When you get hit by a driver who doesn't have insurance, one of the first things you'll wonder is what an average uninsured motorist settlement looks like. As an Atlanta personal injury attorney, I can tell you the blunt answer is: there's no magic number. Every single case is different, and that's because every person's experience and losses are unique.

Think of it less like a standard payout and more like a custom-built solution. Your settlement is pieced together from the specific, real-world costs you've faced—from medical bills and lost paychecks to your physical pain and mental anguish.

What a Typical Uninsured Motorist Settlement Looks Like

It’s completely natural to want a simple, straightforward figure after a crash with an uninsured driver. But the value of your uninsured motorist (UM) claim isn't based on some national average. It’s a direct reflection of your personal losses.

In these situations, your own UM coverage steps up to the plate. It essentially takes the place of the insurance the at-fault driver should have carried.

This is why you have it—your UM policy is a financial safety net designed to make you whole again. It compensates you for the actual damages you've sustained, which are generally broken down into two core categories.

The Building Blocks of Your Claim

The entire process really starts by methodically calculating every single loss you've incurred because of the accident. This isn't about pulling numbers out of thin air; it’s about adding up the tangible costs and then assigning a fair, recognized value to the intangible suffering.

- Economic Damages: These are the straightforward, out-of-pocket expenses. They have a clear dollar value tied to them and are the easiest to prove with receipts and records.

- Non-Economic Damages: This category is about the human cost. It’s meant to compensate you for things like physical pain, emotional trauma, and the inability to enjoy life the way you did before the crash.

Let's break down what these categories actually cover.

What Your Uninsured Motorist Settlement Covers

Your UM settlement is meant to cover a broad range of losses, from bills you can hold in your hand to the personal impact the accident had on your life.

| Damage Category | Examples of What It Covers |

|---|---|

| Economic Damages | Medical bills (ER, surgery, physical therapy), lost wages from missed work, future lost earning capacity, property damage (car repairs/replacement), prescription costs. |

| Non-Economic Damages | Physical pain and suffering, emotional distress and anxiety, loss of enjoyment of life, permanent disfigurement or scarring, loss of consortium (impact on your marriage). |

As you can see, a comprehensive settlement goes far beyond just paying for your immediate hospital bills.

The final settlement amount is ultimately determined by two things: the strength of your documentation and the limits of your own insurance policy. Your total compensation cannot go beyond the UM coverage amount you chose when you bought your policy.

Putting a final number on a claim involves a mix of state laws, medical expert opinions, and legal precedent. Because every single situation is unique—from the severity of the injuries to how clear the fault is—settlement amounts can vary dramatically. You can get more familiar with the factors insurers consider by looking at resources from the Insurance Information Institute.

Ultimately, understanding these components is the first real step toward figuring out the potential value of your uninsured motorist settlement.

The Reality of Uninsured Drivers on the Road

To understand why having uninsured motorist (UM) coverage is so essential—and how it directly impacts a potential average uninsured motorist settlement—you first have to get a clear picture of what’s happening on our roads. It’s a jarring fact, but a significant number of drivers in Georgia and across the U.S. get behind the wheel without any insurance at all. This isn't just their problem; it creates a serious financial risk for every single person who follows the law.

When you're out there driving, you’re sharing the road, and that means you’re also sharing the risk. The hard truth is that people drive uninsured for all sorts of reasons, from financial struggles to simply gambling they won’t get into a wreck. That reality is precisely why having your own UM protection is non-negotiable for any smart, prepared driver.

The Scope of the Problem

The number of uninsured drivers is far higher than most people assume. It's a persistent, widespread issue that can leave responsible drivers holding the bag after a crash.

Recent data paints a sobering picture of American roadways. In 2023, an estimated 15.4 percent of all motorists were uninsured. Think about that for a moment—more than one out of every seven drivers you see on your commute probably doesn't have any auto insurance.

That statistic represents millions of drivers and underscores the very real possibility of getting hit by someone who has no way to pay for your injuries or vehicle damage. You can see the full data and how these numbers have shifted by checking the statistics from the Insurance Information Institute.

Why This Matters for Your Protection

Knowing these numbers isn't just for trivia. It's about recognizing the huge gap that your Uninsured Motorist coverage is specifically designed to fill. Without it, you could be facing a mountain of medical bills and repair costs with no obvious way to get them paid.

Here's why this context is so important:

- High Probability: With so many uninsured drivers out there, the odds of an accident involving one are not as low as you might hope.

- Financial Shield: Your UM policy is a financial backstop. It protects your own assets from the consequences of another driver's irresponsibility.

- Peace of Mind: Knowing you have this coverage means you have a plan. It ensures there’s a source of funds available if the worst happens.

At the end of the day, carrying solid UM coverage is a proactive decision. It’s an acknowledgment of the real-world risks on the road and ensures you have a reliable way to handle the financial fallout, which directly affects your ability to secure a fair uninsured motorist settlement.

Key Factors That Shape Your Settlement Amount

Since there’s no official calculator for an average uninsured motorist settlement, it's far more useful to understand the real-world factors that actually build your claim’s value. Don't think of your settlement as one magic number. Instead, see it as a structure built from several distinct, provable components.

Each piece represents a tangible loss you suffered, and together, they form the foundation of your final compensation. The process begins by methodically cataloging every single way the accident has impacted your life, from your physical health to your financial stability.

The Core Building Blocks of Your Claim

The final value of your claim is tied directly to the severity of your damages. Insurance adjusters and, if necessary, your attorney will scrutinize several key areas to determine what's fair. It’s a methodical process of adding up every documented cost and assigning a recognized value to your personal suffering.

Here are the primary factors that determine what your claim is ultimately worth:

- Severity of Your Injuries: This is the heavyweight champion of all factors. A claim involving minor whiplash and a few trips to the doctor will be valued completely differently than one involving a spinal cord injury that requires surgery and lifelong care.

- Total Medical Bills (Past and Future): This is a straightforward calculation of every cost tied to your medical care—the ER visit, any hospital stay, surgeries, physical therapy, prescription drugs, and any future treatments your doctors anticipate you'll need.

- Lost Income and Earning Capacity: If your injuries kept you out of work, you are entitled to compensation for those lost wages. If the injury is permanent and hobbles your ability to earn a living in the future, this becomes a major component of the settlement.

- Vehicle and Property Damage: The cost to repair or replace your vehicle is a black-and-white part of your claim. This also covers any other personal property, like a laptop or phone, that was destroyed in the crash.

The Role of Your Own Policy Limits

There is one important element that puts a hard cap on your settlement's potential value: your own insurance policy. No matter how high your calculated damages climb, you cannot recover more than the Uninsured Motorist (UM) coverage limits you chose.

Your UM policy limit acts as a ceiling on your potential settlement. For example, if your total damages amount to $75,000 but your UM coverage limit is $50,000, the absolute maximum you can recover from your insurer is $50,000.

This is precisely why choosing adequate coverage before an accident happens is so important. Georgia law requires insurers to offer UM coverage, but the amount you carry is up to you. You can find more details about Georgia’s auto insurance requirements on the state’s official Office of Insurance and Safety Fire Commissioner website.

Understanding these pieces gives you a practical roadmap of how a final number is calculated, providing valuable insight into the potential worth of your uninsured motorist settlement.

How Your Location Impacts Your Claim

It’s easy to assume a car accident is the same no matter where it happens, but that’s a misconception. The state where your crash occurs plays a huge role in your claim. From local laws to the sheer number of uninsured drivers on the road, geography shapes your case from day one. Any discussion of the average uninsured motorist settlement is incomplete without this essential context.

Think about it this way: driving in a state with a high rate of uninsured motorists means you’re statistically far more likely to get hit by one. This isn't just an abstract number; it's a real-world risk that changes the moment you cross a state line.

State Laws and Your Uninsured Motorist Claim

Every state has its own rulebook for auto insurance, and these differences are not minor. Here in Georgia, for example, insurers must offer you Uninsured Motorist (UM) coverage, but you have the right to reject that offer in writing. In other states, carrying UM coverage is mandatory, period.

These legal nuances are exactly why a claim filed in Atlanta proceeds differently than one in another state.

- "No-Fault" vs. "At-Fault" States: Georgia is an "at-fault" state. This means the driver who caused the accident is legally responsible for the damages. In "no-fault" states, your own insurance covers your initial medical bills, regardless of fault, which changes how and when your UM coverage comes into play. You can learn more about how fault systems work on Wikipedia's page for Tort law.

- Stacking Policies: Some states let you "stack" UM policies. If you insure multiple vehicles, you can combine their UM coverage limits to create a much larger pool of funds for a serious accident. Georgia has very specific rules about when and how stacking is allowed.

How Uninsured Driver Rates Vary by State

The percentage of drivers without insurance is anything but uniform across the country. In fact, the numbers vary dramatically from one state to the next, which directly influences both insurance premiums and claim trends.

While the national average often sits around 14 percent, the state-level data tells the real story. Take a look at the data below for some high-risk and low-risk states. You can explore a more comprehensive breakdown in Bankrate's analysis of uninsured motorist statistics.

Uninsured Driver Rates a High vs Low State Comparison

| State | Uninsured Motorist Rate (%) |

|---|---|

| Tennessee | 20.0 |

| New Mexico | 20.8 |

| Michigan | 20.3 |

| Wyoming | 5.9 |

| Massachusetts | 6.2 |

A higher rate of uninsured drivers in your area often leads to higher premiums for UM coverage because the risk for insurers is greater. More importantly, it highlights just how essential it is to carry adequate protection if you live in a high-risk state.

Ultimately, your location sets the entire stage for your claim. It dictates the laws, the statistical risks, and the environment in which your case will unfold. This geographic context is a fundamental factor in determining what a fair uninsured motorist settlement looks like for your specific situation.

A Step-by-Step Guide to Filing Your UM Claim

When you're hit by a driver with no insurance, the path forward can feel overwhelming. While it's helpful to understand the factors that shape an average uninsured motorist settlement, the most important part is taking the correct legal steps right from the start. Each action you take builds the foundation for a successful claim.

This guide provides an actionable checklist for filing your Uninsured Motorist (UM) claim. Following these steps helps protect your right to fair compensation during a difficult time.

1. Seek Medical Attention Immediately

Your health is the priority. Even if you feel your injuries are minor, you must get a professional medical evaluation. The adrenaline from a crash can easily mask serious conditions like whiplash or internal bleeding, which may not show symptoms for hours or even days.

Prompt medical care creates an official record linking your injuries directly to the accident. Any delay gives the insurance company an opening to argue that your injuries were caused by something else.

2. Report the Accident to the Police

Always call law enforcement to the scene. An officer will create an official police report, which is an essential piece of evidence documenting the facts of the crash. This report serves as an unbiased, third-party account of the incident.

You'll need a copy of this report for your claim. In Georgia, you can typically request it from the local police department or directly from the Georgia Department of Transportation for accidents on state highways.

3. Notify Your Own Insurance Company

You are required to report the accident to your own insurance carrier promptly. Most policies contain a notice clause, and failing to inform them in a timely manner could jeopardize your ability to make a claim under your UM coverage.

When you make the call, stick to the basic facts. State that you were in an accident, the at-fault driver was uninsured, and you intend to file a claim under your Uninsured Motorist policy. Avoid speculating on fault or the extent of your injuries.

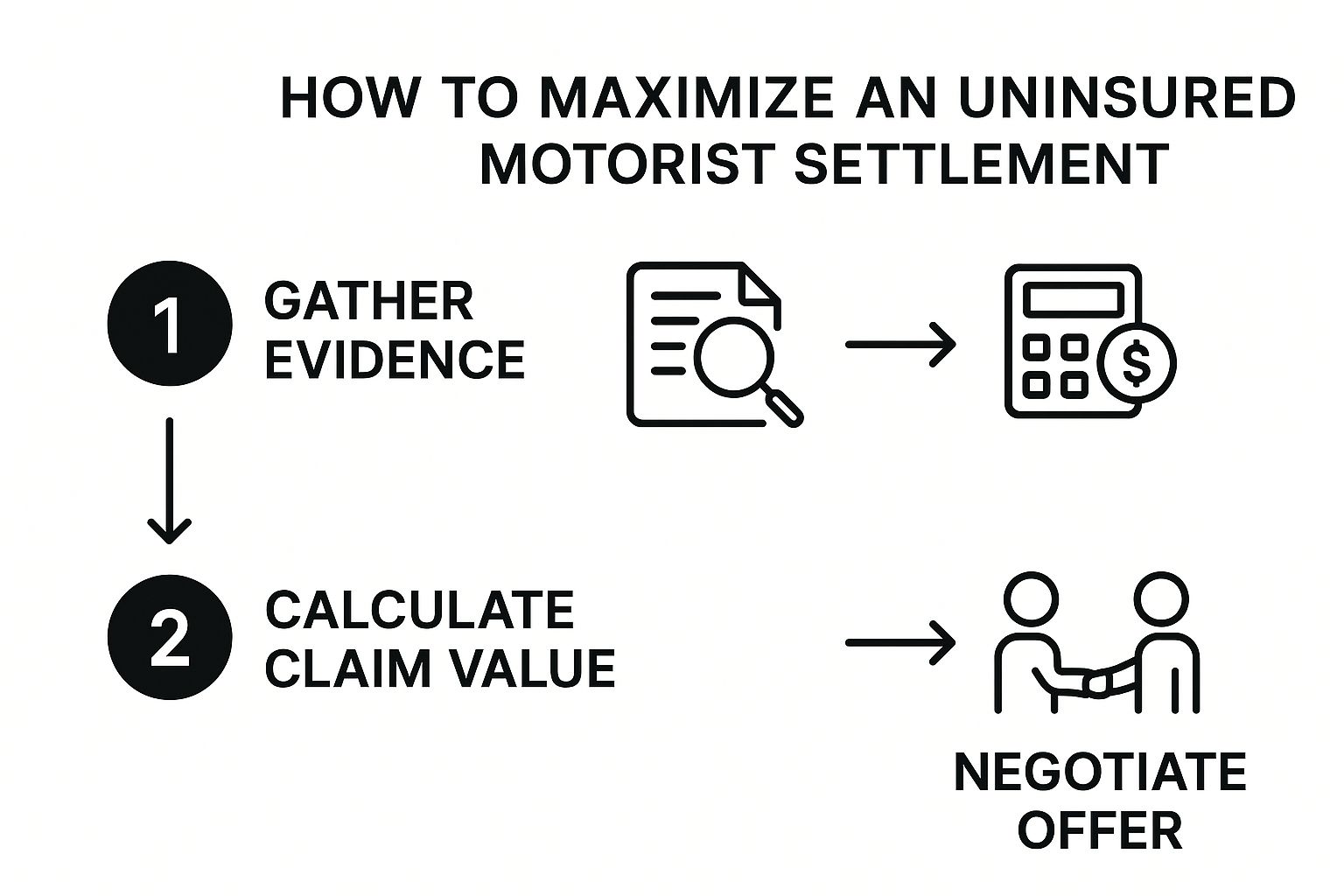

4. Document Everything Carefully

From this moment on, you must become a meticulous record-keeper. Every receipt, bill, and note strengthens your claim and helps prove the full value of your damages.

- Medical Records: Keep a complete file of all bills, physician notes, treatment plans, and receipts from doctors, hospitals, physical therapists, and pharmacies.

- Photos and Videos: If possible, take pictures of the damage to your vehicle, your visible injuries, and the accident scene, including skid marks or debris.

- Lost Wages: Obtain a letter from your employer on company letterhead. It should detail your regular pay rate, your job duties, and the specific dates you were unable to work due to your injuries.

- Pain Journal: Document your physical pain and emotional state each day. This journal provides tangible evidence for your pain and suffering, which is a key component of your damages.

This infographic illustrates how these initial steps are fundamental to the entire settlement process.

As the visual shows, gathering strong evidence is the essential first phase. No valuation or negotiation can begin without it. By following this careful, step-by-step process, you put yourself in the strongest possible position to secure a fair uninsured motorist settlement.

Answering Your Questions About UM Claims

When you're trying to heal after a crash, the last thing you need is a mountain of confusing insurance questions. But that's often exactly what happens. Many of our clients in Atlanta come to us worried about how the claims process works and what it means for their future.

We want to clear up that confusion. Below are straightforward answers to the most common questions we hear about uninsured motorist (UM) claims and what it takes to get a fair average uninsured motorist settlement.

Frequently Asked Questions

-

What Happens in a Hit-and-Run Accident?

It’s one of the most frustrating and violating experiences a driver can have. If the person who hit you speeds off and can't be found, your Uninsured Motorist (UM) coverage is specifically designed to step in. For insurance purposes, a hit-and-run is treated exactly like an accident caused by a driver with no insurance whatsoever.

Your own UM policy becomes the source of compensation for your medical bills, lost income, and pain and suffering. To activate it, you have to show that the crash wasn't your fault and the other driver is unidentifiable. This is why calling 911 immediately is non-negotiable—a police report creates the official record needed to prove a hit-and-run occurred.

-

Will Filing a UM Claim Make My Insurance Rates Go Up?

This is a huge and completely valid concern. The short answer is no. In Georgia, it is against the law for an insurance company to raise your premiums for using your UM coverage when you weren't at fault. You pay for this exact protection every month for a reason: to shield you from irresponsible drivers.

You are simply using the benefits you paid for to cover losses caused by someone else. If your insurer tries to hike your rates or threaten to drop your policy after a not-at-fault UM claim, they may be operating in bad faith.

-

What Is the Difference Between Uninsured and Underinsured Coverage?

They sound almost the same, but Uninsured Motorist (UM) and Underinsured Motorist (UIM) coverage kick in for two very different scenarios. Knowing which is which tells you what kind of protection you really have.

- Uninsured Motorist (UM) Coverage: This applies when the at-fault driver has zero insurance coverage or when you're the victim of a hit-and-run.

- Underinsured Motorist (UIM) Coverage: This is for situations where the at-fault driver has insurance, but their policy limits are too low to cover the full extent of your damages. If your medical bills hit $80,000 but the other driver only carries the state minimum of $25,000, your UIM coverage can step in to cover the $55,000 gap, up to your policy's limit.

Both are essential safety nets. Georgia law requires insurers to offer you this coverage, and you can see the specifics on the official Georgia state government website. Understanding these answers is the first step toward demystifying the process and preparing you to secure a fair uninsured motorist settlement.