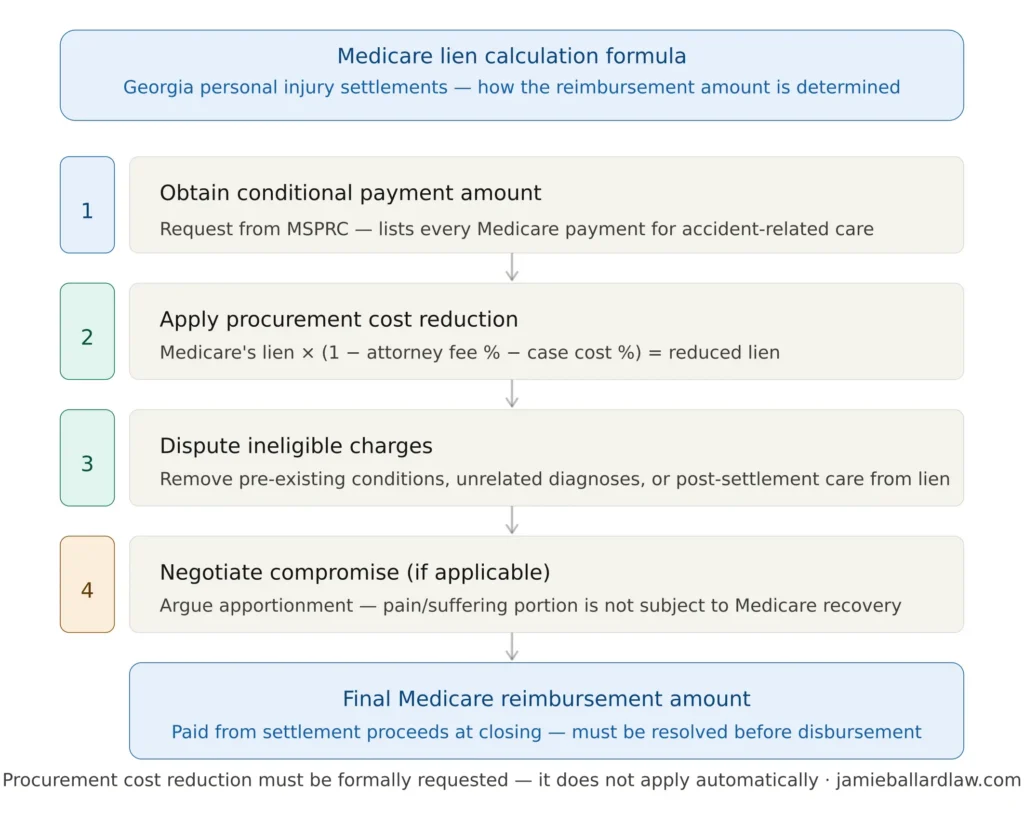

The Conditional Payment Amount

Medicare tracks every claim it pays that relates to your accident. Before your case settles, your attorney requests a conditional payment letter from the Medicare Secondary Payer Recovery Contractor (MSPRC). This document lists every payment Medicare made for accident-related treatment — and the total it intends to recover from your settlement.

That total is called the conditional payment amount. It is the starting number — not necessarily the final number you pay back.

The Procurement Cost Reduction

Federal law requires Medicare to reduce its lien by a proportionate share of your attorney fees and litigation costs. The formula works like this:

If your attorney fee is one-third of the settlement and litigation costs are 10%, Medicare reduces its lien by roughly 43%. So a $30,000 conditional payment could drop to around $17,000 after the procurement cost reduction is applied.

Practical rule: The procurement cost reduction alone can cut your Medicare lien by a third or more — but you have to formally request it. It does not happen automatically.

The $5,000 or Under Rule — Flat 25% Recovery

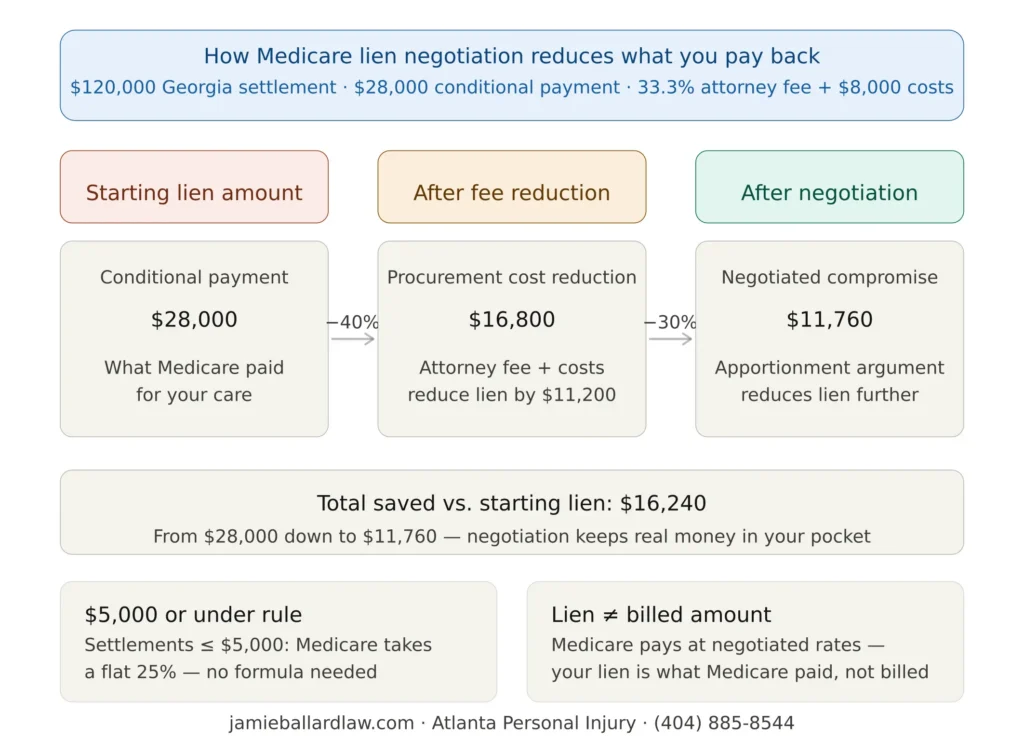

For settlements of $5,000 or less, Medicare simplifies the process. It takes a flat 25% of the total settlement amount, regardless of what it actually paid. This fixed-percentage option avoids the paperwork of a full lien dispute for smaller cases.

What Medicare Paid vs. What Was Billed

Medicare pays providers at negotiated rates — usually far less than what was billed. Your Medicare lien is based on what Medicare actually paid, not the original billed amount. This distinction matters. A $45,000 hospital bill might have been paid by Medicare at $18,000. Your lien is $18,000, not $45,000.

Can You Negotiate a Medicare Lien Down Further

Yes — and this is where having the right attorney makes a measurable financial difference.

The Waiver Process

You can request a waiver of the Medicare lien if repaying it would cause financial hardship or if the lien recovery would be against equity and good conscience. Waivers are not easy to obtain, but they are a legitimate path — especially when the settlement amount is low relative to the total damages and the lien is large.

The Compromise Process

More commonly, attorneys negotiate a compromise — a reduced lien amount agreed to by Medicare and the injured party. Medicare considers the total settlement amount, the strength of the liability case, the injured person’s overall damages, and what share of the settlement is fairly attributable to past medical expenses versus pain and suffering.

If only 20% of your settlement is attributable to past medical care and 80% reflects pain, suffering, and future losses, Medicare should only be reimbursed for that 20% portion. A skilled attorney makes that argument formally.

Practical rule: Medicare rarely accepts its first conditional payment amount as final. Negotiation is expected — and it routinely results in reductions of 30% to 60% off the initial figure.

Challenging What Medicare Included

Not every treatment Medicare paid for after your accident is legally recoverable. Medicare’s conditional payment list sometimes includes charges for pre-existing conditions, unrelated diagnoses, or treatment that predated the accident. Your attorney can dispute those line items and have them removed from the lien before the final settlement is distributed.

The Process: What Happens Step by Step

| Step | Who Acts | What Happens |

|---|---|---|

| 1. Notify Medicare | Your attorney | Reports your claim to the MSPRC as soon as litigation begins |

| 2. Request conditional payment letter | Your attorney | Gets the full list of what Medicare paid for your injury care |

| 3. Dispute ineligible charges | Your attorney | Removes unrelated or pre-existing condition charges from the list |

| 4. Apply procurement cost reduction | Your attorney | Calculates proportionate fee/cost reduction and submits to Medicare |

| 5. Negotiate compromise if needed | Your attorney + MSPRC | Agrees on a reduced lien amount based on settlement apportionment |

| 6. Settle and pay lien | Your attorney (from proceeds) | Medicare is paid from settlement funds at closing |

| 7. Demand letter to MSPRC | MSPRC | Issues final demand — must be paid within 60 days of settlement |

The timeline from notification to final lien resolution typically runs 60 to 120 days. This is one reason personal injury cases involving Medicare can take longer to close after a settlement is reached — the lien process runs parallel to the case itself and must be fully resolved before funds are distributed.

What Happens If You Don’t Pay the Medicare Lien

This is where people get into serious trouble. If you receive a settlement and do not resolve the Medicare lien, the federal government has aggressive recovery tools available.

Double Damages Against You

Under the Medicare Secondary Payer Act, if you receive a settlement and fail to reimburse Medicare, the government can sue you for double the lien amount. That means a $20,000 lien becomes a $40,000 judgment.

Your Attorney Is Also Liable

Your personal injury attorney has an independent obligation to protect Medicare’s interests in the settlement. If your attorney distributes your settlement proceeds without resolving the lien, they face the same double-damages exposure. This is why reputable Atlanta personal injury lawyers make Medicare lien resolution a non-negotiable part of every case involving a Medicare beneficiary.

Practical rule: Never accept settlement funds and walk away without confirming in writing that the Medicare lien has been resolved. “I didn’t know” is not a defense under the Medicare Secondary Payer Act.

Future Medicare Benefits Can Be Affected

In cases involving future medical treatment — particularly spinal cord injuries or traumatic brain injuries — the settlement must include a Medicare Set-Aside (MSA) arrangement. This is a separate allocation from the settlement that is set aside specifically to pay for future injury-related care. If you don’t create one when required, Medicare can refuse to cover your future injury care until the MSA funds are exhausted.

Medicare Set-Asides in Georgia — When Are They Required

Not every settlement requires a Medicare Set-Aside — but you need to know when one does.

CMS Thresholds

The Centers for Medicare and Medicaid Services (CMS) has established informal thresholds. A Medicare Set-Aside is generally required when:

- The settlement is $25,000 or more and the claimant is a current Medicare beneficiary

- The settlement is $250,000 or more and the claimant has a reasonable expectation of Medicare enrollment within 30 months

These are the thresholds at which CMS reviews and approves MSA submissions — but many attorneys recommend MSAs even below these amounts to protect clients from future Medicare disputes.

How an MSA Works in Practice

The MSA amount is determined by a life care planner or certified Medicare set-aside consultant. It reflects the cost of future injury-related treatment over the claimant’s life expectancy — at Medicare rates. Those funds are placed in a separate interest-bearing account and can only be used for injury-related care. Once the account is exhausted, Medicare resumes primary coverage for those expenses.

Practical rule: If your case involves permanent injuries and future medical care, and you’re on Medicare or approaching eligibility, ask your attorney directly: “Does this settlement include an MSA?” If they don’t have an answer, that’s a red flag.

Real Numbers: How Much Does a Medicare Lien Reduce Your Settlement

Here’s a concrete example so you can see how these pieces interact.

Say you settle a Georgia car accident case for $120,000. Medicare paid $28,000 for your injury-related treatment.

- Attorney fee: 33.3% = $40,000

- Case costs: $8,000

- Total procurement costs: $48,000 (40% of settlement)

- Medicare lien reduction: 40% of $28,000 = $11,200 reduction

- Adjusted lien after procurement reduction: $28,000 – $11,200 = $16,800

If your attorney further negotiates a 30% compromise based on apportionment arguments, the lien drops to roughly $11,760. On a $120,000 settlement, that’s a $16,240 difference from the original lien — real money that stays in your pocket.

You can learn more about how settlements are structured and what deductions to expect from the Centers for Medicare and Medicaid Services, as well as the official Medicare.gov resource on how Medicare interacts with legal settlements.

Why This Is Harder Without an Attorney

You can technically handle your own Medicare lien. You can contact the MSPRC, request your conditional payment letter, and try to negotiate directly. Here’s what that looks like in practice:

The MSPRC is a federal contractor with its own internal procedures, timelines, and dispute forms. Response times average 45 to 90 days per inquiry. Errors on your paperwork reset the clock. Most people who try to handle this alone either miss the procurement cost reduction entirely or fail to dispute ineligible charges — leaving thousands of dollars on the table.

An experienced personal injury attorney who handles Medicare liens regularly knows the dispute process, has established communication with the MSPRC, and can typically resolve a lien faster and at a lower amount than a claimant acting alone. For more on Georgia-specific lien law, the State Bar of Georgia provides referral resources for injury victims navigating complex settlement issues.

For a deeper explanation of how these liens work on video, this overview from Personal Injury Law Gurus on Medicare, Medicaid, and ERISA liens covers the fundamentals clearly.

Practical rule: The MSPRC is not your advocate. They have no obligation to tell you about reductions you qualify for. Your attorney does.

Georgia-Specific Rules That Affect Your Medicare Lien

Georgia law adds another layer on top of federal Medicare rules. Understanding both is important when you are trying to figure out what you will actually keep from your settlement.

Georgia’s Made Whole Doctrine

Under Georgia law, an injured person must be made whole before a lienholder can recover. This means that if your total damages — medical bills, lost wages, pain and suffering, future care — are greater than your settlement amount, you can argue that Medicare should not recover its full lien because you haven’t been fully compensated.

The made whole doctrine does not automatically override the federal Medicare Secondary Payer Act. Federal law generally takes precedence. But your attorney can use the made whole argument as leverage in a compromise negotiation to push Medicare’s recovery lower, especially in cases where the liability policy limit is less than your total damages.

Subrogation Limits in Georgia

Georgia places limits on subrogation rights — the ability of a payer to step into your shoes and recover what they paid. For private health insurance under Georgia state law, subrogation is capped and subject to proportionate reduction rules. Medicare, as a federal program, operates under its own federal framework — but the same reduction principles your attorney applies to private health insurance liens apply to Medicare as well.

The Official Code of Georgia Annotated governs many of the state-level lien rights that interact with your settlement, and the Georgia Department of Labor provides resources for workers whose injuries occurred in a work context and involve both workers’ comp and Medicare.

When You Have Both Medicare and a Georgia Workers’ Compensation Claim

If your injury happened at work and you filed a workers’ compensation claim in Georgia, the Medicare lien analysis becomes more complicated. Workers’ comp settlements have their own Medicare Set-Aside requirements — separate from a personal injury MSA. CMS reviews workers’ comp MSA submissions and has its own thresholds and approval process. Your attorney must handle both the workers’ comp lien resolution and the personal injury Medicare lien separately if you have both types of claims arising from the same incident.

Statute of Limitations Does Not Protect You From Medicare

Some clients assume that once their case is closed and funds are distributed, Medicare cannot come after them. That assumption is wrong. Medicare has three years from the date it knew or should have known about your settlement to file a recovery action. The statute of limitations for your underlying injury claim has no bearing on Medicare’s recovery window. Resolving the lien at settlement is the only clean way to close this chapter.

Common Mistakes That Cost Injury Victims Money

After handling hundreds of cases involving Medicare liens, the same errors come up repeatedly. Avoiding them starts with knowing what they are.

Waiting Until Settlement to Notify Medicare

The earlier your attorney notifies Medicare about your claim, the more time there is to get an accurate conditional payment amount — and to dispute errors. Attorneys who wait until the eve of settlement to contact the MSPRC often face rushed timelines, incomplete payment records, and less room to negotiate. Medicare notification should happen at the start of litigation, not the end.

Accepting the Conditional Payment Amount Without Review

The conditional payment letter is Medicare’s starting position, not a final bill. Every line item on that letter should be reviewed. Charges for unrelated conditions, pre-existing treatments, or post-settlement care sometimes appear on the list. Each one you successfully dispute reduces the final lien amount — dollar for dollar.

Failing to Request the Procurement Cost Reduction

This is the most costly mistake. The procurement cost reduction is a right under federal law — but it must be formally requested. It does not automatically apply. Attorneys who skip this step leave clients paying a lien that should have been reduced by their proportionate share of attorney fees and case costs.

Practical rule: Ask your attorney specifically: “Have you requested the procurement cost reduction from Medicare?” If they hesitate or seem uncertain, that is a problem worth following up on.

Not Accounting for the Medicare Lien When Evaluating Settlement Offers

A $100,000 settlement offer sounds very different once you know there is a $22,000 Medicare lien attached. Your net recovery — after attorney fees, case costs, and the Medicare lien — is the number that matters. Some clients accept settlement offers without understanding that Medicare will take a significant portion. Your attorney should walk you through the net recovery calculation before you sign anything.

Frequently Asked Questions About Medicare and Personal Injury Settlements

| Question | Answer |

|---|---|

| Does Medicare always get paid back from a settlement? | Yes, if Medicare paid for injury-related care. The Medicare Secondary Payer Act requires reimbursement from any settlement proceeds. |

| Can I negotiate the Medicare lien amount? | Yes. Through the compromise process, your attorney can negotiate a reduced amount based on apportionment and the strength of the liability case. |

| What if my settlement isn’t enough to cover the lien? | You may be eligible for a waiver based on financial hardship, or a compromise to reduce the lien to a level the settlement can cover. |

| How long does Medicare lien resolution take? | Typically 60 to 120 days from initial notification to final demand letter, though disputes can extend the timeline. |

| What is a Medicare Set-Aside? | A portion of the settlement allocated to cover future injury-related medical costs — required when the settlement is large and the injured person is a current or near-future Medicare beneficiary. |

| Does Medicare take money from pain and suffering? | No — Medicare’s lien only covers the portion of the settlement attributed to past medical expenses Medicare paid. A skilled attorney argues that pain and suffering damages are not subject to the lien. |

| What happens if my attorney doesn’t tell Medicare about my settlement? | Both you and your attorney face liability for double the lien amount under federal law. Reputable attorneys always notify Medicare and resolve the lien before distributing funds. |

| Can Medicare take my whole settlement? | In theory, if the lien equals or exceeds the settlement amount, yes — but that outcome is rare and typically avoidable through negotiation, waiver, or compromise. |

Protecting What You Earned: How Medicare Settlement Liens Work in Your Favor With the Right Help

You don’t have to accept the first number Medicare puts on the table. How much will Medicare take from my settlement is not a fixed answer — it is a negotiation, and Georgia injury victims who work with experienced attorneys routinely keep thousands more than those who don’t. Jamie Ballard Law handles Medicare lien resolution as part of every personal injury case involving a Medicare beneficiary — so you never face the federal government alone. Call (404) 885-8544 or visit the contact page for a free consultation.

About Jamie Ballard Law

Jamie Ballard Law is an Atlanta-based personal injury law firm representing injured Georgians in car accidents, slip and falls, wrongful death claims, and complex settlement matters including Medicare and Medicaid lien resolution. The firm serves clients throughout Atlanta and the surrounding metro area, fighting to maximize every dollar of compensation clients receive.